|

市场调查报告书

商品编码

1876631

汽车氢气感测器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Hydrogen Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

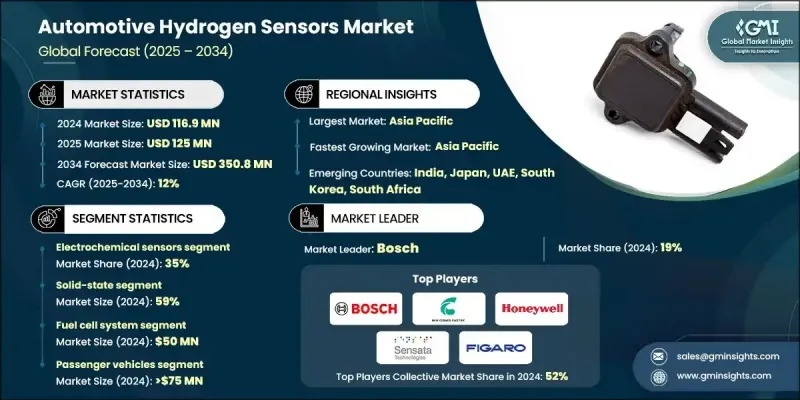

2024 年全球汽车氢气感测器市场价值为 1.169 亿美元,预计到 2034 年将以 12% 的复合年增长率增长至 3.508 亿美元。

氢燃料电池汽车需求的不断增长,以及日益严格的安全法规,正在加速汽车氢感测器产业的成长。这些感测器是关键部件,用于检测氢气洩漏、监测燃料电池性能,并确保氢动力车辆的整体安全。市场上有许多感测技术,例如电化学感测器、催化燃烧感测器、热导率感测器和金属氧化物半导体感测器,每种技术都满足不同的汽车需求。氢燃料加註网路的持续发展,不仅推动了车辆氢感测器的应用,也促进了整个氢供应链中氢感测器的应用。对氢动力交通工具(尤其是商用车)投资的增加,进一步推动了市场扩张。儘管新冠疫情初期由于供应链受阻和工业活动减少,导致生产中断和研发项目延误,但最终却成为支持氢能和安全发展的政策倡议的催化剂,从而为市场復苏和技术创新註入了新的动力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.169亿美元 |

| 预测值 | 3.508亿美元 |

| 复合年增长率 | 12% |

2024年,电化学感测器市占率达到35%,预计2025年至2034年将以10.2%的复合年增长率成长。该细分市场持续占据主导地位,主要得益于其高精度、高灵敏度和快速反应能力,这些特性对于安全至关重要的汽车系统而言必不可少。电化学感测器的工作原理是利用电解液中的铂基电极,产生与环境中氢气浓度成正比的电讯号。它们能够在数秒内检测到低至1 ppm的氢气浓度,使其成为对精度和可靠性要求极高的监测应用的理想选择。

固态感测器市场占有率高达59%,预计在2025年至2034年间将维持14%的强劲复合年增长率。其市场主导地位归功于其耐用性、紧凑的设计和免维护运行,这些特性符合现代汽车对可靠耐用组件的需求。这些感测器利用微机电系统(MEMS)和薄膜半导体技术,打造出整合先进讯号处理和通讯功能的微型感测元件。这种方法提高了燃料电池和排放监测系统中氢气检测的可靠性和效率。

亚太地区汽车氢气感测器市场占据51.6%的市场份额,预计到2034年将以13%的复合年增长率成长。该地区的成长主要得益于政府对氢能基础设施的大规模公共投资、对零排放出行的强有力政策支持以及氢动力汽车的快速商业化。预计该地区对氢燃料应用的战略重点将使其在整个预测期内保持领先地位。

汽车氢气感测器市场的主要参与者包括霍尼韦尔、博世、安费诺感测器、大陆集团、英飞凌科技、森萨塔科技、新宇宙电气、菲加罗工程、日产FIS和森赛瑞恩。活跃于汽车氢气感测器市场的企业正在实施创新驱动型策略,以加强其全球影响力。他们大力投资研发,致力于打造小型化、节能高效且经济实惠的感测器解决方案,以满足氢动力汽车的需求。汽车原始设备製造商 (OEM) 与感测器製造商之间的策略合作正在加速产品开发週期,并提升燃料电池系统中的技术整合。此外,各公司也正在拓展区域分销网络和扩大生产能力,以满足新兴氢能经济体日益增长的需求。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 专业气体感测器製造商

