|

市场调查报告书

商品编码

1876803

冷板市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Cold Plates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

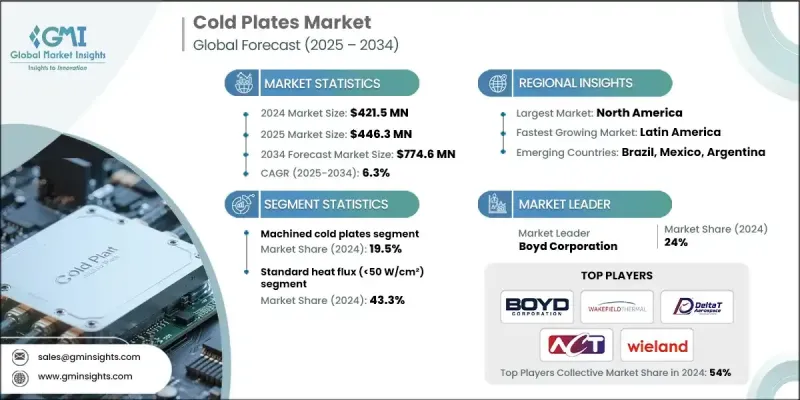

2024 年全球冷板市场价值为 4.215 亿美元,预计到 2034 年将以 6.3% 的复合年增长率增长至 7.746 亿美元。

电动车、再生能源系统和先进运算应用的日益普及推动了这一成长,而这些应用都需要高效的散热管理解决方案。冷板对于去除电力电子装置、电池和半导体元件产生的多余热量至关重要,从而确保系统的可靠性和性能。高效能运算、5G基础设施和储能领域的投资不断增加,也推动了对创新液冷技术的需求。製造商正致力于开发采用铝和铜等材料的紧凑、轻巧、高效的冷却系统,以满足汽车、航太和工业领域的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 4.215亿美元 |

| 预测值 | 7.746亿美元 |

| 复合年增长率 | 6.3% |

2024年,标准热通量容量(传热係数低于50 W/cm²)的散热器市占率为43.3%。此类别主要服务于工业电子、汽车系统以及各种通用热管理应用。凭藉其成熟的大规模生产能力,该类别能够提供经济高效的解决方案,满足各行各业的日常使用需求。

2024年,机械加工冷板市占率达到19.5%,预计将以6.4%的复合年增长率成长。这些解决方案透过精密数控加工和专业焊焊工艺,提供卓越的客製化能力。它们非常适合复杂的流路设计、精确的安装要求,以及整合翅片嵌件以提高传热效率,尤其适用于先进半导体、云端运算和人工智慧系统等严苛环境。

2024年,北美冷板市场占据33.4%的市场份额,预计到2034年将以5.6%的复合年增长率成长。该地区的领先地位得益于其先进的技术基础设施以及在航太、资料中心和医疗设备等关键领域对热管理解决方案的广泛应用。行业领先企业的存在、强大的研发实力以及对高效冷却系统以支持高性能电子设备的日益增长的需求,正在推动该地区的创新和市场持续扩张。

全球冷板市场的主要参与者,例如博伊德公司(Boyd Corporation)、德纳公司(Dana Incorporated)、TE Technology, Inc.、川崎泰克(Kawaso Texcel)、默森公司(Mersen)、印度潘特罗尼克斯公司(Pantronics India)、韦克菲尔德热解决方案公司(Wakefield Thermal Solutions)、威兰热解决方案Solutions)、泰西奥公司(Tesio)、QATS公司、建发科技公司(KenFa Tech.)、台达航太)和先进冷却技术公司(ACT),正致力于技术创新、策略合作和产能扩张,以巩固其市场地位。这些公司正在投资积层製造和精密加工等先进製造工艺,以提高设计灵活性和散热性能。与电动车製造商、航太公司和资料中心营运商的策略合作,使其能够提供满足高性能冷却需求的客製化解决方案。各公司也强调永续发展,开发轻质可回收材料和环保冷却剂,以减少对环境的影响。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依材料类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依材料类型划分,2021-2034年

