|

市场调查报告书

商品编码

1876615

汽车生物辨识感测器半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Biometric Sensor Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

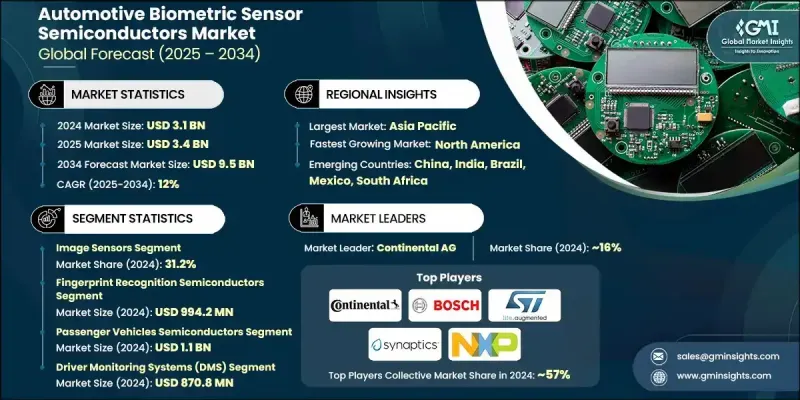

2024 年全球汽车生物辨识感测器半导体市场价值为 31 亿美元,预计到 2034 年将以 12% 的复合年增长率成长至 95 亿美元。

对先进车辆安全、驾驶员安全和个人化车内体验日益增长的需求,正在推动汽车生物识别感测器半导体的应用。汽车製造商正迅速整合指纹、脸部和虹膜辨识技术,以加强门禁控制、点火系统和驾驶员识别。在人工智慧驱动的身份验证支援下,互联智慧汽车的兴起正在加速市场成长。随着车辆失窃案件的增加以及对驾驶员监控的日益重视,汽车製造商正在利用这些基于半导体的生物识别系统来防止未经授权的进入,并透过客製化座椅、空调和资讯娱乐设置来提升用户体验。高级驾驶辅助系统 (ADAS) 的日益普及也推动了对生物辨识感测解决方案的需求,这些解决方案利用脸部辨识和眼动追踪功能来监测驾驶者的疲劳程度、注意力集中程度和情绪状态。强调驾驶员安全和减少事故的监管措施正在鼓励这些技术的更广泛应用。随着车辆向数位化生态系统演进,基于半导体的生物辨识身分验证正成为实现安全存取、资讯娱乐控制和数位支付系统的核心,并确立其作为下一代汽车架构关键要素的地位。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 31亿美元 |

| 预测值 | 95亿美元 |

| 复合年增长率 | 12% |

到2024年,影像感测器市场份额将达到31.2%,引领全球汽车生物辨识感测器半导体市场。影像感测器在人脸、虹膜和手势辨识方面发挥着至关重要的作用,这些技术可用于驾驶员监控和身份验证。这些感测器能够捕捉高解析度影像,用于检测驾驶员的疲劳程度、注意力水平和行为模式。 CMOS和红外线成像技术的不断进步提高了灵敏度、精度和处理效率,推动了电动车、连网汽车和自动驾驶汽车等需要强大车内监控和自适应安全系统的车辆对影像感测器的应用。

2024年,指纹辨识半导体市场规模达9.942亿美元,占最大市场。指纹辨识晶片广泛应用于车辆门禁系统、点火模组和驾驶个人化设定等领域。与其他生物辨识方式相比,指纹辨识晶片具有高精度、低延迟和成本效益等优势。随着电容式和超音波指纹辨识技术的进步,指纹辨识晶片在豪华车和中檔车的应用日益广泛。紧凑的设计、低功耗和可靠的性能,使得这些半导体成为注重安全性和用户便利性的现代智慧网联汽车应用的关键组件。

2024年,北美汽车生物辨识感测器半导体市场占据29.4%的市场。该地区的成长得益于驾驶员监控技术、指纹和脸部辨识系统以及先进的车内安全解决方案的广泛应用。消费者对更高安全性和个人化驾驶体验的需求不断增长,加上鼓励驾驶注意力监控的监管措施,正在增强区域市场的成长动能。主要半导体和汽车电子公司的强大实力,以及人工智慧成像、红外线感测和嵌入式资料保护的突破,持续巩固北美在汽车生物辨识创新领域的领先地位。