- 多元化工业电子集团

- 汽车专用感测器供应商

- 化学及先进材料公司

- 专业的氢能和燃料电池技术专家

- 成本结构

- 利润率

- 每个阶段的价值增加

- 影响供应链的因素

- 颠覆者

- 供应商格局

- 对力的影响

- 成长驱动因素

- 全球大力发展绿氢燃料电池电动车

- 扩大氢气加註基础设施

- 严格的安全标准和政府指令

- 感测器技术的进步

- 产业陷阱与挑战

- 先进感测器技术成本高昂

- 技术和性能挑战

- 市场机会

- 与物联网和预测性维护的集成

- 氢动力商用车的成长

- 成长驱动因素

- 技术趋势与创新生态系统

- 目前技术

- 量子点感测器

- 无线感测器网路

- 基于石墨烯的检测

- 预测性维护系统

- 新兴技术

- 机器学习集成

- 区块链保障资料完整性

- 扩增实境介面

- 人工智慧驱动的智慧感测器

- 目前技术

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 成本細項分析

- 专利格局

- 专利组合分析

- 关键专利族

- 专利到期分析

- 智慧财产权策略与许可

- 价格趋势

- 成本加成定价模式

- 获利提升策略

- 製造费用

- 销售与价格的关係

- 产品线及研发路线图

- 技术开发时间表

- 短期发展规划(2024-2026)

- 中期创新(2027-2030 年)

- 长期突破(2031-2034 年)

- 登月科技(2034)

- 产品开发阶段

- 概念和可行性研究

- 原型开发

- 试点测试与验证

- 商业发布准备

- 研发投资分析

- 企业研发支出

- 政府资助项目

- 学术研究计划

- 公私合营

- 技术准备度评估

- 技术成熟度等级(TRL)映射

- 商业化时程

- 可扩展性挑战

- 市场准入壁垒

- 技术开发时间表

- 风险评估与缓解

- 技术性能下降

- 需求波动

- 供应链中断

- 风险识别流程

- 缓解行动计划

- 供应链韧性与本地化

- 全球供应链图谱

- 供应链风险评估

- 在地化策略

- 政府激励措施

- 市场采纳与渗透分析

- 采用曲线分析

- 早期采用者的特征

- 主流市场渗透率

- 后期采用者群体

- 市场饱和度预测

- 各细分市场的渗透率

- 车辆类型渗透率

- 地理渗透率

- 应用特定采用

- 技术迁移模式

- 市场成熟度评估

- 技术成熟度指标

- 市场发展阶段

- 竞争强度演变

- 价值链优化

- 消费者行为与终端用户洞察

- 基础设施营运商的要求

- 使用者体验分析

- 客户之声洞察

- 购买决策因素

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依产品划分,2021-2034年

- 主要趋势

- 催化燃烧感测器

- 电化学感测器

- 金属氧化物半导体(MOS)感测器

- 热导率感测器

- 其他的

第六章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 微机电系统

- 固态感测器

第七章:市场估价与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 搭乘用车

- 轿车

- 掀背车

- SUV

- 商用车辆

- 轻型商用车

- 中型商用车

- 重型商用车辆

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 车载检测

- 燃料电池系统监测

- 氢气加註站

- 废气分析

- 碰撞后侦测

- 其他的

第九章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- OEM

- 售后市场

第十章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- 全球参与者

- Bosch

- Continental

- Figaro Engineering

- Honeywell

- Nissha FIS

- Sensata Technologies

- Sensirion

- 区域玩家

- Amphenol Sensors

- Infineon Technologies

- New Cosmos Electric

- TE Connectivity

- Vitesco Technologies

- 新兴玩家

- Custom Sensors Solutions

- NexTech Materials

- NGK Spark Plug

- Nuvoton Technology

- UST Umweltsensortechnik

- UTC Fuel Cells

- Winsen Sensor

- Xensor Integration

The Global Automotive Hydrogen Sensors Market was valued at USD 116.9 million in 2024 and is estimated to grow at a CAGR of 12% to reach USD 350.8 million by 2034.

