|

市场调查报告书

商品编码

1876577

微流控市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Microfluidics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

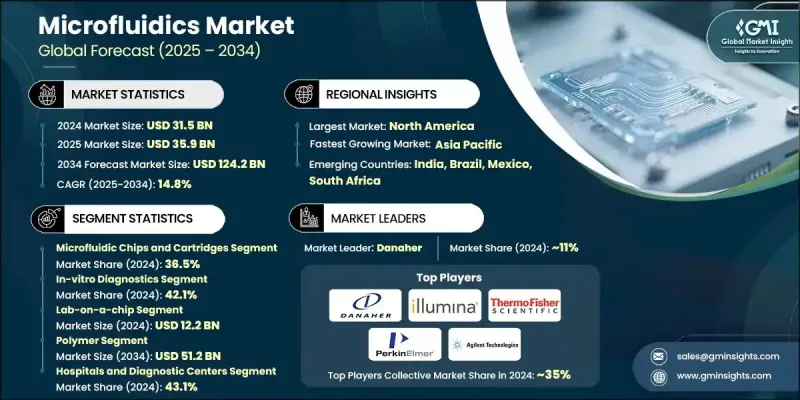

2024 年全球微流控市场价值为 315 亿美元,预计到 2034 年将以 14.8% 的复合年增长率增长至 1242 亿美元。

市场扩张的驱动力来自即时诊断系统的日益普及、精准医疗的兴起以及对更快、更准确的样本分析日益增长的需求。包括癌症、心血管疾病和糖尿病在内的慢性疾病盛行率不断上升,显着增加了对既能提供高效结果又能确保患者舒适度的诊断技术的需求。微流控装置因其能够以极少的样本量提供快速、高精度的结果,在临床和研究应用中得到广泛认可。数位微流控、微型晶片实验室系统和3D细胞培养模型等创新技术的出现,正在拓展该技术在药物研发、生物医学研究和临床诊断等多个领域的应用。此外,不断完善的医疗基础设施和强大的研发投入也在加速微流控技术的应用。微流控技术涉及在微尺度通道内操控极小体积的流体,具有精确控制、试剂消耗量低和成本效益高等优势,使其成为现代诊断和治疗研发中不可或缺的工具。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 315亿美元 |

| 预测值 | 1242亿美元 |

| 复合年增长率 | 14.8% |

微流控晶片和晶片盒在2024年占据了36.5%的市场份额,这主要得益于它们在实现便携式、高效且经济的诊断应用方面发挥的关键作用。这些晶片对于晶片实验室系统和即时检测至关重要,为分散式医疗机构提供了可扩展的解决方案。在诊断基础设施有限的地区,微流控晶片盒的日益普及进一步推动了该领域的成长,因为这些设备无需复杂的实验室设备即可提供快速、准确的检测结果。

体外诊断(IVD)领域预计在2024年占据42.1%的市场份额,这主要得益于慢性病和传染病领域对经济实惠、精准高效且高通量检测的需求不断增长。基于微流控技术的IVD解决方案因其多重检测能力和卓越的灵敏度,被广泛应用于液体活检、基因分析和传染病检测。将其整合到现代实验室工作流程中,可提高诊断效率并缩短週转时间,从而显着推动市场扩张。

2024年,北美微流控市场占43.5%的比重。该地区的领先地位源于美国和加拿大先进的医疗保健体系、大规模的研发投入以及对创新诊断技术的广泛应用。研究机构、医院和学术中心对微流控平台的日益普及,为科技的持续发展创造了有利环境。此外,政府支持的分子诊断、个人化医疗和基于人工智慧的健康分析等倡议,进一步加速了市场渗透,并促进了微流控设备在医疗保健和生命科学领域的应用。

全球微流控市场的主要参与者包括丹纳赫(Danaher)、Illumina、Bio-Rad Laboratories、罗氏(F. Hoffmann-La Roche)、凯杰(Qiagen)、贝克顿·迪金森(Becton Dickinson)、赛默飞世尔科技(Thermo Fisher Scients)、安捷伦科技生物(Agil 这些科技)、MicHoria)、梅梅里科技生物) Microfluidics、Fluigent、Standard BioTools、珀金埃尔默(PerkinElmer)、波士顿製药(Boston Pharmaceutical,旗下品牌Nanomix)、Emulate、uFluidix、Sphere Fluidics和Xona Microfluidics。为了巩固其在全球微流控市场的地位,各大公司正致力于产品创新、自动化整合以及与诊断和製药公司的合作。许多公司正在投资开发多功能晶片实验室平台、数位微流控系统以及可扩展的基于晶片盒的解决方案,这些方案旨在实现快速、高精度的检测。设备製造商和生物技术公司之间的策略合作正在帮助拓展产品组合併加速临床验证。为了顺应去中心化诊断和个人化医疗的发展趋势,各公司也优先考虑小型化和互联互通。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 对即时诊断的需求不断增长

