|

市场调查报告书

商品编码

1876551

膜市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Membranes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

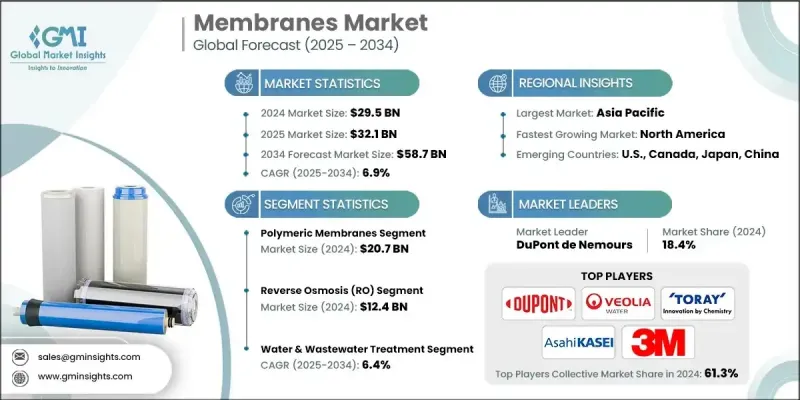

2024年全球膜市场价值为295亿美元,预计2034年将以6.9%的复合年增长率成长至587亿美元。

由于排放标准日益严格,新的废水排放目标出台,各行业正越来越多地将膜技术整合到废水处理过程中。监管指南鼓励使用薄膜生物反应器和逆渗透等先进系统,以实现近零液体排放,这促使各行业采用高回收率薄膜以提高成本效益。淡水资源日益短缺,促使政府和企业投资海水淡化和回收技术。各地海水和微咸水逆渗透工厂的成长推动了薄膜技术的应用。薄膜复合膜(TFC)和聚偏氟乙烯(PVDF)薄膜的不断改进,包括提高渗透性、抗污染性和耐久性,降低了营运成本,并使其能够应用于各种具有挑战性的场合。持续的研发和试点计画进一步支持了市场的长期扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 295亿美元 |

| 预测值 | 587亿美元 |

| 复合年增长率 | 6.9% |

2024年,聚合物薄膜市场规模预计将达207亿美元。这些膜产品凭藉其适应性和优异的性能占据主导地位。聚偏氟乙烯(PVDF)、聚酰胺(PA)和聚醚砜(PES)材料因其高化学稳定性、高渗透性和易结垢性,被广泛应用于工业和市政领域的各种过滤製程。防污涂层和表面改质技术的不断创新,进一步提升了这些膜产品的可靠性和使用寿命。

2024年,逆渗透(RO)市场规模预计将达到124亿美元。逆渗透系统能够高效去除溶解盐和杂质,因此在水净化和工业循环利用领域至关重要。低能耗逆渗透系统和薄膜复合材料(TFC)薄膜技术的进步进一步提高了效率,同时降低了营运成本。这些改进正在巩固逆渗透技术在已开发经济体和新兴经济体中的主导地位。

由于北美拥有成熟的工业基础和严格的水处理法规,预计到2024年,北美膜市场将占据26.1%的份额。市政水回用、海水淡化项目以及各行业工业过滤系统升级改造的投资,都推动了市场扩张。日益增强的环保意识也促使超滤和逆渗透系统得到更广泛的应用,以满足更严格的污染物排放标准。

全球膜市场的主要参与者包括杜邦公司、东丽株式会社、Hydranautics(日东集团旗下)、科赫膜系统公司、颇尔公司(丹纳赫旗下)、旭化成株式会社、LG化学有限公司、威立雅水务技术公司、滨特尔公司、3M公司、Iono Innovations、Aquaporin A/SadiMode、Aquaporin、SadiModeant公司和SadiModeing公司、Aquaporin、SadiModeant公司和SadiModeing公司。膜市场企业采取的关键策略包括:大力投资研发以提高薄膜的效率和使用寿命;建立策略联盟和合作伙伴关係以扩大全球业务;以及不断创新产品以满足不同的产业需求。此外,各公司也专注于收购以巩固市场地位,并进入新兴市场以抓住新的成长机会。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 严格的水质法规和环保署合规要求

- 水资源日益短缺及海水淡化需求

- 工业废水处理要求

- 膜材料的技术进步

- 产业陷阱与挑战

- 高昂的初始资本投资和系统成本

- 膜污染及运作挑战

- 市场机会

- 与再生能源系统集成

- 智能膜技术与物联网集成

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 材料类型

- 科技

- 应用

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依材料类型划分,2021-2034年

- 主要趋势

- 聚合物薄膜

- 陶瓷膜

- 复合膜和混合膜

- 其他的

第六章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 微滤(MF)

