|

市场调查报告书

商品编码

1876592

人工智慧驱动的视网膜筛检设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)AI-Driven Retinal Screening Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

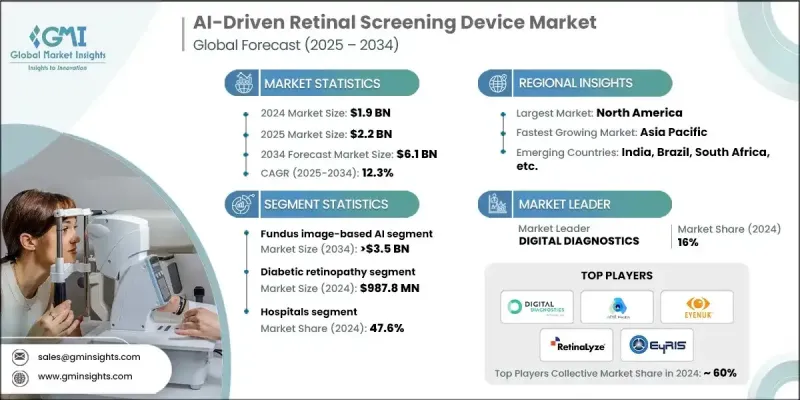

2024 年全球人工智慧驱动的视网膜筛检设备市场价值为 19 亿美元,预计到 2034 年将以 12.3% 的复合年增长率成长至 61 亿美元。

糖尿病盛行率上升、技术创新不断进步以及人工智慧医学影像工具的日益普及是推动这一成长的主要因素。政府和私人医疗系统支持的、不断扩大的宣传项目和筛检计划进一步刺激了市场需求。将人工智慧应用于视网膜诊断,能够实现精准的即时筛检,并有助于早期发现多种眼部疾病。随着医疗服务提供者转向预防性护理和远端诊断,人工智慧驱动的视网膜设备正成为改善全球眼部健康状况和提高医疗服务可近性(尤其是在资源匮乏地区)的关键工具。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 19亿美元 |

| 预测值 | 61亿美元 |

| 复合年增长率 | 12.3% |

深度学习演算法、影像技术和可携式诊断设备的进步显着提升了基于人工智慧的视网膜筛检系统的效能和易用性。这些设备现在能够提供即时分析,同时检测多种眼部疾病,并与数位健康记录系统无缝整合。小型化和云端成像工具的出现,使得视网膜筛检更加快速、经济,并在各种医疗机构中更容易进行。新一代人工智慧演算法日趋完善,能够辨识细微的视网膜变化,进而实现早期介入和个人化治疗方案的发展。这些演算法正与全球卫生组织、地方政府和医疗机构携手合作,进行宣传活动和大规模筛检,以对抗可预防的失明。配备人工智慧技术的行动诊断单元正在惠及服务不足的社区,而人工智慧筛检工具也被纳入常规体检,以加强早期发现和预防性眼部保健。人工智慧驱动的视网膜筛检设备依靠机器学习演算法来解读视网膜影像,从而准确、及时地识别主要眼部疾病,并提高高品质眼科诊断的可及性。

2024年,基于眼底影像的人工智慧(AI)市占率达到56.7%,预计到2034年将达到35亿美元,年复合成长率(CAGR)为12.7%。该领域的领先地位归功于人们对早期检测威胁视力的眼部疾病日益增长的需求。基于眼底影像的AI工具利用高解析度二维视网膜影像来检测表面异常,包括微动脉瘤、出血和视盘异常。这些模型经过训练,能够识别糖尿病视网膜病变和高血压视网膜病变等疾病,从而透过自动影像评估实现快速可靠的诊断。

2024年,糖尿病视网膜病变市场规模达9.878亿美元。作为糖尿病患者视力丧失的主要原因之一,糖尿病视网膜病变仍然是人工智慧驱动的筛检解决方案最常见的应用领域。这些设备能够快速、非侵入性地分析视网膜影像,无需专科医生干预即可在基层医疗机构有效运作。它们在糖尿病护理机构和社区诊所的应用极大地扩大了筛检覆盖范围,尤其是在眼科服务资源有限的地区。糖尿病视网膜病变的高发生率和可预防性使其成为该行业中最具影响力的细分市场。

预计到2024年,北美人工智慧驱动的视网膜筛检设备市占率将达到47.3%。该地区市场扩张的驱动力包括广泛的创新、先进的医疗保健生态系统以及对利用人工智慧技术加速诊断的高度重视。该地区完善的基础设施、对预防性眼保健的高度重视以及众多人工智慧医疗新创企业的存在,都为这些系统的稳步普及提供了支持。糖尿病和与老化相关的眼部疾病发生率的不断上升,也推动了对能够快速、准确地检测疾病的智慧视网膜筛检工具的需求。