- 个人化医疗和基因组学的扩展

- 与人工智慧和数位健康平台的整合

- 微加工和材料技术的进步

- 产业陷阱与挑战

- 高昂的研发和製造成本

- 监管和标准化方面的障碍

- 市场机会

- 晶片器官和3D细胞培养平台的发展

- 在资源匮乏和分散的环境中采用

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 未来市场趋势

- 技术格局

- 目前技术

- 新兴技术

- 专利分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 主要趋势

- 微流控晶片和晶片盒

- 仪器和分析仪

- 帮浦、阀门和感测器

- 试剂和耗材

- 其他产品

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 製药

- 医疗器材

- 体外诊断

- 其他应用

第七章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 晶片实验室

- 晶片上的器官

- 连续流微流控

- 其他技术

第八章:市场估算与预测:依材料划分,2021-2034年

- 主要趋势

- 硅

- 玻璃

- 聚合物

- 其他材料

第九章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 医院和诊断中心

- 学术和研究中心

- 製药和生物技术公司

- 其他最终用途

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- Agilent Technologies

- Bartels Mikrotechnik

- Becton Dickinson

- bioMerieux

- Bio-Rad Laboratories

- Boston Pharmaceutical (Nanomix)

- Danaher

- Dolomite Microfluidics

- Emulate

- F. Hoffmann-La Roche

- Fluigent

- Illumina

- PerkinElmer

- Qiagen

- Sphere Fluidics

- Standard BioTools

- Thermo Fisher Scientific

- uFluidix

- Xona Microfluidics

The Global Microfluidics Market was valued at USD 31.5 billion in 2024 and is estimated to grow at a CAGR of 14.8% to reach USD 124.2 billion by 2034.

The market's expansion is driven by increasing adoption of point-of-care diagnostic systems, the rise of precision medicine, and the growing demand for faster and more accurate sample analysis. The increasing prevalence of chronic diseases, including cancer, cardiovascular disorders, and diabetes, has significantly amplified the need for diagnostic technologies that deliver efficient results while ensuring patient comfort. Microfluidic devices are gaining widespread acceptance in clinical and research applications due to their ability to provide rapid results with high accuracy using minimal sample quantities. The emergence of innovations such as digital microfluidics, miniaturized lab-on-a-chip systems, and 3D cell culture models is extending the technology's use across diverse domains, including drug discovery, biomedical research, and clinical diagnostics. Furthermore, expanding healthcare infrastructure and strong R&D investments are accelerating the adoption of microfluidic technologies. Microfluidics, which involves manipulating extremely small fluid volumes within microscale channels, offers advantages such as precision control, low reagent consumption, and cost efficiency, making it indispensable for modern diagnostics and therapeutic development.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $31.5 Billion |

| Forecast Value | $124.2 Billion |

| CAGR | 14.8% |

The microfluidic chips and cartridges segment held 36.5% share in 2024, because of their critical role in enabling portable, efficient, and cost-effective diagnostic applications. These chips are vital for lab-on-a-chip systems and point-of-care testing, offering scalable solutions for decentralized healthcare settings. The rising adoption of microfluidic cartridges in regions with limited diagnostic infrastructure is further supporting this segment's growth, as these devices provide rapid, accurate results without requiring complex laboratory setups.

The in-vitro diagnostics segment held 42.1% share in 2024, fueled by increasing demand for affordable, precise, and high-throughput testing across chronic and infectious diseases. Microfluidic-based IVD solutions are widely used for liquid biopsies, genetic analyses, and infectious disease detection due to their multiplexing capabilities and exceptional sensitivity. Their integration into modern laboratory workflows enhances diagnostic efficiency while reducing turnaround times, contributing significantly to market expansion.

North America Microfluidics Market held a 43.5% share in 2024. The region's dominance stems from advanced healthcare systems, large-scale R&D spending, and strong adoption of innovative diagnostic technologies in the U.S. and Canada. Growing utilization of microfluidic platforms in research institutes, hospitals, and academic centers has created a fertile environment for continued technological development. Additionally, government-backed initiatives supporting molecular diagnostics, personalized medicine, and AI-based health analytics are further accelerating market penetration and enhancing the adoption of microfluidic devices across healthcare and life sciences sectors.

