|

市场调查报告书

商品编码

1876802

汽车半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

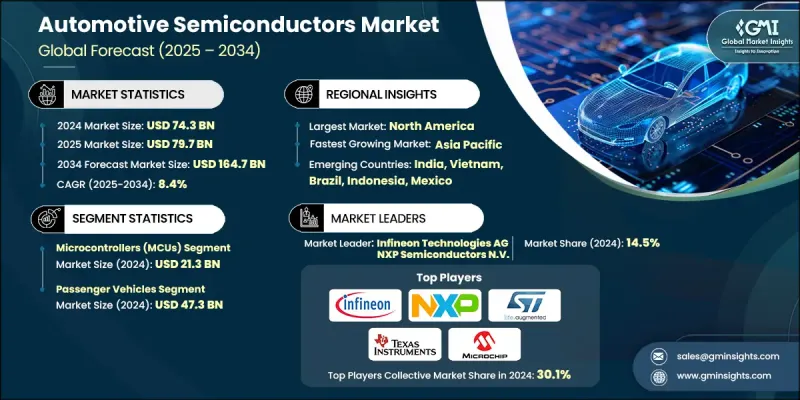

2024 年全球汽车半导体市场价值为 743 亿美元,预计到 2034 年将以 8.4% 的复合年增长率增长至 1,647 亿美元。

电动车的日益普及以及动力系统技术的不断演进,正在推动汽车半导体需求的成长。车辆电气化程度的提高,以及高阶驾驶辅助系统(ADAS)和自动驾驶系统的快速发展,正在改变汽车的安全性和营运效率。资讯娱乐系统、车辆互联解决方案和车联网(V2X)通讯技术的日益融合,进一步加速了半导体的应用。此外,日益严格的排放标准和监管规范也促使汽车製造商(OEM)部署基于半导体的控制系统,以提高燃油效率并降低排放。全球向电动化和智慧化的转型正在不断重塑半导体产业格局,因为这些晶片在能量转换、电池管理和车辆智慧化方面发挥着至关重要的作用,从而支持建立更智慧、更永续的汽车生态系统。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 743亿美元 |

| 预测值 | 1647亿美元 |

| 复合年增长率 | 8.4% |

2024年,微控制器市场规模预计将达213亿美元。汽车电子元件含量的不断增加,尤其是在电动车和配备高级驾驶辅助系统(ADAS)的车型中,持续推动对高性能汽车微控制器的需求。这些组件仍然是动力系统控制、电池管理、安全气囊、资讯娱乐系统和网域控制器等系统不可或缺的一部分。随着软体定义汽车(SDV)的兴起,微控制器的应用范围也在不断扩大,因为它们能够实现更快的即时运算和跨多个子系统的高级车辆协调。

预计到2034年,轻型商用车(LCV)市场将以7.9%的复合年增长率成长。城市配送车队的电气化和互联远端资讯处理技术的整合是推动这一成长的关键因素。 2级商用车产量的不断增长以及对车队可持续性日益重视,正在为轻型商用车电气化和数位化监控专用半导体创造稳定的需求。

2024年,美国汽车半导体市场规模预计将达174亿美元。电动车的加速普及,加上政府的优惠政策和严格的监管框架,正在推动全美半导体需求的成长。製造商正在调整研发策略,以满足OEM厂商对区域电子/电气架构的要求,并开发符合AEC-Q100 1级安全性和可靠性标准的先进人工智慧和机器学习处理器。

全球汽车半导体市场的主要企业包括:采埃孚股份公司 (ZF Friedrichshafen AG)、瑞萨电子株式会社 (Renesas Electronics Corporation)、意法半导体公司 (STMicroelectronics NV)、英飞凌科技股份公司 (Infineon Technologies AG)、亚德诺导体公司 (Peranoial NV)、罗姆株式会社 (Rohm Co., Ltd.)、超微半导体公司 (Advanced Micro Devices)、大陆集团 (Continental)、东芝 (Toshiba)、德州仪器公司 (Texas Instruments, Inc.)、塔芯半导体有限公司 (Tower Semiconductor Ltd.)、泰科科技公司 (Micron Technology. (Onsemi)、美力仕公司 (Melexis NV)、罗伯特博世有限公司 (Robert Bosch GmbH)、美光科技 (Micron Technology) 和艾利格罗微系统公司 (Allegro Microsystems)。汽车半导体产业的领导者正致力于创新、策略联盟和产能扩张,以巩固其市场地位。他们大力投资研发,以开发支援电动和自动驾驶汽车架构的晶片,同时提升能源效率和处理速度。与原始设备製造商 (OEM) 和一级供应商的合作有助于产品开发与新兴汽车平台保持一致。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 衝击力