- 超滤(UF)

- 奈米过滤(NF)

- 逆渗透(RO)

- 电渗析(ED)

- 其他的

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 水和废水处理

- 市政饮用水处理

- 工业废水处理

- 膜生物反应器(MBR)系统

- 水资源再利用与回收

- 海水淡化应用

- 海水逆渗透(SWRO)

- 苦咸水处理

- 能量回收与优化

- 工业加工

- 食品饮料应用

- 製药与生物技术

- 化学和石油化学加工

- 石油和天然气生产水处理

- 采矿和金属回收

- 气体分离及能源应用

- 氢气纯化和燃料电池

- 天然气加工

- 空气分离应用

- 储能和电池隔膜

- 医疗和生物技术应用

- 血液透析及医疗器材

- 无菌过滤与生物加工

- 体外诊断(IVD)

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Hydranautics (Nitto Group)

- Koch Membrane Systems

- Pall Corporation (Danaher)

- Asahi Kasei Corporation

- LG Chem Ltd.

- Veolia Water Technologies

- Pentair plc

- 3M Company

- Ionomr Innovations Inc.

- Aquaporin A/S

- Modern Water plc

- Gradiant Corporation

- Membrion, Inc.

The Global Membranes Market was valued at USD 29.5 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 58.7 billion by 2034.

Industries are increasingly integrating membrane technologies into wastewater treatment processes due to stricter discharge standards and new effluent targets. Regulatory guidelines encourage the use of advanced systems, such as membrane bioreactors and reverse osmosis, to achieve near-zero liquid discharge, prompting industries to adopt high-recovery membranes for cost efficiency. Rising freshwater scarcity is driving both governments and businesses to invest in water desalination and recycling technologies. Growth in seawater and brackish water reverse osmosis plants across various regions is boosting membrane adoption. Continuous improvements in thin-film composite (TFC) and PVDF membranes, including enhanced permeability, fouling resistance, and durability, are reducing operational costs and enabling their use in challenging applications. Ongoing R&D and pilot initiatives further support long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.5 Billion |

| Forecast Value | $58.7 Billion |

| CAGR | 6.9% |

The polymeric membranes segment generated USD 20.7 billion in 2024. These membranes dominate due to their adaptability and superior performance. PVDF, PA, and PES materials are widely used in various filtration processes for industrial and municipal applications because of their high chemical stability, permeability, and ease of scaling. Continuous innovations in antifouling coatings and surface modifications are further extending their reliability and lifespan.

The reverse osmosis (RO) segment generated USD 12.4 billion in 2024. RO systems are highly effective in removing dissolved salts and impurities, making them critical for water purification and industrial recycling. Advances in low-energy RO systems and TFC membranes have further enhanced efficiency while reducing operational costs. These improvements are strengthening RO's dominance in both developed and emerging economies.

North America Membranes Market captured 26.1% share in 2024 owing to its established industrial base and stringent water treatment regulations. Market expansion is supported by investments in municipal water reuse, desalination projects, and upgrades to industrial filtration systems across various industries. Rising environmental awareness has increased the adoption of ultrafiltration and RO systems to comply with stricter contaminant standards.

Major players in the Global Membranes Market include DuPont de Nemours, Inc., Toray Industries, Inc., Hydranautics (Nitto Group), Koch Membrane Systems, Pall Corporation (Danaher), Asahi Kasei Corporation, LG Chem Ltd., Veolia Water Technologies, Pentair plc, 3M Company, Ionomr Innovations Inc., Aquaporin A/S, Modern Water plc, Gradiant Corporation, and Membrion, Inc. Key strategies adopted by companies in the Membranes Market include investing heavily in research and development to improve membrane efficiency and lifespan, forming strategic alliances and partnerships to expand global reach, and continuously innovating product offerings to meet diverse industrial requirements. Companies are also focusing on acquisitions to consolidate market position and entering emerging markets to capture new growth opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent water quality regulations & epa compliance requirements

- 3.2.1.2 Growing water scarcity & desalination demand

- 3.2.1.3 Industrial wastewater treatment mandates

- 3.2.1.4 Technological advancements in membrane materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment & system costs

- 3.2.2.2 Membrane fouling & operational challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with renewable energy systems

- 3.2.3.2 Smart membrane technologies & IoT integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Material Type

