|

市场调查报告书

商品编码

1876625

汽车影像讯号处理器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Image Signal Processor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球汽车影像讯号处理器市场价值为 21.5 亿美元,预计到 2034 年将以 16.1% 的复合年增长率成长至 93.7 亿美元。

现代汽车中智慧成像技术的日益普及正在改变汽车影像处理器(ISP)的格局。先进的ISP能够即时处理来自多个摄影机的影像,支援物体侦测、车道追踪和360度全景影像系统等关键功能。这些处理器即使在光线和天气条件恶劣的情况下也能提供超低延迟、高动态范围和可靠的性能,从而促进更安全、更节能的车辆运行。向自动化和软体定义车辆架构的持续演进正在加强高性能ISP的整合。半导体製造商、汽车製造商和人工智慧软体公司之间的策略合作也在推动人工智慧驱动的影像处理技术的发展,以增强驾驶辅助和感知系统。与晶片製造商和摄影机模组供应商的合作正在优化集中式电子设计中的热管理、图像品质和系统集成,帮助汽车製造商提高安全性、舒适性和自动驾驶水平。随着车辆向智慧出行生态系统转型,ISP正成为下一代高阶驾驶辅助系统(ADAS)和自动驾驶平台的关键组件。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 21.5亿美元 |

| 预测值 | 93.7亿美元 |

| 复合年增长率 | 16.1% |

2024年,现场可程式闸阵列(FPGA)市占率达到42%,预计到2034年将以14.9%的复合年增长率成长。基于FPGA的处理器凭藉其可重构架构、可扩展性和卓越的平行运算效能,在汽车ISP市场占据主导地位。它们使汽车製造商无需进行大规模硬体重新设计,即可整合用于驾驶员监控、物体侦测和车道保持等应用的高级影像处理演算法。此外,它们对不断变化的摄影机和感知需求的适应性也缩短了产品上市时间,使其成为下一代ADAS和自动驾驶汽车开发的关键。

2024年,OEM厂商占据了63%的市场。原始设备製造商是汽车影像处理器(ISP)的主要采用者,因为他们在生产过程中将这些处理器直接整合到新车型中。这确保了影像系统能够发挥最佳性能,满足安全法规要求,并实现可靠运作。随着汽车製造商部署高解析度摄影机、感测器融合技术和即时影像分析来增强高级驾驶辅助系统(ADAS)功能并提高驾驶安全性,原厂安装ISP的趋势日益明显。多摄影机配置和先进感知功能的日益普及也进一步推动了全球OEM厂商对ISP的采用。

预计到2024年,中国汽车影像讯号处理器(ISP)市场将占据39%的份额,市场规模达3.249亿美元。凭藉强大的汽车电子和半导体製造生态系统,中国在该区域市场保持主导地位。国内主要汽车製造商快速部署高级驾驶辅助系统(ADAS)和半自动驾驶技术,大大推动了对ISP的需求。政府鼓励智慧汽车和晶片设计创新的支持性政策,进一步加速了市场成长。中国致力于推动本土半导体生产和智慧出行解决方案,这将持续巩固其在汽车ISP领域的领先地位。

全球汽车影像讯号处理器市场的主要参与者包括德州仪器 (TI)、安森美半导体 (ON Semiconductor)、瑞萨电子 (Renesas Electronics)、亚德诺半导体 (ADI)、意法半导体 (STMicroelectronics)、Arm Limited、恩智浦半导体 (NXP)、Hparty-pimimel) OmniVision Technologies。汽车影像讯号处理器市场的领导企业正采取多管齐下的策略来巩固其竞争地位。许多企业致力于将人工智慧驱动的成像功能、边缘处理和即时电脑视觉增强技术整合到其影像讯号处理器 (ISP) 架构中。各公司正与汽车製造商和软体公司建立合作关係,共同开发针对高级驾驶辅助系统 (ADAS)、自动驾驶和车内监控等应用优化的客製化 ISP 平台。研发投入正集中于低功耗设计、先进的散热解决方案以及增强的摄影机同步功能,以支援多感测器融合。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- ADAS和自动驾驶汽车研发的激增

