|

市场调查报告书

商品编码

1876825

再生铅市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Recycled Lead Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

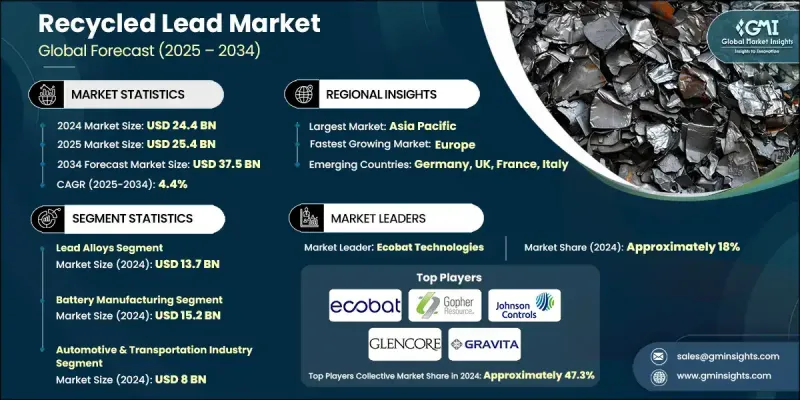

2024 年全球再生铅市场价值为 244 亿美元,预计到 2034 年将以 4.4% 的复合年增长率增长至 375 亿美元。

再生铅在循环经济中扮演着至关重要的角色,其主要来源是废弃铅酸电池和其他含铅产品。采用火法冶金和湿式冶金的回收工艺,可生产出品质和性能与原生铅相当的再生铅。日益严格的环境法规和永续发展倡议正推动製造商采用再生铅,从而减少碳排放并满足严格的合规标准。电动车的普及也增加了储能和电网稳定解决方案对再生铅的需求。铅酸电池仍然是汽车系统、工业备用电源和其他储能应用的关键部件。高达95%以上的回收率有助于建立闭环供应系统,在确保成本效益和供应可靠性的同时,减少对原生铅开采的依赖。全球监管部门的支持进一步加速了再生铅相对于原生铅的使用,因为再生铅对环境的影响较小。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 244亿美元 |

| 预测值 | 375亿美元 |

| 复合年增长率 | 4.4% |

2024年,铅合金市场规模达到137亿美元,占56%的市场份额,预计2025年至2034年将以4.3%的复合年增长率成长。铅合金之所以占据市场主导地位,是因为它们具有优异的机械强度、耐腐蚀性和透过与锑、锡和钙等金属合金化而优化的导电性。这些特性使其成为汽车电池、储能係统以及需要高耐用性和可靠性能的工业应用的理想选择。

2024年,电池製造业市场规模达152亿美元,占全球市场份额的62.4%,预计到2034年将以4.2%的复合年增长率成长。铅酸电池在汽车、工业和储能领域的广泛应用,是该产业主导的关键因素。再生铅与原生铅具有相同的电化学性能,同时也能降低成本并带来环境优势。铅酸电池的高回收率维持着稳健的闭环系统,确保了全球电池生产所需的再生铅的稳定供应。

预计2025年至2034年,北美再生铅市场将以4.5%的复合年增长率成长。企业对永续製造、循环经济倡议以及日益增强的环保意识推动了该地区的成长。对先进铅回收技术的投资不断增加,正逐步取代传统的原生铅生产方法,从而推动了汽车、工业和储能应用领域的市场需求。

全球再生铅市场的主要参与者包括Exide Technologies、Hindustan Zinc Limited、Gravita India Limited、Ecobat Technologies、RSR Corporation、Johnson Controls International、Gopher Resource、GreenLead、Prime Lead Recycling、LeadCo、Glencore(Britannia Refined Metals)、Ardee Industries Ltd.、Cim、Sami.m.、Smner)。这些公司正透过各种策略来巩固其市场地位,例如扩建回收设施以提高产能、采用先进的火法冶金和湿法冶金製程生产更高品质的再生铅,以及与电池製造商和工业客户建立战略合作伙伴关係。许多公司注重永续发展品牌建立和遵守环境法规,以获得竞争优势。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 陷阱与挑战

- 机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 软铅/纯铅

- 铅合金

- 铅锑合金

- 铅钙合金

- 铅硒和铅锡合金

- 客製化合金开发

- 氧化铅

- 红铅氧化物(Pb3O4)