- 3.7.3 Technology

- 3.7.4 Application

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polymeric membranes

- 5.3 Ceramic membranes

- 5.4 Composite & hybrid membranes

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Microfiltration (MF)

- 6.3 Ultrafiltration (UF)

- 6.4 Nanofiltration (NF)

- 6.5 Reverse Osmosis (RO)

- 6.6 Electrodialysis (ED)

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Water & wastewater treatment

- 7.2.1 Municipal drinking water treatment

- 7.2.2 Industrial wastewater processing

- 7.2.3 Membrane bioreactor (MBR) systems

- 7.2.4 Water reuse & reclamation

- 7.3 Desalination applications

- 7.3.1 Seawater reverse osmosis (SWRO)

- 7.3.2 Brackish water treatment

- 7.3.3 Energy recovery & optimization

- 7.4 Industrial processing

- 7.4.1 Food & beverage applications

- 7.4.2 Pharmaceutical & biotechnology

- 7.4.3 Chemical & petrochemical processing

- 7.4.4 Oil & gas produced water treatment

- 7.4.5 Mining & metal recovery

- 7.5 Gas separation & energy applications

- 7.5.1 Hydrogen purification & fuel cells

- 7.5.2 Natural gas processing

- 7.5.3 Air separation applications

- 7.5.4 Energy storage & battery separators

- 7.6 Medical & biotechnology applications

- 7.6.1 Hemodialysis & medical devices

- 7.6.2 Sterile filtration & bioprocessing

- 7.6.3 In-vitro diagnostics (IVD)

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 DuPont de Nemours, Inc.

- 9.2 Toray Industries, Inc.

- 9.3 Hydranautics (Nitto Group)

- 9.4 Koch Membrane Systems

- 9.5 Pall Corporation (Danaher)

- 9.6 Asahi Kasei Corporation

- 9.7 LG Chem Ltd.

- 9.8 Veolia Water Technologies

- 9.9 Pentair plc

- 9.10 3M Company

- 9.11 Ionomr Innovations Inc.

- 9.12 Aquaporin A/S

- 9.13 Modern Water plc

- 9.14 Gradiant Corporation

- 9.15 Membrion, Inc.

褶皱膜市场规模、份额和成长分析:按褶皱膜类型、材料类型、功能、应用、终端用户产业和地区划分 - 2026-2033 年产业预测

褶皱膜市场规模、份额和成长分析:按褶皱膜类型、材料类型、功能、应用、终端用户产业和地区划分 - 2026-2033 年产业预测 2026-2030年全球食品饮料加工膜市场

2026-2030年全球食品饮料加工膜市场 2026年全球侧向流动免疫检测膜市场研究报告

2026年全球侧向流动免疫检测膜市场研究报告 聚四氟乙烯 (PTFE) 过滤膜市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2026–2034)

聚四氟乙烯 (PTFE) 过滤膜市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2026–2034) 食品饮料原位清洗 (CIP) 系统市场-全球机会分析及产业预测(依产品类型、应用和地区划分):2026-2036 年

食品饮料原位清洗 (CIP) 系统市场-全球机会分析及产业预测(依产品类型、应用和地区划分):2026-2036 年 膜元件市场-全球产业规模、份额、趋势、机会与预测:组成、膜类型、应用、地区和竞争格局,2021-2031年

膜元件市场-全球产业规模、份额、趋势、机会与预测:组成、膜类型、应用、地区和竞争格局,2021-2031年 DTRO膜市场按应用、材料类型、配置、最终用户和工厂规模划分,全球预测,2026-2032年PFSA质子交换膜市场按产品类型、製造技术、厚度范围、结构、应用和最终用途产业划分-2026-2032年全球预测单膜黏合剂市场(按产品类型、形态、聚合物类型、应用、最终用户和分销管道划分),全球预测,2026-2032年全球膜市场:市场规模、占有率、成长率、产业分析、按类型、应用和地区划分的分析以及未来预测(2026-2034)

DTRO膜市场按应用、材料类型、配置、最终用户和工厂规模划分,全球预测,2026-2032年PFSA质子交换膜市场按产品类型、製造技术、厚度范围、结构、应用和最终用途产业划分-2026-2032年全球预测单膜黏合剂市场(按产品类型、形态、聚合物类型、应用、最终用户和分销管道划分),全球预测,2026-2032年全球膜市场:市场规模、占有率、成长率、产业分析、按类型、应用和地区划分的分析以及未来预测(2026-2034)