- 主要趋势

- 铜

- 铝

- 不銹钢

- 杂交种

- 其他的

第六章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 冲压冷板

- 加工冷板

- 微通道冷板

- 成型管冷板

- 平板管冷板

- 深孔冷板

第七章:市场估算与预测:依热通量容量划分,2021-2034年

- 关键趋势

- 标准热通量(<50 W/cm²)

- 高热通量(50-200 W/cm²)

- 极高的热通量(200-500 W/cm²)

- 超高热通量(>500 W/cm²)

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 资料中心

- 电动车

- 航太与国防

- 工业电子

- 医疗设备

- 电信设备

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Advanced Cooling Technologies (ACT)

- Boyd Corporation

- Dana Incorporated

- DeltaT Aerospace

- Kawaso Texcel

- KenFa Tech.

- Mersen

- Pantronics India

- QATS

- TE Technology, Inc

- Tesio

- Wakefield Thermal Solutions

- Wieland Thermal Solutions

The Global Cold Plates Market was valued at USD 421.5 million in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 774.6 million by 2034.

The growth is driven by the rising adoption of electric vehicles (EVs), renewable energy systems, and advanced computing applications that require efficient thermal management solutions. Cold plates are essential for removing excess heat from power electronics, batteries, and semiconductor components, ensuring system reliability and performance. Increasing investments in high-performance computing, 5G infrastructure, and energy storage are boosting demand for innovative liquid-cooled technologies. Manufacturers are focusing on developing compact, lightweight, and high-efficiency cooling systems using materials such as aluminum and copper to meet the needs of automotive, aerospace, and industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $421.5 Million |

| Forecast Value | $774.6 Million |

| CAGR | 6.3% |

In 2024, the standard heat flux capacity segment, requiring a heat transfer rating below 50 W/cm2, held a 43.3% share. This category primarily serves industrial electronics, automotive systems, and a range of general thermal management applications. Owing to its well-established large-scale manufacturing, this segment delivers cost-effective solutions tailored for everyday use across diverse industries.

The machined cold plates segment captured a 19.5% share in 2024 and is projected to grow at a CAGR of 6.4%. These solutions offer superior customization capabilities through precision CNC machining and specialized brazing processes. They are ideal for intricate flow path designs, precise mounting requirements, and the integration of fin inserts that enhance heat transfer efficiency in demanding environments such as advanced semiconductors, cloud computing, and AI-based systems.

North America Cold Plates Market held 33.4% share in 2024 with a CAGR of 5.6% through 2034. The region's dominance is supported by its advanced technological infrastructure and widespread adoption of thermal management solutions across key sectors, including aerospace, data centers, and medical equipment. The presence of leading industry players, strong R&D activities, and the growing need for high-efficiency cooling systems to support high-performance electronics are driving innovation and continued market expansion in the region.

Leading players in the Global Cold Plates Market, such as Boyd Corporation, Dana Incorporated, TE Technology, Inc., Kawaso Texcel, Mersen, Pantronics India, Wakefield Thermal Solutions, Wieland Thermal Solutions, Tesio, QATS, KenFa Tech., DeltaT Aerospace, Advanced Cooling Technologies (ACT), are focusing on technological innovation, strategic partnerships, and capacity expansion to strengthen their market position. These companies are investing in advanced manufacturing processes like additive manufacturing and precision machining to enhance design flexibility and thermal performance. Strategic collaborations with EV manufacturers, aerospace firms, and data center operators are enabling customized solutions tailored to high-performance cooling requirements. Firms are emphasizing sustainability, developing lightweight recyclable materials, and eco-friendly coolants to reduce environmental impact.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Technology