- 成长驱动因素

- 电气化和动力系统变革正在推动对汽车半导体的需求。

- 越来越关注高级驾驶辅助系统(ADAS)和自动驾驶

- 资讯娱乐系统与车载网路的日益融合

- 对互联互通和车联网(V2X)通讯的需求日益增长

- 监管压力和更严格的排放标准正在加速半导体技术的应用。

- 产业陷阱与挑战

- 供应链中断

- 高昂的研发和合规成本

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 新兴商业模式

- 合规要求

- 永续性措施

- 专利和智慧财产权分析

- 地缘政治与贸易动态

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 对主要参与者进行竞争基准分析

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理位置比较

- 全球足迹分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导人

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年主要发展动态

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/新创企业竞争对手格局

第五章:市场估算与预测:依组件类型划分,2021-2034年

- 主要趋势

- 微控制器(MCU)

- 感应器

- 功率半导体

- 记忆

- 类比和混合讯号积体电路

- 其他的

第六章:市场估价与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 搭乘用车

- 轻型商用车(LCV)

- 重型商用车辆(HCV)

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 动力系统与电气化

- 引擎控制单元(ECU)

- 电池管理系统(BMS)

- 车用充电器

- 其他的

- 安全系统

- 高级驾驶辅助系统(ADAS)

- 防锁死煞车系统(ABS)

- 电子稳定控制系统(ESC)

- 其他的

- 人体电子系统

- 车门、座椅和车窗控制

- 照明(LED,自适应头灯)

- 暖通空调系统

- 其他的

- 底盘和悬吊

- 电动辅助转向系统(EPS)

- 悬吊控制单元

- 其他的

- 资讯娱乐和车载资讯系统

- 音频处理和放大器

- GPS及导航系统

- 其他的

第八章:市场估算与预测:依销售管道划分,2021-2034年

- 主要趋势

- 原始设备製造商

- 售后市场

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球关键参与者

- Infineon Technologies AG

- NXP Semiconductors NV

- STMicroelectronics NV

- Texas Instruments, Inc.

- Renesas Electronics Corporation

- Microchip Technology Inc.

- 区域关键参与者

- 北美:

- Advanced Micro Devices (AMD)

- Analog Devices, Inc.

- Micron Technology

- Onsemi

- 欧洲:

- Continental

- Melexis NV

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- 亚太地区:

- Toshiba

- Rohm Co., Ltd.

- Tower Semiconductor Ltd.

- 北美:

- 小众/颠覆者

- Allegro Microsystems

- TE Connectivity

The Global Automotive Semiconductor Market was valued at USD 74.3 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 164.7 billion by 2034.

The growing adoption of electric mobility, coupled with the continuous evolution of powertrain technologies, is driving the demand for automotive semiconductors. Increasing vehicle electrification, along with the rapid advancement of ADAS and autonomous driving systems, is transforming automotive safety and operational efficiency. Rising integration of infotainment systems, vehicle connectivity solutions, and V2X communication is further accelerating semiconductor adoption. Additionally, tightening emission norms and regulatory standards are pushing OEMs to deploy semiconductor-based control systems for enhanced fuel efficiency and lower emissions. The global shift toward electric and intelligent mobility continues to reshape the semiconductor landscape, as these chips play a crucial role in energy conversion, battery management, and vehicle intelligence, supporting smarter and more sustainable automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $74.3 Billion |

| Forecast Value | $164.7 Billion |

| CAGR | 8.4% |

The microcontroller segment was valued at USD 21.3 billion in 2024. Increasing electronic content in vehicles, especially within electric and ADAS-equipped models, continues to boost demand for high-performance automotive microcontrollers. These components remain integral to systems such as powertrain control, battery management, airbags, infotainment, and domain controllers. With the rise of software-defined vehicles (SDVs), the reliance on MCUs is expanding as they enable faster real-time computing and advanced vehicle coordination across multiple subsystems.

The light commercial vehicles (LCVs) segment is projected to register a CAGR of 7.9% throughout 2034. Electrification of urban delivery fleets and integration of connected telematics are key contributors to this growth. The increasing production of Class 2 commercial vehicles and the rising focus on fleet sustainability are creating steady demand for semiconductors designed for LCV electrification and digital monitoring.

U.S. Automotive Semiconductor Market generated USD 17.4 billion in 2024. The accelerating adoption of electric vehicles, coupled with favorable government incentives and stringent regulatory frameworks, is driving semiconductor demand across the nation. Manufacturers are realigning R&D strategies to match OEM requirements for zonal E/E architectures and developing advanced AI- and ML-based processors that meet AEC-Q100 Grade 1 standards for safety and reliability.

Prominent companies operating in the Global Automotive Semiconductor Market include ZF Friedrichshafen AG, Renesas Electronics Corporation, STMicroelectronics N.V., Infineon Technologies AG, Analog Devices, Inc., NXP Semiconductors N.V., Rohm Co., Ltd., Advanced Micro Devices, Continental, Toshiba, Texas Instruments, Inc., Tower Semiconductor Ltd., TE Connectivity, Microchip Technology Inc., Onsemi, Melexis N.V., Robert Bosch GmbH, Micron Technology, and Allegro Microsystems. Leading companies in the automotive semiconductor industry are focusing on innovation, strategic alliances, and capacity expansion to strengthen their market position. They are heavily investing in R&D to develop chips that support electric and autonomous vehicle architectures while enhancing energy efficiency and processing speed. Partnerships with OEMs and Tier-1 suppliers help in aligning product development with emerging vehicle platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Component type trends