- 高解析度汽车摄影机的扩展

- 车辆安全法规日益增多

- 电动车普及率不断提高,智慧驾驶舱功能日益增强

- 产业陷阱与挑战

- 高昂的开发和整合成本

- 软体和感测器校准的复杂性

- 市场机会

- 软体定义车辆的出现

- 车队和商用车分析的成长

- 在两轮车和入门级车辆的应用

- 原始设备製造商和半导体公司之间的合作

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利分析

- 价格趋势

- 按地区

- 按组件

- 成本細項分析

- 商业案例及投资报酬率分析

- 总拥有成本框架

- 投资报酬率计算方法

- 实施时间表和里程碑

- 风险评估与缓解策略

- 永续性和环境影响分析

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来展望与机会

- 技术演进与下一代网际网路服务供应商架构

- 人工智慧和机器学习整合趋势

- 边缘运算与分散式处理模型

3.14.4. 5G 连接与车联网 (V2X) 集成

- 永续性和环境影响考量

- 监理演变与全球协调趋势

- 市场整合与产业结构变化

- 新兴应用及用例开发

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 硬体

- 模拟前端

- 影像感测器

- 讯号处理核心

- 记忆

- 输出介面

- 软体

- 服务

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- ADAS系统

- 自动驾驶汽车

- 停车辅助/后视/环视

- 夜视系统

- 驾驶员监控系统

- 其他的

第七章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 数位讯号处理(DSP)

- 现场可程式闸阵列(FPGA)

- 专用积体电路(ASIC)

第八章:市场估算与预测:依类型划分,2021-2034年

- 主要趋势

- 独立影像讯号处理器

- 整合影像讯号处理器

第九章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- OEM

- 售后市场

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- 全球参与者

- ARM

- Broadcom

- Cirrus Logic

- Fujitsu

- Infineon Technologies

- Intel (Mobileye)

- Microchip Technology

- Nikon

- NVIDIA

- NXP Semiconductors

- Olympus

- OmniVision Technologies

- Qualcomm Technologies

- Renesas Electronics

- Sony Semiconductor Solutions

- STMicroelectronics

- Texas Instruments

- ON Semiconductor

- Analog Devices

- 区域玩家

- Allwinner Technology

- Amlogic

- HiSilicon Technologies

- MediaTek

- Rockchip Electronics

- 新兴参与者

11.3.1. 10x工程师

- Cadence 设计系统

- 电子经济系统

- 影像品质实验室

- 独立半导体

- 创新磁碟

- 晶格半导体

- 豹子影像

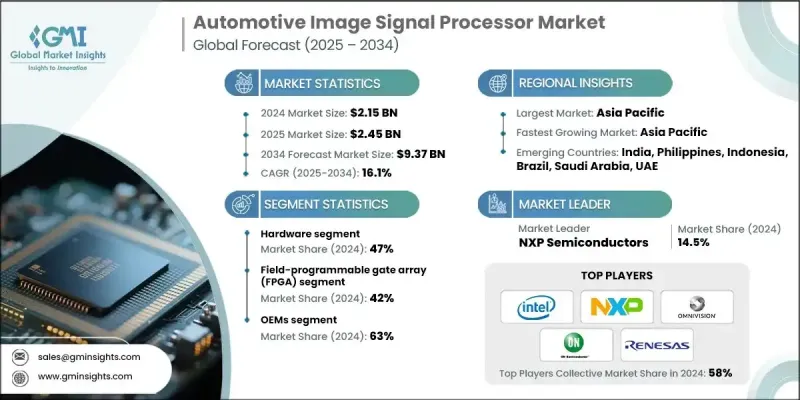

The Global Automotive Image Signal Processor Market was valued at USD 2.15 billion in 2024 and is estimated to grow at a CAGR of 16.1% to reach USD 9.37 billion by 2034.