The rising demand for hydrogen fuel cell vehicles, along with stringent safety regulations, is accelerating the growth of the automotive hydrogen sensors industry. These sensors are critical components designed to detect hydrogen leaks, monitor fuel cell performance, and ensure the overall safety of vehicles powered by hydrogen technology. The market features multiple sensing technologies such as electrochemical, catalytic combustion, thermal conductivity, and metal oxide semiconductor sensors, each catering to distinct automotive requirements. The ongoing development of hydrogen fueling networks is fueling the adoption of hydrogen sensors not only in vehicles but also across the broader hydrogen supply chain. Increasing investments in hydrogen-powered transport, particularly in commercial vehicles, are further driving market expansion. Although the COVID-19 pandemic initially disrupted production and delayed R&D projects due to supply chain constraints and reduced industrial activity, it ultimately acted as a catalyst for policy initiatives supporting hydrogen energy and safety advancements, leading to renewed momentum in market recovery and technological innovation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $116.9 Million |

| Forecast Value | $350.8 Million |

| CAGR | 12% |

The electrochemical sensors category captured a 35% share in 2024 and is expected to grow at a CAGR of 10.2% from 2025 to 2034. This segment continues to dominate due to its high precision, sensitivity, and fast response, which are essential in safety-critical automotive systems. Electrochemical sensors operate by using platinum-based electrodes within an electrolyte that produce electrical signals directly proportional to the hydrogen concentration in the environment. They are capable of detecting hydrogen concentrations as low as 1 ppm within seconds, making them ideal for monitoring applications that require accuracy and reliability.

The solid-state sensors segment held a 59% share and is projected to witness a robust CAGR of 14% during 2025-2034. Their dominance is attributed to their durability, compact design, and maintenance-free operation, which align with modern automotive preferences for reliable and long-lasting components. These sensors leverage MEMS and thin-film semiconductor technologies to create micro-scale sensing elements integrated with advanced signal processing and communication features. This approach enhances the robustness and efficiency of hydrogen detection in fuel cell and emission monitoring systems.

Asia-Pacific Automotive Hydrogen Sensors Market held a 51.6% share and is forecasted to grow at a 13% CAGR through 2034. Regional growth is primarily supported by large-scale public investment in hydrogen infrastructure, strong policy backing for zero-emission mobility, and rapid commercialization of hydrogen-powered vehicles. The region's strategic focus on hydrogen fuel adoption is expected to sustain its leadership position throughout the forecast period.

Key Automotive Hydrogen Sensors Market participants include Honeywell, Bosch, Amphenol Sensors, Continental, Infineon Technologies, Sensata Technologies, New Cosmos Electric, Figaro Engineering, Nissha FIS, and Sensirion. Companies active in the Automotive Hydrogen Sensors Market are implementing innovation-driven strategies to strengthen their global presence. They are heavily investing in research and development to create miniaturized, energy-efficient, and cost-effective sensor solutions tailored for hydrogen-powered vehicles. Strategic collaborations between automotive OEMs and sensor manufacturers are accelerating product development cycles and improving technology integration within fuel cell systems. Firms are also expanding their regional distribution networks and manufacturing capacities to meet the growing demand across emerging hydrogen economies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast

- 1.4 Primary research and validation

- 1.5 Some of the primary sources

- 1.6 Data mining sources

- 1.6.1 Secondary

- 1.6.1.1 Paid Sources

- 1.6.1.2 Public Sources

- 1.6.1.3 Sources, by region

- 1.6.1 Secondary

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Vehicle

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Specialized gas sensor manufacturers

- 3.1.1.2 Diversified industrial electronics conglomerates

- 3.1.1.3 Automotive-specific sensor suppliers

- 3.1.1.4 Chemical & advanced materials companies

- 3.1.1.5 Dedicated hydrogen & fuel cell technology specialists

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global push for green hydrogen and fuel cell electric vehicles