全球汽车生物辨识感测器半导体市场的主要参与者包括 Synaptics Incorporated、Fingerprint Cards AB、Gentex Corporation、Fujitsu Limited、Continental AG、NXP Semiconductors NV、Harman International Industries、IDEMIA、HID Global Corporation、Aware Inc.、Infineon Technologies AG、Texas Instruics Inc.、ams OSRAM AG、Qualcomm Technologies, Inc.、Robert Bosch GmbH 和 Precise Biometrics AB。这些领导企业正致力于透过技术创新、合作和产品多元化来巩固其市场地位。许多企业正大力投资研发,以提升基于人工智慧的身份验证、低功耗晶片性能以及感测器在各种环境条件下的精度。半导体製造商与汽车製造商之间的策略合作旨在将下一代生物识别解决方案整合到互联汽车和电动汽车中。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 对先进的车辆安全和防盗系统的需求日益增长。

- 驾驶员监控系统在高阶驾驶辅助系统中的整合度日益提高。

- 透过生物辨识技术,提高车内个人化体验的使用率。

- 人工智慧赋能的生物辨识技术取得了进展。

- 产业陷阱与挑战

- 生物辨识系统的製造成本和整合成本很高。

- 对生物识别资料隐私和网路安全风险的担忧。

- 市场机会

- 扩展互联自动驾驶汽车生态系统。

- 开发基于边缘人工智慧的生物辨识处理晶片。

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

- 技术格局

- 当前趋势

- 新兴技术

- 管道分析

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 影像感测器

- 处理单元

- 安全组件

- 类比元件

- 记忆体组件

第六章:市场估算与预测:依技术类型划分,2021-2034年

- 主要趋势

- 指纹辨识半导体

- 脸部辨识半导体

- 虹膜识别半导体

- 语音辨识半导体

- 多模态生物特征半导体

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 搭乘用车

- 商用车辆

- 电动车

- 自动驾驶汽车

第八章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 驾驶员监控系统(DMS)

- 车辆出入控制

- 个人化系统

- 安全系统

- 车载支付认证

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Continental AG

- Hyundai Mobis

- Valeo SA

- Gentex Corporation

- Robert Bosch GmbH

- Harman International Industries

- Synaptics Incorporated

- Fingerprint Cards AB

- Fujitsu Limited

- Cerence Inc.

- IDEMIA

- STMicroelectronics NV

- Texas Instruments Incorporated

- Qualcomm Technologies, Inc.

- Infineon Technologies AG

- NXP Semiconductors NV

- ams OSRAM AG

- HID Global Corporation

- Precise Biometrics AB

- Aware Inc.

The Global Automotive Biometric Sensor Semiconductors Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 12% to reach USD 9.5 billion by 2034.

The rising demand for advanced vehicle security, driver safety, and personalized in-cabin experiences is fueling the adoption of automotive biometric sensor semiconductors. Automakers are rapidly incorporating fingerprint, facial, and iris recognition technologies to strengthen access control, ignition systems, and driver identification. The shift toward connected and intelligent vehicles, supported by AI-driven authentication, is accelerating market growth. With increasing cases of vehicle theft and a growing emphasis on driver monitoring, automakers are leveraging these semiconductor-based biometric systems to prevent unauthorized entry while enhancing user experience through customized seat, climate, and infotainment settings. The growing integration of Advanced Driver Assistance Systems (ADAS) is also boosting demand for biometric sensing solutions that track driver fatigue, focus, and emotion using facial recognition and eye-tracking capabilities. Regulatory initiatives emphasizing driver safety and accident reduction are encouraging broader use of these technologies. As vehicles evolve into digital ecosystems, semiconductor-based biometric authentication is becoming central to enabling secure access, infotainment control, and digital payment systems, establishing itself as a key element in next-generation automotive architecture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $9.5 Billion |

| CAGR | 12% |

The image sensors segment held a 31.2% share in 2024, leading the global automotive biometric sensor semiconductors market. Image sensors play a crucial role in enabling facial, iris, and gesture recognition used for both driver monitoring and authentication. These sensors capture high-resolution imagery necessary for detecting driver drowsiness, attention, and behavioral patterns. Ongoing advances in CMOS and infrared imaging have improved sensitivity, precision, and processing efficiency, driving adoption across electric, connected, and autonomous vehicles that require robust in-cabin monitoring and adaptive safety systems.