- 二氧化铅(PbO)

- 四氧化铅(PbO2)

- 电池级氧化物

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 电池製造

- 汽车电池生产

- 工业电池製造

- 储能係统集成

- UPS和备用电源应用

- 辐射屏蔽

- 医疗设施申请

- 核工业要求

- 工业X射线及无损检测设备

- 捲材和挤出产品

- 建筑业需求

- 屋顶及防风雨工程

- 建筑应用

- 工业设备製造

- 颜料和化合物

- 工业油漆和涂料应用

- 化学加工用途

- 专业工业应用

- 其他应用

- 弹药与防御

- 电缆护套

- 专业工业用途

第七章:市场估算与预测:依最终用途产业划分,2021-2034年

- 主要趋势

- 汽车和运输业

- 能源与发电业

- 工业製造业

- 建筑与基础建设产业

- 医疗保健产业

- 电子通讯业

- 其他行业

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Ecobat Technologies

- Gopher Resource

- Glencore (Britannia Refined Metals)

- Gravita India Limited

- Cimbar Performance Minerals

- Sims Limited

- LeadCo

- Exide Technologies

- Hindustan Zinc Limited

- GreenLead

- EnerSys

- Prime Lead Recycling

- Ardee Industries Ltd.

- RSR Corporation

- Johnson Controls International

The Global Recycled Lead Market was valued at USD 24.4 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 37.5 billion by 2034.

Recycled lead plays a crucial role in the circular economy, primarily sourced from spent lead-acid batteries and other lead-containing products. The recycling process, using pyrometallurgical and hydrometallurgical methods, produces secondary lead that matches the quality and performance of primary lead. Rising environmental regulations and sustainability initiatives are driving manufacturers to adopt recycled lead, reducing carbon footprints and meeting strict compliance standards. The growing adoption of electric vehicles is also increasing demand for recycled lead in energy storage and grid stabilization solutions. Lead-acid batteries remain critical for automotive systems, industrial power backups, and other energy storage applications. High recycling rates, often exceeding 95%, support a closed-loop supply system, reducing reliance on primary lead extraction while ensuring cost efficiency and supply reliability. Regulatory support globally further accelerates the use of recycled lead over primary lead due to its lower environmental impact.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.4 Billion |

| Forecast Value | $37.5 Billion |

| CAGR | 4.4% |

The lead alloys generated USD 13.7 billion in 2024, holding a 56% share, and are expected to grow at a CAGR of 4.3% from 2025 to 2034. Lead alloys dominate the market due to their superior mechanical strength, corrosion resistance, and optimized electrical conductivity achieved by alloying with metals like antimony, tin, and calcium. These properties make them ideal for automotive batteries, energy storage systems, and industrial applications requiring high durability and reliable performance.

The battery manufacturing segment accounted for USD 15.2 billion in 2024, representing a 62.4% share, and is projected to grow at a CAGR of 4.2% through 2034. The widespread use of lead-acid batteries across automotive, industrial, and energy storage sectors underpins the dominance of this segment. Recycled lead offers identical electrochemical properties to primary lead, while delivering cost savings and environmental advantages. The high recycling rates of lead-acid batteries maintain a robust closed-loop system, ensuring a steady supply of recycled lead for battery production globally.

North America Recycled Lead Market is expected to grow at a CAGR of 4.5% from 2025 to 2034. Regional growth is supported by corporate adoption of sustainable manufacturing, circular economy initiatives, and rising environmental awareness. Increased investment in advanced lead recycling technologies is gradually replacing conventional primary lead production methods, driving demand across automotive, industrial, and energy storage applications.

Key players in the Recycled Lead Market include Exide Technologies, Hindustan Zinc Limited, Gravita India Limited, Ecobat Technologies, RSR Corporation, Johnson Controls International, Gopher Resource, GreenLead, Prime Lead Recycling, LeadCo, Glencore (Britannia Refined Metals), Ardee Industries Ltd., Cimbar Performance Minerals, EnerSys, and Sims Limited. Companies in the Global Recycled Lead Market are strengthening their market presence through strategies such as expanding recycling facilities to increase production capacity, adopting advanced pyrometallurgical and hydrometallurgical processes for higher-quality secondary lead, and forming strategic partnerships with battery manufacturers and industrial clients. Many firms focus on sustainability-driven branding and compliance with environmental regulations to gain a competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Soft/pure lead