- 2.2.2 Vehicle type trends

- 2.2.3 Application trends

- 2.2.4 Sales channel trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical Success Factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification and powertrain evolution is driving demand for automotive semiconductors

- 3.2.1.2 Increasing focus on advanced driver-assistance systems (ADAS) and autonomous driving

- 3.2.1.3 Rising integration of infotainment systems and in-vehicle networking

- 3.2.1.4 Growing need for connectivity and vehicle-to-everything (V2X) communication

- 3.2.1.5 Regulatory pressure and stricter emission standards are accelerating semiconductor adoption

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply Chain Disruptions

- 3.2.2.2 High R&D and Compliance Costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.11 Patent and IP analysis

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Component Type, 2021-2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Microcontrollers (MCUs)

- 5.3 Sensors

- 5.4 Power semiconductors

- 5.5 Memory

- 5.6 Analog & mixed-signal ICs

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Vehicle Type, 2021-2034 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Light commercial vehicles (LCVs)

- 6.4 Heavy commercial vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Powertrain & electrification

- 7.2.1 Engine control units (ECU)

- 7.2.2 Battery management systems (BMS)

- 7.2.3 Onboard chargers

- 7.2.4 Others

- 7.3 Safety systems

- 7.3.1 Advanced driver assistance systems (ADAS)

- 7.3.2 Anti-lock braking systems (ABS)

- 7.3.3 Electronic stability control (ESC)

- 7.3.4 Others

- 7.4 Body electronics

- 7.4.1 Door, seat & window control

- 7.4.2 Lighting (LED, Adaptive headlamps)

- 7.4.3 HVAC systems

- 7.4.4 Others

- 7.5 Chassis & suspension

- 7.5.1 Electric power steering (EPS)

- 7.5.2 Suspension control units

- 7.5.3 Others

- 7.6 Infotainment & telematics

- 7.6.1 Audio processing & amplifiers

- 7.6.2 GPS & navigation systems

- 7.6.3 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021-2034 (USD Billion & Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Infineon Technologies AG

- 10.1.2 NXP Semiconductors N.V.

- 10.1.3 STMicroelectronics N.V.

- 10.1.4 Texas Instruments, Inc.

- 10.1.5 Renesas Electronics Corporation

- 10.1.6 Microchip Technology Inc.

- 10.2 Regional Key Players

- 10.2.1 North America:

- 10.2.1.1 Advanced Micro Devices (AMD)

- 10.2.1.2 Analog Devices, Inc.

- 10.2.1.3 Micron Technology

- 10.2.1.4 Onsemi

- 10.2.2 Europe:

- 10.2.2.1 Continental

- 10.2.2.2 Melexis N.V.

- 10.2.2.3 Robert Bosch GmbH

- 10.2.2.4 ZF Friedrichshafen AG

- 10.2.3 Asia Pacific:

- 10.2.3.1 Toshiba

- 10.2.3.2 Rohm Co., Ltd.

- 10.2.3.3 Tower Semiconductor Ltd.

- 10.2.1 North America:

- 10.3 Niche / Disruptors

- 10.3.1 Allegro Microsystems

- 10.3.2 TE Connectivity

汽车半导体市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、装置、最终使用者、功能及安装类型划分

汽车半导体市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、装置、最终使用者、功能及安装类型划分 2026年全球汽车半导体市场报告

2026年全球汽车半导体市场报告 汽车用碳化硅元件市场:2026-2032年全球预测(依元件类型、应用、额定电压和封装类型划分)汽车用碳化硅功率元件市场:2026-2032年全球预测(依元件类型、车辆型态、电压等级、额定功率、销售管道和应用划分)汽车用碳化硅功率模组市场:按车辆类型、配置、额定功率、冷却方式和应用划分,全球预测(2026-2032年)

汽车用碳化硅元件市场:2026-2032年全球预测(依元件类型、应用、额定电压和封装类型划分)汽车用碳化硅功率元件市场:2026-2032年全球预测(依元件类型、车辆型态、电压等级、额定功率、销售管道和应用划分)汽车用碳化硅功率模组市场:按车辆类型、配置、额定功率、冷却方式和应用划分,全球预测(2026-2032年) 汽车半导体市场:驱动智慧(2025)

汽车半导体市场:驱动智慧(2025) 乘用车半导体市场-全球产业规模、份额、趋势、机会和预测,按组件类型、应用类型、地区和竞争格局划分,2020-2030年预测

乘用车半导体市场-全球产业规模、份额、趋势、机会和预测,按组件类型、应用类型、地区和竞争格局划分,2020-2030年预测 汽车功率半导体及模组(SiC、GaN)产业(2025)

汽车功率半导体及模组(SiC、GaN)产业(2025) 汽车全像显示半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

汽车全像显示半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球汽车半导体市场按组件、车辆类型、动力系统、材料、应用和地区划分-预测至2030年

全球汽车半导体市场按组件、车辆类型、动力系统、材料、应用和地区划分-预测至2030年