The fingerprint recognition semiconductor segment generated USD 994.2 million in 2024, holding the largest share in the market. Fingerprint recognition chips are widely utilized in vehicle access systems, ignition modules, and driver-specific customization settings. They provide high accuracy, low latency, and cost efficiency compared with other biometric modalities. Their integration in both luxury and mid-range vehicles is increasing, driven by advancements in capacitive and ultrasonic fingerprint technologies. Compact designs, low power consumption, and reliable performance have made these semiconductors essential for modern connected car applications focused on security and user convenience.

North America Automotive Biometric Sensor Semiconductors Market held a 29.4% share in 2024. The region's growth is supported by the widespread adoption of driver monitoring technologies, fingerprint and facial recognition systems, and advanced in-cabin safety solutions. Rising consumer demand for enhanced security and personalized driving experiences, coupled with regulatory measures encouraging driver attention monitoring, is strengthening regional market momentum. The strong presence of major semiconductor and automotive electronics companies, along with breakthroughs in AI-powered imaging, infrared sensing, and embedded data protection, continues to reinforce North America's leadership in automotive biometric innovation.

Prominent companies operating in the Global Automotive Biometric Sensor Semiconductors Market include Synaptics Incorporated, Fingerprint Cards AB, Gentex Corporation, Fujitsu Limited, Continental AG, NXP Semiconductors N.V., Harman International Industries, IDEMIA, HID Global Corporation, Aware Inc., Infineon Technologies AG, Texas Instruments Incorporated, Valeo SA, STMicroelectronics N.V., Hyundai Mobis, Cerence Inc., ams OSRAM AG, Qualcomm Technologies, Inc., Robert Bosch GmbH, and Precise Biometrics AB. Leading participants in the Automotive Biometric Sensor Semiconductors Market are pursuing strategies centered on technological innovation, partnerships, and product diversification to strengthen their market position. Many are investing heavily in research and development to enhance AI-based authentication, low-power chip performance, and sensor accuracy under diverse environmental conditions. Strategic collaborations between semiconductor manufacturers and automakers aim to integrate next-generation biometric solutions into connected and electric vehicles.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional Trends

- 2.2.2 Component Trends

- 2.2.3 Technology Type Trends

- 2.2.4 Vehicle Type Trends

- 2.2.5 Application Trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for advanced vehicle security and anti-theft systems.

- 3.2.1.2 Rising integration of driver monitoring systems in ADAS.

- 3.2.1.3 Increasing use of personalized in-vehicle experiences through biometrics.

- 3.2.1.4 Advancements in AI-enabled biometric recognition technologies.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and integration costs for biometric systems.

- 3.2.2.2 Concerns over biometric data privacy and cybersecurity risks.

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of connected and autonomous vehicle ecosystems.

- 3.2.3.2 Development of edge AI-based biometric processing chips.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Image Sensors

- 5.3 Processing Units

- 5.4 Security Components

- 5.5 Analog Components

- 5.6 Memory Components

Chapter 6 Market Estimates and Forecast, By Technology Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fingerprint Recognition Semiconductors

- 6.3 Facial Recognition Semiconductors

- 6.4 Iris Recognition Semiconductors

- 6.5 Voice Recognition Semiconductors

- 6.6 Multimodal Biometric Semiconductors

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Passenger Vehicles

- 7.3 Commercial Vehicles

- 7.4 Electric Vehicles

- 7.5 Autonomous Vehicles

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Driver Monitoring Systems (DMS)

- 8.3 Vehicle Access Control

- 8.4 Personalization Systems

- 8.5 Safety & Security Systems

- 8.6 In-Vehicle Payment Authentication

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Continental AG

- 10.2 Hyundai Mobis

- 10.3 Valeo SA

- 10.4 Gentex Corporation

- 10.5 Robert Bosch GmbH

- 10.6 Harman International Industries

- 10.7 Synaptics Incorporated

- 10.8 Fingerprint Cards AB

- 10.9 Fujitsu Limited

- 10.10 Cerence Inc.

- 10.11 IDEMIA

- 10.12 STMicroelectronics N.V.

- 10.13 Texas Instruments Incorporated

- 10.14 Qualcomm Technologies, Inc.

- 10.15 Infineon Technologies AG

- 10.16 NXP Semiconductors N.V.

- 10.17 ams OSRAM AG

- 10.18 HID Global Corporation

- 10.19 Precise Biometrics AB

- 10.20 Aware Inc.