|

市场调查报告书

商品编码

1876633

特种化学品回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Specialty Chemicals Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

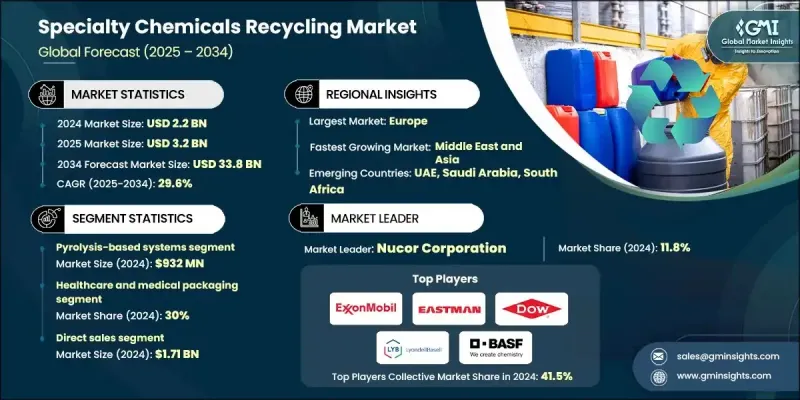

2024 年全球特用化学品回收市场价值为 22 亿美元,预计到 2034 年将以 29.6% 的复合年增长率增长至 338 亿美元。

随着各行业日益重视回收溶剂、催化剂、颜料和其他特殊化学品副产品等原本会成为废弃物的有价值材料,市场需求正在不断增长。将这些材料回收为可重复使用的原料或中间体化学品,不仅能显着降低原料消耗和製造成本,还能促进环境永续性和循环经济目标的实现。蒸馏、薄膜分离、解聚和纯化方法的创新正在改变回收格局,提高回收材料的效率和纯度。自动化、数位化监控和流程最佳化软体进一步提升了回收的一致性,降低了能源消耗,并增强了成本效益。这些因素使得特种化学品回收成为包括製药、水处理、黏合剂、涂料和电子等行业在内的众多行业中更具商业可行性和环境责任感的解决方案。已开发经济体正以严格的永续发展法规引领潮流,而新兴市场也稳定采用这些回收系统,以最大限度地减少浪费、降低生产成本并实现环境目标。向闭环生产系统的转变,正使特种化学品回收成为全球工业永续发展的关键推动因素。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 22亿美元 |

| 预测值 | 338亿美元 |

| 复合年增长率 | 29.6% |

2024年,基于热解技术的系统创造了9.32亿美元的产值。这些系统之所以引领市场,是因为它们能够处理传统回收方法无法处理的复杂且受污染的废物流。热解技术将混合化学材料转化为可重复利用的原料,从而支持那些致力于循环生产模式和提高材料回收效率的产业。解聚技术紧随其后,其优势在于能够回收高纯度单体,这些单体可用于製造性能与原生材料相同的再生材料。对永续原料日益增长的关注以及减少对化石燃料依赖的努力,是推动热解和解聚製程在多个工业领域广泛应用的关键因素。

预计到2024年,医疗保健和医疗包装领域将占据30%的市场。该领域的成长主要得益于市场对药品、医疗器材和一次性用品所需的无菌、耐用且易于操作的包装解决方案的需求不断增长。人口老化加剧、医疗保健支出不断攀升以及卫生法规日益严格,都进一步强化了医疗保健生态系统对先进可回收包装材料的需求。此外,由于电动车和自动驾驶汽车技术的快速发展,汽车产业也取得了显着进展,这些技术需要创新且永续的包装和化学解决方案来保护其复杂的电子和感测器系统。

2024年,美国特用化学品回收市场规模达5.694亿美元。在北美,由于建筑和汽车行业的强劲需求,特种化学品回收行业持续扩张。在美国,电动车的快速普及和节能建筑实践的推广,增加了对钢铁和铝等再生材料的需求。加拿大在工业废料和废弃物中金属和化学品的回收利用方面取得了显着进展,这得益于其对永续发展和循环经济实践的国家承诺。这些因素共同推动该地区转型为资源高效型製造和永续工业营运。