全球人工智慧驱动型视网膜筛检设备市场的主要企业包括iCare、RetinaLyze、Heart Eye、EYENUK、Retmarker、Airdoc、AEYE Health、Evolucare、Topcon Healthcare、Remidio、MONA Health、Forus Health、Identifeye Health、Visionix、Digital Diagnostics和EyRIS。这些企业持续投资于技术创新和市场拓展,以巩固其全球地位。人工智慧驱动型视网膜筛检设备市场的领导者正采用多种策略来提升其竞争优势。其中一个重点是研发,旨在创建能够更精准地检测更多视网膜疾病的先进人工智慧演算法。许多公司正与医院、诊所和远距医疗服务提供者建立策略联盟,以扩大人工智慧筛检工具的部署。此外,各公司也致力于将其係统与电子健康记录平台集成,以实现无缝的临床工作流程。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 糖尿病盛行率不断上升

- 老年人口不断增加

- 技术进步

- 提高公众意识和筛检计划

- 产业陷阱与挑战

- 资料隐私和安全问题

- 严格的监管准则

- 机会

- 多病种检测平台开发

- 与行动医疗(mHealth)的整合

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 投资环境

- 报销方案

- 技术演进时间轴

- 新兴用例和应用

- 利用视网膜影像进行全身性疾病筛检

- 心血管风险评估

- 神经系统疾病检测

- 价值链分析

- 硬体製造商

- 人工智慧演算法开发人员

- 软体平台供应商

- 医疗保健服务提供者

- 最终用户整合合作伙伴

- 波特的分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 基于眼底影像的人工智慧

- 基于OCT的AI

- 多模态人工智慧

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 糖尿病视网膜病变

- 老年性黄斑部病变

- 青光眼

- 白内障

- 其他应用

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 医院

- 眼科诊所

- 流动诊所/乡村营地

- 其他最终用途

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AEYE Health

- Airdoc

- DIGITAL DIAGNOSTICS

- evolucare

- EYENUK

- EyRIS

- Forus Health

- HEART EYE

- iCare

- identifeye HEALTH

- MONA.health

- remidio

- RetinaLyze

- Retmarker

- Topcon Healthcare

- Visionix

The Global AI-Driven Retinal Screening Device Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 12.3% to reach USD 6.1 billion by 2034.

Rising diabetes prevalence, growing technological innovation, and increasing adoption of AI-based medical imaging tools are among the major forces driving this growth. Expanding awareness programs and screening initiatives, supported by government and private healthcare systems, are further propelling demand. The integration of artificial intelligence into retinal diagnostics enables precise, real-time screening and supports early detection of multiple eye conditions. As healthcare providers move toward preventive care and remote diagnostics, AI-powered retinal devices are becoming essential tools for improving global eye health outcomes and enhancing accessibility, especially in low-resource regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 12.3% |

Advancements in deep learning algorithms, imaging technologies, and portable diagnostic equipment have significantly enhanced the performance and usability of AI-based retinal screening systems. These devices now provide real-time analytics, detect multiple eye disorders simultaneously, and seamlessly integrate with digital health record systems. The emergence of compact and cloud-enabled imaging tools has made retinal screening faster, more affordable, and more accessible across various healthcare settings. Next-generation AI algorithms are becoming more refined, capable of identifying subtle retinal changes that allow for earlier interventions and personalized treatment planning. Alongside global health organizations, local authorities, and medical institutions, they are implementing awareness drives and mass screening campaigns to fight preventable blindness. Mobile diagnostic units with AI technology are reaching underserved communities, while AI screening tools are being incorporated into standard checkups to strengthen early detection and preventive eye care. AI-driven retinal screening devices rely on machine learning algorithms to interpret images of the retina, providing accurate and timely identification of major ocular diseases and improving accessibility to quality eye diagnostics.

In 2024, the fundus image-based AI segment held 56.7% and is projected to reach USD 3.5 billion by 2034, growing at a CAGR of 12.7%. This segment's dominance is attributed to the rising demand for early detection of vision-threatening eye diseases. Fundus image-based AI tools use high-resolution 2D retinal images to detect surface-level irregularities, including microaneurysms, hemorrhages, and optic disc abnormalities. These models are trained to recognize conditions such as diabetic and hypertensive retinopathy, enabling rapid and reliable diagnostics through automated image assessment.

The diabetic retinopathy segment reached USD 987.8 million in 2024. As one of the primary causes of vision loss among individuals with diabetes, diabetic retinopathy continues to be the most common application for AI-driven screening solutions. These devices deliver rapid, non-invasive analysis of retinal images and can function effectively in primary healthcare environments without requiring specialist intervention. Their implementation in diabetes care facilities and community clinics has greatly expanded screening outreach, particularly in regions with limited access to ophthalmology services. The high prevalence and preventable nature of diabetic retinopathy continue to make it the most influential segment within the industry.