- 2.2.4 Heat flux capacity

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Copper

- 5.3 Aluminum

- 5.4 Stainless steel

- 5.5 Hybrid

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Stamped cold plates

- 6.3 Machined cold plates

- 6.4 Microchannel cold plates

- 6.5 Formed tube cold plates

- 6.6 Flat tube cold plates

- 6.7 Deep drilled cold plates

Chapter 7 Market Estimates and Forecast, By Heat Flux Capacity, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trend

- 7.2 Standard heat flux (<50 W/cm²)

- 7.3 High heat flux (50-200 W/cm²)

- 7.4 Very high heat flux (200-500 W/cm²)

- 7.5 Ultra-high heat flux (>500 W/cm²)

Chapter 8 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Data centres

- 8.3 Electric vehicles

- 8.4 Aerospace & defense

- 8.5 Industrial electronics

- 8.6 Medical equipment

- 8.7 Telecommunication equipment

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Advanced Cooling Technologies (ACT)

- 10.2 Boyd Corporation

- 10.3 Dana Incorporated

- 10.4 DeltaT Aerospace

- 10.5 Kawaso Texcel

- 10.6 KenFa Tech.

- 10.7 Mersen

- 10.8 Pantronics India

- 10.9 QATS

- 10.10 TE Technology, Inc

- 10.11 Tesio

- 10.12 Wakefield Thermal Solutions

- 10.13 Wieland Thermal Solutions

冷轧钢板市场:2026-2032年全球市场预测(依产品类型、表面处理、通路和最终用途产业划分)伺服器水冷散热板市场:按冷却类型、伺服器类型、资料中心规模、散热能力、应用、最终用户产业划分,全球预测(2026-2032年)晶片用介质冷却板市场:依冷却机制、材料类型、流道设计与应用划分-全球预测,2026-2032年金属一体式冷板市场:按形状、冷却技术、冷却介质、材料、应用、终端用户产业划分,全球预测(2026-2032年)

冷轧钢板市场:2026-2032年全球市场预测(依产品类型、表面处理、通路和最终用途产业划分)伺服器水冷散热板市场:按冷却类型、伺服器类型、资料中心规模、散热能力、应用、最终用户产业划分,全球预测(2026-2032年)晶片用介质冷却板市场:依冷却机制、材料类型、流道设计与应用划分-全球预测,2026-2032年金属一体式冷板市场:按形状、冷却技术、冷却介质、材料、应用、终端用户产业划分,全球预测(2026-2032年) 全球冷板市场规模、份额、趋势和成长分析报告(2026-2034年)

全球冷板市场规模、份额、趋势和成长分析报告(2026-2034年) 冷轧板材市场-全球产业规模、份额、趋势、机会与预测:依硬度、终端用途产业、地区和竞争格局划分,2021-2031年商用车液冷板按动力传动系统、车辆类型、材质、类型、应用和最终用户划分 - 全球市场预测 2026-2032直接晶片液冷板市场按相态、冷却剂、冷板结构、目标元件、基板、设计类型和最终用户划分,全球预测,2026-2032年轧延半铸槽钢市场依产品类型、应用、终端用户产业及通路划分,全球预测(2026-2032年)冷轧钢板(冷轧捲板)市场规模、占有率、成长、全球产业分析:按类型、应用和地区划分的洞察,预测(2026-2034 年)

冷轧板材市场-全球产业规模、份额、趋势、机会与预测:依硬度、终端用途产业、地区和竞争格局划分,2021-2031年商用车液冷板按动力传动系统、车辆类型、材质、类型、应用和最终用户划分 - 全球市场预测 2026-2032直接晶片液冷板市场按相态、冷却剂、冷板结构、目标元件、基板、设计类型和最终用户划分,全球预测,2026-2032年轧延半铸槽钢市场依产品类型、应用、终端用户产业及通路划分,全球预测(2026-2032年)冷轧钢板(冷轧捲板)市场规模、占有率、成长、全球产业分析:按类型、应用和地区划分的洞察,预测(2026-2034 年)