The rising use of intelligent imaging technologies in modern vehicles is transforming the landscape of automotive ISPs. Advanced ISPs now enable real-time image processing from multiple cameras, supporting key functions such as object detection, lane tracking, and 360-degree view systems. These processors deliver ultra-low latency, high dynamic range, and dependable performance even in challenging lighting and weather conditions, fostering safer and more energy-efficient vehicle operations. The ongoing evolution toward automated and software-defined vehicle architectures is strengthening the integration of high-performance ISPs. Strategic collaborations between semiconductor manufacturers, automakers, and AI software companies are also advancing AI-driven image processing for enhanced driver-assistance and perception systems. Partnerships with chipmakers and camera module suppliers are optimizing thermal management, image quality, and system integration in centralized electronic designs, helping automakers improve safety, comfort, and autonomy levels. As vehicles transition toward intelligent mobility ecosystems, ISPs are becoming critical components in next-generation ADAS and autonomous driving platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.15 Billion |

| Forecast Value | $9.37 Billion |

| CAGR | 16.1% |

The field-programmable gate array (FPGA) segment held a 42% share in 2024 and is anticipated to grow at a CAGR of 14.9% through 2034. FPGA-based processors dominate the automotive ISP market due to their reconfigurable architecture, scalability, and superior parallel computing performance. They enable vehicle manufacturers to integrate advanced image-processing algorithms for applications such as driver monitoring, object detection, and lane-keeping without extensive hardware redesign. Their adaptability to changing camera and perception requirements also reduces time-to-market, making them essential for next-generation ADAS and autonomous vehicle development.

In 2024, the OEMs segment held a 63% share. Original equipment manufacturers are the leading adopters of automotive ISPs because they directly integrate these processors into new vehicle models during production. This ensures that imaging systems perform optimally, meet safety regulations, and deliver reliable operation. The preference for factory-installed ISPs is increasing as automakers deploy high-resolution cameras, sensor-fusion technologies, and real-time image analysis to enhance ADAS capabilities and improve driver safety. The growing use of multi-camera configurations and advanced perception features further supports ISP adoption among global OEMs.

China Automotive Image Signal Processor Market held a 39% share in 2024, generating USD 324.9 million. The country maintains a dominant position in the region due to its strong automotive electronics and semiconductor manufacturing ecosystem. Rapid implementation of ADAS and semi-autonomous technologies by major domestic automakers has fueled significant demand for ISPs. Supportive government programs encouraging innovation in smart vehicles and chip design are further accelerating market growth. China's commitment to advancing local semiconductor production and intelligent mobility solutions continues to reinforce its leadership in the automotive ISP space.

Key industry participants in the Global Automotive Image Signal Processor Market include Texas Instruments, ON Semiconductor, Renesas Electronics, Analog Devices, STMicroelectronics, Arm Limited, NXP Semiconductors, Microchip Technology, Intel (Mobileye), and OmniVision Technologies. Leading players in the Automotive Image Signal Processor Market are adopting multi-faceted strategies to strengthen their competitive positioning. Many are focusing on integrating AI-driven imaging capabilities, edge processing, and real-time computer vision enhancements into their ISP architectures. Companies are forming partnerships with automakers and software firms to co-develop customized ISP platforms optimized for ADAS, autonomous driving, and in-cabin monitoring. R&D investments are being directed toward low-power designs, advanced thermal solutions, and enhanced camera synchronization to support multi-sensor fusion.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 Technology

- 2.2.5 End Use

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in ADAS and autonomous vehicle development

- 3.2.1.2 Expansion of high-resolution automotive cameras

- 3.2.1.3 Rise in vehicle safety regulations

- 3.2.1.4 Growing EV adoption and smart cockpit features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs

- 3.2.2.2 Complexity in software and sensor calibration

- 3.2.3 Market opportunities

- 3.2.3.1 Emergence of software-defined vehicles

- 3.2.3.2 Growth in fleet and commercial vehicle analytics

- 3.2.3.3 Adoption in two-wheelers and entry-level vehicles

- 3.2.3.4 Collaborations between OEMs and semiconductor firms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Cost breakdown analysis

- 3.11 Business Case & ROI Analysis

- 3.11.1 Total cost of ownership framework

- 3.11.2 ROI calculation methodologies

- 3.11.3 Implementation timeline & milestones

- 3.11.4 Risk assessment & mitigation strategies

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

- 3.14 Future outlook & opportunities

- 3.14.1 Technology evolution & next-generation ISP architectures

- 3.14.2 AI & machine learning integration trends

- 3.14.3 Edge computing & distributed processing models

3.14.4. 5G connectivity & vehicle-to-everything (V2X) integration

- 3.14.5 Sustainability & environmental impact considerations

- 3.14.6 Regulatory evolution & global harmonization trends

- 3.14.7 Market consolidation & industry structure changes

- 3.14.8 Emerging applications & use case development

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LAMEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Analog Front-End