- 3.2.1.2 Expansion of hydrogen refueling infrastructure

- 3.2.1.3 Stringent safety standards and government mandates

- 3.2.1.4 Advancements in sensor technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of advanced sensor technologies

- 3.2.2.2 Technical and performance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with IoT and predictive maintenance

- 3.2.3.2 Growth of hydrogen-powered commercial vehicles

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Quantum dot sensors

- 3.3.1.2 Wireless sensor networks

- 3.3.1.3 Graphene-based detection

- 3.3.1.4 Predictive maintenance systems

- 3.3.2 Emerging technologies

- 3.3.2.1 Machine learning integration

- 3.3.2.2 Blockchain for data integrity

- 3.3.2.3 Augmented reality interfaces

- 3.3.2.4 AI-powered smart sensors

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Cost breakdown analysis

- 3.9 Patent landscape

- 3.9.1 Patent Portfolio Analysis

- 3.9.2 Key Patent Families

- 3.9.3 Patent Expiration Analysis

- 3.9.4 IP Strategy & Licensing

- 3.10 Price trends

- 3.10.1 Cost-plus pricing models

- 3.10.2 Margin enhancement strategies

- 3.10.3 Manufacturing expenses

- 3.10.4 Volume-price relationships

- 3.11 Product pipeline & R&D roadmap

- 3.11.1 Technology Development Timeline

- 3.11.1.1 Short-Term Developments (2024-2026)

- 3.11.1.2 Medium-Term Innovations (2027-2030)

- 3.11.1.3 Long-Term Breakthroughs (2031-2034)

- 3.11.1.4 Moonshot Technologies(Beyond 2034)

- 3.11.2 Product Development Stages

- 3.11.2.1 Concept & Feasibility Studies

- 3.11.2.2 Prototype Development

- 3.11.2.3 Pilot Testing & Validation

- 3.11.2.4 Commercial Launch Readiness

- 3.11.3 R&D Investment Analysis

- 3.11.3.1 Corporate R&D Spending

- 3.11.3.2 Government Funding Programs

- 3.11.3.3 Academic Research Initiatives

- 3.11.3.4 Public-Private Partnerships

- 3.11.4 Technology Readiness Assessment

- 3.11.4.1 TRL Mapping by Technology

- 3.11.4.2 Commercialization Timelines

- 3.11.4.3 Scalability Challenges

- 3.11.4.4 Market Entry Barriers

- 3.11.1 Technology Development Timeline

- 3.12 Risk assessment & mitigation

- 3.12.1 Technology performance degradation

- 3.12.2 Demand volatility

- 3.12.3 Supply chain disruptions

- 3.12.4 Risk identification processes

- 3.12.5 Mitigation action plans

- 3.13 Supply chain resilience & localization

- 3.13.1 Global supply chain mapping

- 3.13.2 Supply chain risk assessment

- 3.13.3 Localization strategies

- 3.13.4 Government incentives

- 3.14 Market adoption & penetration analysis

- 3.14.1.1 Adoption Curve Analysis

- 3.14.1.2 Early Adopter Characteristics

- 3.14.1.3 Mainstream Market Penetration

- 3.14.1.4 Late Adopter Segments

- 3.14.1.5 Market Saturation Projections

- 3.14.2 Penetration Rate by Segment

- 3.14.2.1 Vehicle Type Penetration

- 3.14.2.2 Geographic Penetration Rates

- 3.14.2.3 Application-Specific Adoption

- 3.14.2.4 Technology Migration Patterns

- 3.14.3 Market Maturity Assessment

- 3.14.3.1 Technology Maturity Indicators

- 3.14.3.2 Market Development Stages

- 3.14.3.3 Competitive Intensity Evolution

- 3.14.3.4 Value Chain Optimization

- 3.15 Consumer behavior & end-user insights

- 3.15.1 Infrastructure operator demands

- 3.15.2 User experience analysis

- 3.15.3 Voice of customer insights

- 3.15.4 Purchase decision factors

- 3.16 Sustainability and environmental aspects

- 3.16.1 Sustainable practices

- 3.16.2 Waste reduction strategies

- 3.16.3 Energy efficiency in production

- 3.16.4 Eco-friendly initiatives

- 3.16.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Catalytic combustion Sensors