全球特种化学品回收市场的主要参与者包括科思创、雪佛龙菲利普斯化学公司、巴斯夫公司、伊士曼化学公司、陶氏公司、帝斯曼-菲美意公司、阿科玛公司、赢创工业集团、埃克森美孚公司、利安德巴塞尔公司、江苏东方盛宏公司、Indorama Ventures公司、马来西亚国家石油化学集团、三菱工业公司。这些市场领导者正致力于创新、合作和产能扩张,以巩固其市场地位。许多企业正在投资先进的回收技术,例如热解、解聚和溶剂回收,以提高製程效率和材料品质。它们正与工业製造商和研究机构建立策略联盟和合资企业,以加速高纯度再生化学品的商业化。此外,各公司也正在采用数位化和自动化技术来优化回收操作、降低成本并提高可追溯性。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 原料成本上涨

- 回收製程的技术进步

- 终端用户产业的需求不断成长

- 成长驱动因素

- 产业陷阱与挑战

- 高初始投资

- 市场对再生化学品的需求波动

- 市场机会

- 先进回收技术的发展

- 用于化学废弃物交易的数位平台

- 利用回收化学品进行产品创新

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依技术类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依技术类型划分,2021-2034年

- 主要趋势

- 基于热解的系统

- 解聚技术

- 溶解和纯化

- 气化和热处理

- 新兴和混合技术

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 医疗保健和医疗包装

- 汽车应用

- 电子和半导体

- 包装产业

- 建筑材料

- 其他工业应用

第七章:市场估计与预测:依配销通路划分,2021-2034年

- 主要趋势

- 直销

- 在线的

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Arkema

- BASF SE

- Chevron Phillips Chemical

- Covestro

- DSM-Firmenich

- Dow Inc.

- Eastman Chemical

- Evonik Industrie

- ExxonMobil

- Indorama Ventures

- Jiangsu Eastern Shenghong

- LyondellBasell

- Mitsubishi Chemical

- PETRONAS Chemical Group

- SABIC

The Global Specialty Chemicals Recycling Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 29.6% to reach USD 33.8 billion by 2034.

The market is gaining traction as industries increasingly focus on recovering valuable materials such as solvents, catalysts, pigments, and other specialty chemical by-products that would otherwise become waste. Recycling these materials into reusable feedstocks or intermediate chemicals significantly reduces raw material consumption and manufacturing costs while promoting environmental sustainability and circular economy goals. Technological advancements are transforming the recycling landscape through innovations in distillation, membrane separation, depolymerization, and purification methods, enabling greater efficiency and purity in recovered materials. Automation, digital monitoring, and process optimization software are further improving consistency, reducing energy usage, and enhancing cost-effectiveness. These factors make specialty chemical recycling a more commercially viable and environmentally responsible solution across industries, including pharmaceuticals, water treatment, adhesives, coatings, and electronics. Developed economies are taking the lead with stringent sustainability regulations, while emerging markets are steadily adopting these recycling systems to minimize waste, lower production costs, and meet environmental targets. The shift toward closed-loop production systems is positioning specialty chemical recycling as a key enabler of global industrial sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $33.8 Billion |

| CAGR | 29.6% |

The pyrolysis-based systems generated USD 932 million in 2024. These systems are leading the market due to their capability to process complex and contaminated waste streams that conventional recycling methods cannot manage. Pyrolysis technology converts mixed chemical materials into reusable feedstocks, supporting industries striving for circular production models and material recovery efficiency. Depolymerization technologies closely follow, offering the advantage of recovering high-purity monomers that can be used to manufacture recycled materials with identical performance to their virgin counterparts. The rising focus on sustainable raw materials and the drive to reduce dependency on fossil-based inputs are key factors encouraging the widespread adoption of both pyrolysis and depolymerization processes across multiple industrial sectors.

The healthcare and medical packaging segment held a 30% share in 2024. This segment's growth is fueled by increasing demand for sterile, durable, and easy-to-handle packaging solutions for pharmaceuticals, medical devices, and disposable products. The expanding aging population, along with rising healthcare expenditure and stricter hygiene regulations, has strengthened the need for advanced recyclable packaging materials in the healthcare ecosystem. The automotive sector is also witnessing significant progress due to technological evolution in electric and autonomous vehicles, which require innovative and sustainable packaging and chemical solutions for intricate electronic and sensor systems.