Key players active in the Global Microfluidics Market include Danaher, Illumina, Bio-Rad Laboratories, F. Hoffmann-La Roche, Qiagen, Becton Dickinson, Thermo Fisher Scientific, Agilent Technologies, bioMerieux, Bartels Mikrotechnik, Dolomite Microfluidics, Fluigent, Standard BioTools, PerkinElmer, Boston Pharmaceutical (Nanomix), Emulate, uFluidix, Sphere Fluidics, and Xona Microfluidics. To strengthen their foothold in the Global Microfluidics Market, major companies are focusing on product innovation, automation integration, and partnerships with diagnostic and pharmaceutical firms. Many are investing in the development of multifunctional lab-on-chip platforms, digital microfluidic systems, and scalable cartridge-based solutions designed for rapid, high-precision testing. Strategic collaborations between device manufacturers and biotechnology companies are helping expand product portfolios and accelerate clinical validation. Firms are also prioritizing miniaturization and connectivity to align with the growing trend of decentralized diagnostics and personalized medicine.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Technology trends

- 2.2.5 Material trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for point-of-care diagnostics

- 3.2.1.2 Expansion of personalized medicine and genomics

- 3.2.1.3 Integration with AI and digital health platforms

- 3.2.1.4 Advancements in microfabrication and materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and manufacturing costs

- 3.2.2.2 Regulatory and standardization hurdles

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in organ-on-chip and 3D cell culture platforms

- 3.2.3.2 Adoption in low-resource and decentralized settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Microfluidic chips and cartridges

- 5.3 Instruments and analyzers

- 5.4 Pumps, valves and sensors

- 5.5 Reagents and consumables

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pharmaceuticals

- 6.3 Medical devices

- 6.4 In-vitro diagnostics

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Lab-on-a-chip

- 7.3 Organs-on-chips

- 7.4 Continuous flow microfluidics

- 7.5 Other technologies

Chapter 8 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Silicon

- 8.3 Glass

- 8.4 Polymer

- 8.5 Other materials

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and diagnostic centers

- 9.3 Academic and research centers

- 9.4 Pharmaceutical and biotechnology companies

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Agilent Technologies

- 11.2 Bartels Mikrotechnik

- 11.3 Becton Dickinson

- 11.4 bioMerieux

- 11.5 Bio-Rad Laboratories

- 11.6 Boston Pharmaceutical (Nanomix)

- 11.7 Danaher

- 11.8 Dolomite Microfluidics

- 11.9 Emulate

- 11.10 F. Hoffmann-La Roche

- 11.11 Fluigent

- 11.12 Illumina

- 11.13 PerkinElmer

- 11.14 Qiagen

- 11.15 Sphere Fluidics

- 11.16 Standard BioTools

- 11.17 Thermo Fisher Scientific

- 11.18 uFluidix

- 11.19 Xona Microfluidics

数位微流体晶片市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材料类型、装置、製程、最终用户及解决方案划分

数位微流体晶片市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材料类型、装置、製程、最终用户及解决方案划分 微流体液滴晶片市场规模、份额和成长分析:按产品类型、应用领域、材料类型、最终用户、地区和产业预测,2026-2033年微流体市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、製程、最终用户、功能及安装类型划分

微流体液滴晶片市场规模、份额和成长分析:按产品类型、应用领域、材料类型、最终用户、地区和产业预测,2026-2033年微流体市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、製程、最终用户、功能及安装类型划分 全球微流体市场规模、份额、趋势和成长分析报告(2026-2034)

全球微流体市场规模、份额、趋势和成长分析报告(2026-2034) 全球微流体市场按产品、应用、最终用户和地区划分-预测至2030年

全球微流体市场按产品、应用、最终用户和地区划分-预测至2030年 2026年全球微流体市场报告

2026年全球微流体市场报告 微流体装置原型市场-全球产业规模、份额、趋势、机会及预测(按组件、应用、地区和竞争格局划分,2021-2031年)

微流体装置原型市场-全球产业规模、份额、趋势、机会及预测(按组件、应用、地区和竞争格局划分,2021-2031年) 微流体晶片解决方案市场按产品类型、材料和应用划分,全球预测(2026-2032年)液滴发生晶片市场:依发生机制、通道材料、流速、应用和最终用户划分,全球预测(2026-2032年)

微流体晶片解决方案市场按产品类型、材料和应用划分,全球预测(2026-2032年)液滴发生晶片市场:依发生机制、通道材料、流速、应用和最终用户划分,全球预测(2026-2032年) 日本微流控市场报告(按材料、组件、应用和地区划分,2026-2034年)

日本微流控市场报告(按材料、组件、应用和地区划分,2026-2034年)