North America AI-Driven Retinal Screening Device Market held a 47.3% share in 2024. Market expansion in the region is driven by widespread innovation, an advanced healthcare ecosystem, and a heightened focus on accelerating diagnosis using AI technologies. The region's established infrastructure, coupled with strong awareness of preventive eye health and the presence of numerous AI healthcare startups, supports steady adoption of these systems. A growing incidence of diabetes and aging-related eye conditions is also fueling demand for intelligent retinal screening tools capable of fast and accurate disease detection.

Prominent companies operating in the Global AI-Driven Retinal Screening Device Market include iCare, RetinaLyze, Heart Eye, EYENUK, Retmarker, Airdoc, AEYE Health, Evolucare, Topcon Healthcare, Remidio, and MONA. Health, Forus Health, Identifeye Health, Visionix, Digital Diagnostics, and EyRIS. These players continue to invest in technological innovation and market expansion to strengthen their global presence. Leading companies in the AI-driven retinal screening device market are employing multiple strategies to enhance their competitive position. A major focus lies in research and development to create advanced AI algorithms capable of detecting a wider range of retinal conditions with greater accuracy. Many firms are forming strategic alliances with hospitals, clinics, and telemedicine providers to expand the deployment of AI-based screening tools. Companies are also emphasizing the integration of their systems with electronic health record platforms to enable seamless clinical workflows.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes

- 3.2.1.2 Rising geriatric population

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 Stringent regulatory guidelines

- 3.2.3 Opportunities

- 3.2.3.1 Multi-disease detection platform development

- 3.2.3.2 Integration with mobile health (mHealth)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Investment landscape

- 3.7 Reimbursement scenario

- 3.8 Technology evolution timeline

- 3.9 Emerging use cases & applications

- 3.9.1 Systemic disease screening from retinal images

- 3.9.2 Cardiovascular risk assessment

- 3.9.3 Neurological condition detection

- 3.10 Value chain analysis

- 3.10.1 Hardware manufacturers

- 3.10.2 AI algorithm developers

- 3.10.3 Software platform providers

- 3.10.4 Healthcare service providers

- 3.10.5 End use integration partners

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Fundus image-based AI

- 5.3 OCT-based AI

- 5.4 Multi-modal AI

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diabetic retinopathy

- 6.3 Age-related macular degeneration

- 6.4 Glaucoma

- 6.5 Cataract

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ophthalmology clinics

- 7.4 Mobile clinics/Rural camps

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AEYE Health

- 9.2 Airdoc

- 9.3 DIGITAL DIAGNOSTICS

- 9.4 evolucare

- 9.5 EYENUK

- 9.6 EyRIS

- 9.7 Forus Health

- 9.8 HEART EYE

- 9.9 iCare

- 9.10 identifeye HEALTH

- 9.11 MONA.health

- 9.12 remidio

- 9.13 RetinaLyze

- 9.14 Retmarker

- 9.15 Topcon Healthcare

- 9.16 Visionix

卵巢癌诊断市场:依技术、产品、通路和应用划分-2026-2032年全球市场预测多癌种筛检市场:按检测类型、癌症类型、技术、支付方式、应用和最终用户划分-2026-2032年全球市场预测

卵巢癌诊断市场:依技术、产品、通路和应用划分-2026-2032年全球市场预测多癌种筛检市场:按检测类型、癌症类型、技术、支付方式、应用和最终用户划分-2026-2032年全球市场预测 肺癌筛检市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

肺癌筛检市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 卵巢癌诊断市场规模、份额和成长分析:按癌症类型、检测类型和地区划分-2026-2033年产业预测

卵巢癌诊断市场规模、份额和成长分析:按癌症类型、检测类型和地区划分-2026-2033年产业预测 2026年全球卵巢癌诊断市场报告

2026年全球卵巢癌诊断市场报告 卵巢癌诊断市场-全球产业规模、份额、趋势、机会及预测(按诊断类型、癌症类型、最终用户、地区和竞争格局划分,2021-2031年)人工智慧眼底筛检系统市场:2026-2032年全球预测(按硬体、软体、服务、部署类型、应用程式和最终用户划分)犬类癌症筛检市场:按产品类型、技术、癌症类型、检体类型和最终用户划分 - 全球预测(2026-2032 年)

卵巢癌诊断市场-全球产业规模、份额、趋势、机会及预测(按诊断类型、癌症类型、最终用户、地区和竞争格局划分,2021-2031年)人工智慧眼底筛检系统市场:2026-2032年全球预测(按硬体、软体、服务、部署类型、应用程式和最终用户划分)犬类癌症筛检市场:按产品类型、技术、癌症类型、检体类型和最终用户划分 - 全球预测(2026-2032 年) 肺癌筛检市场规模、份额和成长分析(按癌症类型、诊断方法、最终用户和地区划分)—2026-2033年产业预测2025年肺癌筛检全球市场报告

肺癌筛检市场规模、份额和成长分析(按癌症类型、诊断方法、最终用户和地区划分)—2026-2033年产业预测2025年肺癌筛检全球市场报告