U.S. Specialty Chemicals Recycling Market accounted for USD 569.4 million in 2024. In North America, the specialty chemicals recycling industry continues to expand due to strong demand from the construction and automotive sectors. In the U.S., the rapid adoption of electric vehicles and energy-efficient building practices is increasing the need for recycled materials such as steel and aluminum. Canada is advancing in metal and chemical recovery from both industrial and obsolete waste, driven by its national commitment to sustainability and circular economy practices. Together, these factors are propelling the region's transition toward resource-efficient manufacturing and sustainable industrial operations.

Prominent players active in the Global Specialty Chemicals Recycling Market include Covestro, Chevron Phillips Chemical, BASF SE, Eastman Chemical, Dow Inc., DSM-Firmenich, Arkema, Evonik Industries, ExxonMobil, LyondellBasell, Jiangsu Eastern Shenghong, Indorama Ventures, PETRONAS Chemical Group, Mitsubishi Chemical, and SABIC. Leading companies in the Specialty Chemicals Recycling Market are focusing on innovation, collaboration, and capacity expansion to strengthen their market foothold. Many are investing in advanced recycling technologies such as pyrolysis, depolymerization, and solvent recovery to enhance process efficiency and material quality. Strategic alliances and joint ventures with industrial manufacturers and research organizations are being formed to accelerate the commercialization of high-purity recycled chemicals. Firms are also adopting digitalization and automation to optimize recycling operations, reduce costs, and improve traceability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology type

- 2.2.2 Application

- 2.2.3 Distribution channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising raw material costs

- 3.2.1.2 Technological advancements in recycling processes

- 3.2.1.3 Growing demand from End use industries

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1 High initial investment

- 3.3.2 Fluctuating market demand for recycled chemicals

- 3.4 Market opportunities

- 3.4.1 Development of advanced recycling technologies

- 3.4.2 Digital platforms for chemical waste trading

- 3.4.3 Product innovation using recycled chemicals

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By technology type

- 3.11 Future market trends

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Patent landscape

- 3.14 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.14.1 Major importing countries

- 3.14.2 Major exporting countries

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable practices

- 3.15.2 Waste reduction strategies

- 3.15.3 Energy efficiency in production

- 3.15.4 Eco-friendly initiatives

- 3.16 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pyrolysis-based systems

- 5.3 Depolymerization technologies

- 5.4 Dissolution and purification

- 5.5 Gasification and thermal processing

- 5.6 Emerging and hybrid technologies

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Healthcare and medical packaging

- 6.3 Automotive applications

- 6.4 Electronics and semiconductors

- 6.5 Packaging industries

- 6.6 Construction and building materials

- 6.7 Other industrial applications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Online

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arkema

- 9.2 BASF SE

- 9.3 Chevron Phillips Chemical

- 9.4 Covestro

- 9.5 DSM-Firmenich

- 9.6 Dow Inc.

- 9.7 Eastman Chemical

- 9.8 Evonik Industrie

- 9.9 ExxonMobil

- 9.10 Indorama Ventures

- 9.11 Jiangsu Eastern Shenghong

- 9.12 LyondellBasell

- 9.13 Mitsubishi Chemical

- 9.14 PETRONAS Chemical Group

- 9.15 SABIC

电池回收化学品市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

电池回收化学品市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 丙酸铵市场报告:趋势、预测及竞争分析(至2031年)

丙酸铵市场报告:趋势、预测及竞争分析(至2031年) 纸张表面上浆剂:全球市场份额和排名、总收入和需求预测(2025-2031 年)

纸张表面上浆剂:全球市场份额和排名、总收入和需求预测(2025-2031 年) 全球氟化钾市场按形态、纯度、应用、终端用户产业和地区划分-预测至2032年

全球氟化钾市场按形态、纯度、应用、终端用户产业和地区划分-预测至2032年 共聚维酮市场分析及预测(至2034年):类型、产品、应用、形式、技术、最终用户、功能、流程、成分

共聚维酮市场分析及预测(至2034年):类型、产品、应用、形式、技术、最终用户、功能、流程、成分 塔填料市场按类型、材料、应用、最终用途产业和分销管道划分-2025-2030 年全球预测

塔填料市场按类型、材料、应用、最终用途产业和分销管道划分-2025-2030 年全球预测 橡胶加工化学品需求、产能、产量、价格分布、产业展望(至2034年)

橡胶加工化学品需求、产能、产量、价格分布、产业展望(至2034年)