- 5.3 Electrochemical sensors

- 5.4 Metal Oxide Semiconductor (MOS) sensors

- 5.5 Thermal conductivity sensors

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Microelectromechanical system

- 6.3 Solid-State sensors

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicle

- 7.2.1 Sedan

- 7.2.2 Hatchback

- 7.2.3 SUV

- 7.3 Commercial Vehicle

- 7.3.1 Light commercial vehicle

- 7.3.2 Medium commercial vehicle

- 7.3.3 Heavy commercial vehicles

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Onboard vehicle detection

- 8.3 Fuel cell system monitoring

- 8.4 Hydrogen refueling stations

- 8.5 Exhaust gas analysis

- 8.6 Post-crash detection

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Bosch

- 11.1.2 Continental

- 11.1.3 Figaro Engineering

- 11.1.4 Honeywell

- 11.1.5 Nissha FIS

- 11.1.6 Sensata Technologies

- 11.1.7 Sensirion

- 11.2 Regional players

- 11.2.1 Amphenol Sensors

- 11.2.2 Infineon Technologies

- 11.2.3 New Cosmos Electric

- 11.2.4 TE Connectivity

- 11.2.5 Vitesco Technologies

- 11.3 Emerging players

- 11.3.1 Custom Sensors Solutions

- 11.3.2 NexTech Materials

- 11.3.3 NGK Spark Plug

- 11.3.4 Nuvoton Technology

- 11.3.5 UST Umweltsensortechnik

- 11.3.6 UTC Fuel Cells

- 11.3.7 Winsen Sensor

- 11.3.8 Xensor Integration

汽车光束感测器市场:按组件、感测器类型、技术、车辆类型、应用和销售管道划分-2026-2032年全球预测

汽车光束感测器市场:按组件、感测器类型、技术、车辆类型、应用和销售管道划分-2026-2032年全球预测 2026-2034年全球汽车感测器市场规模、份额、趋势和成长分析报告

2026-2034年全球汽车感测器市场规模、份额、趋势和成长分析报告 2026年全球汽车感测器市场报告数位汽车超音波感测器市场按安装类型、换能器类型、运作频率、车辆类型和应用划分-全球预测,2026-2032年汽车电流感测器:2026-2032年全球市场预测(按感测器类型、应用、车辆类型、技术和最终用户划分)

2026年全球汽车感测器市场报告数位汽车超音波感测器市场按安装类型、换能器类型、运作频率、车辆类型和应用划分-全球预测,2026-2032年汽车电流感测器:2026-2032年全球市场预测(按感测器类型、应用、车辆类型、技术和最终用户划分) 全球下一代自动驾驶安全系统市场:未来预测(至2032年)-按系统类型、车辆类型、最终用户和地区分類的分析

全球下一代自动驾驶安全系统市场:未来预测(至2032年)-按系统类型、车辆类型、最终用户和地区分類的分析 日本汽车感测器市场报告(按类型、车辆类型、应用、销售管道(原厂配套、售后市场)和地区划分,2026-2034年)

日本汽车感测器市场报告(按类型、车辆类型、应用、销售管道(原厂配套、售后市场)和地区划分,2026-2034年) 汽车主动安全感测器市场规模、份额和成长分析(按车辆类型、应用、感测器类型和地区划分)—2026-2033年产业预测

汽车主动安全感测器市场规模、份额和成长分析(按车辆类型、应用、感测器类型和地区划分)—2026-2033年产业预测 轮胎感测器市场规模、份额及成长分析(按产品类型、销售管道、车辆类型及地区划分)-2026-2033年产业预测

轮胎感测器市场规模、份额及成长分析(按产品类型、销售管道、车辆类型及地区划分)-2026-2033年产业预测 汽车惯性测量单元(IMU)市场规模、份额和成长分析(按技术、应用和地区划分)-2026-2033年产业预测

汽车惯性测量单元(IMU)市场规模、份额和成长分析(按技术、应用和地区划分)-2026-2033年产业预测