- 5.3 Lead alloys

- 5.3.1 Lead-antimony alloys

- 5.3.2 Lead-calcium alloys

- 5.3.3 Lead-selenium & lead-tin alloys

- 5.3.4 Custom alloy development

- 5.4 Lead oxides

- 5.4.1 Red lead oxide (Pb3O4)

- 5.4.2 Lead(II) oxide (PbO)

- 5.4.3 Lead(IV) oxide (PbO2)

- 5.4.4 Battery-grade oxides

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Battery manufacturing

- 6.2.1 Automotive battery production

- 6.2.2 Industrial battery manufacturing

- 6.2.3 Energy storage system integration

- 6.2.4 Ups & backup power applications

- 6.3 Radiation shielding

- 6.3.1 Medical facility applications

- 6.3.2 Nuclear industry requirements

- 6.3.3 Industrial x-ray & ndt equipment

- 6.3.4 Rolls & extruded products

- 6.4 Construction industry demand

- 6.4.1 Roofing & weatherproofing

- 6.4.2 Architectural applications

- 6.4.3 Industrial equipment manufacturing

- 6.5 Pigments & chemical compounds

- 6.5.1 Industrial paint & coating applications

- 6.5.2 Chemical processing uses

- 6.5.3 Specialized industrial applications

- 6.6 Other applications

- 6.6.1 Ammunition & defense

- 6.6.2 Cable sheathing

- 6.6.3 Specialized industrial uses

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive & transportation industry

- 7.3 Energy & power generation industry

- 7.4 Industrial manufacturing industry

- 7.5 Construction & infrastructure industry

- 7.6 Healthcare & medical industry

- 7.7 Electronics & telecommunications industry

- 7.8 Other industries

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Ecobat Technologies

- 9.2 Gopher Resource

- 9.3 Glencore (Britannia Refined Metals)

- 9.4 Gravita India Limited

- 9.5 Cimbar Performance Minerals

- 9.6 Sims Limited

- 9.7 LeadCo

- 9.8 Exide Technologies

- 9.9 Hindustan Zinc Limited

- 9.10 GreenLead

- 9.11 EnerSys

- 9.12 Prime Lead Recycling

- 9.13 Ardee Industries Ltd.

- 9.14 RSR Corporation

- 9.15 Johnson Controls International

废金属回收市场分析及预测(至2035年):类型、产品类型、服务、技术、应用、形式、材质类型、製程、最终用户、设备

废金属回收市场分析及预测(至2035年):类型、产品类型、服务、技术、应用、形式、材质类型、製程、最终用户、设备 再生废金属市场规模、份额和成长分析(按来源、材质、应用、最终用户和地区划分)—产业预测(2026-2033 年)

再生废金属市场规模、份额和成长分析(按来源、材质、应用、最终用户和地区划分)—产业预测(2026-2033 年) 日本金属回收市场规模、份额、趋势和预测:按金属、产业和地区划分,2026-2034年

日本金属回收市场规模、份额、趋势和预测:按金属、产业和地区划分,2026-2034年 2026年全球再生金属市场报告2026年全球再生铅市场报告2026年全球金属回收市场报告2026年全球金属回收设备市场报告

2026年全球再生金属市场报告2026年全球再生铅市场报告2026年全球金属回收市场报告2026年全球金属回收设备市场报告 汽车金属回收市场-全球产业规模、份额、趋势、机会与预测:按金属、废弃物类型、设备、地区和竞争对手划分,2021-2031年

汽车金属回收市场-全球产业规模、份额、趋势、机会与预测:按金属、废弃物类型、设备、地区和竞争对手划分,2021-2031年 按原料、加工技术、服务类型、回收方法和最终用户产业分類的木炭回收服务市场-2026-2032年全球预测按金属类型、回收製程、产品形式、合金类型、最终用途产业和分销管道分類的全球回收和低碳金属市场预测(2026-2032年)

按原料、加工技术、服务类型、回收方法和最终用户产业分類的木炭回收服务市场-2026-2032年全球预测按金属类型、回收製程、产品形式、合金类型、最终用途产业和分销管道分類的全球回收和低碳金属市场预测(2026-2032年)