- 5.2.2 Image Sensor

- 5.2.3 Signal Processing Core

- 5.2.4 Memory

- 5.2.5 Output Interface

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ADAS Systems

- 6.3 Autonomous Vehicles

- 6.4 Parking Assistance / Rear-View / Surround View

- 6.5 Night Vision Systems

- 6.6 Driver Monitoring Systems

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Digital signal processing (DSP)

- 7.3 Field-programmable gate array (FPGA)

- 7.4 Application-specific integrated circuits (ASIC)

Chapter 8 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Standalone image signal processors

- 8.3 Integrated image signal processors

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ARM

- 11.1.2 Broadcom

- 11.1.3 Cirrus Logic

- 11.1.4 Fujitsu

- 11.1.5 Infineon Technologies

- 11.1.6 Intel (Mobileye)

- 11.1.7 Microchip Technology

- 11.1.8 Nikon

- 11.1.9 NVIDIA

- 11.1.10 NXP Semiconductors

- 11.1.11 Olympus

- 11.1.12 OmniVision Technologies

- 11.1.13 Qualcomm Technologies

- 11.1.14 Renesas Electronics

- 11.1.15 Sony Semiconductor Solutions

- 11.1.16 STMicroelectronics

- 11.1.17 Texas Instruments

- 11.1.18 ON Semiconductor

- 11.1.19 Analog Devices

- 11.2 Regional Players

- 11.2.1 Allwinner Technology

- 11.2.2 Amlogic

- 11.2.3 HiSilicon Technologies

- 11.2.4 MediaTek

- 11.2.5 Rockchip Electronics

- 11.3 Emerging Players

11.3.1. 10xEngineers

- 11.3.2 Cadence Design Systems

- 11.3.3 e-con Systems

- 11.3.4 Image Quality Labs

- 11.3.5 Indie Semiconductor

- 11.3.6 Innodisk

- 11.3.7 Lattice Semiconductor

- 11.3.8 Leopard Imaging

汽车电子编程系统市场:按车辆类型、技术、工具类型、最终用途、部署模式和应用划分,全球预测,2026-2032年

汽车电子编程系统市场:按车辆类型、技术、工具类型、最终用途、部署模式和应用划分,全球预测,2026-2032年 全球汽车电子元件市场:按应用、销售管道、动力方式、车辆类型、类型、国家和地区划分-产业分析、市场规模、份额及2025年至2032年未来预测汽车偏光滤镜市场:按材料、偏光滤镜类型、车辆类型、应用和销售管道,全球预测,2026-2032年汽车级胎压监测晶片市场:按应用、类型、车辆类型和技术分類的全球预测(2026-2032年)车用级蓝牙晶片市场:按应用、晶片类型、整合类型、车辆类型、分销管道和范围划分 - 全球预测,2026-2032年

全球汽车电子元件市场:按应用、销售管道、动力方式、车辆类型、类型、国家和地区划分-产业分析、市场规模、份额及2025年至2032年未来预测汽车偏光滤镜市场:按材料、偏光滤镜类型、车辆类型、应用和销售管道,全球预测,2026-2032年汽车级胎压监测晶片市场:按应用、类型、车辆类型和技术分類的全球预测(2026-2032年)车用级蓝牙晶片市场:按应用、晶片类型、整合类型、车辆类型、分销管道和范围划分 - 全球预测,2026-2032年 全球汽车电子市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车电子市场规模、份额、趋势和成长分析报告(2026-2034) 汽车电子导电塑胶市场:市场机会、成长要素、产业趋势分析及2026-2035年预测

汽车电子导电塑胶市场:市场机会、成长要素、产业趋势分析及2026-2035年预测 日本汽车电子市场规模、份额、趋势和预测:按零件、车辆类型、分销管道、应用和地区划分,2026-2034年汽车电子市场规模、份额、趋势及预测(按组件、车辆类型、通路、应用和地区划分),2026-2034年

日本汽车电子市场规模、份额、趋势和预测:按零件、车辆类型、分销管道、应用和地区划分,2026-2034年汽车电子市场规模、份额、趋势及预测(按组件、车辆类型、通路、应用和地区划分),2026-2034年 2026年全球汽车引擎盖下电子设备市场报告

2026年全球汽车引擎盖下电子设备市场报告