|

市场调查报告书

商品编码

1876827

猪疫苗市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Swine Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

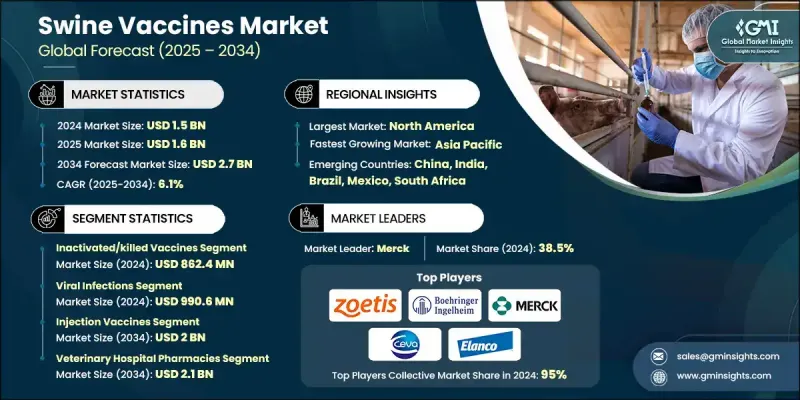

2024 年全球猪疫苗市场价值为 15 亿美元,预计到 2034 年将以 6.1% 的复合年增长率增长至 27 亿美元。

猪肉是全球消费量和产量不断增长的肉类之一,推动了市场成长。随着人口增长、城市化进程加快以及饮食习惯转变,人们对动物蛋白的需求日益增长,畜牧业的扩张也使得保障猪群的健康和生产力成为重中之重。为了提高效率和产量,集约化养猪业更加重视预防性保健,疫苗在最大限度降低可能影响动物存活和经济效益的疾病风险方面发挥关键作用。此外,在严重依赖猪肉的地区,粮食安全仍然是一个紧迫的问题,因此透过疫苗接种进行疾病预防对于维持稳定的供应链、防止价格飙升以及保障这一关键蛋白质来源的供应至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 15亿美元 |

| 预测值 | 27亿美元 |

| 复合年增长率 | 6.1% |

灭活疫苗或灭活疫苗市占率比57.6%,2024年市场规模达8.624亿美元。这类疫苗因其安全性高、稳定性好、保质期长而备受青睐,尤其适用于大规模疫苗接种项目,特别是冷链系统完善的地区。它们在预防常见猪病方面的可靠性确保了其在全球市场的持续需求。

2024年,病毒感染细分市场创造了9.906亿美元的市场规模,预计到2034年将以6.3%的复合年增长率成长。此细分市场的成长主要得益于影响猪群的传染性病毒疾病的高发生率及其造成的经济损失,包括那些会导致繁殖障碍、生长迟缓和重大经济损失的疾病。在猪群密度高的养殖场,病毒的高传染性使得疫苗接种成为最有效的预防策略,从而维持了该细分市场的主导地位。

2024年北美猪疫苗市场规模为6.508亿美元,预计到2034年将达到11亿美元,2025年至2034年间的复合年增长率(CAGR)为5.6%。该地区的领先地位得益于先进的畜牧管理实践、完善的兽医保健基础设施以及对优质猪肉的强劲需求。大型商业养猪场、传染病的频繁爆发以及领先的动物保健公司的存在,都推动了疫苗的普及,并巩固了北美市场的主导地位。

全球猪疫苗市场的主要参与者包括 Addison Biological Laboratory、Bioveta、勃林格殷格翰、Ceva Sante Animale、科罗拉多血清公司、礼来动物保健公司、HIPRA SA、Indian Immunologicals、默克、Biogenesis Bago、Vaxxinova(EWEW集团)、维克和硕腾集团)、维克和硕腾集团。这些公司透过投资研发,开发针对新出现的病毒性和细菌性猪病的创新高效疫苗,从而巩固其市场地位。他们透过策略合作、併购等方式拓展全球业务,同时提高供应链效率,确保关键地区的疫苗供应。此外,这些公司也致力于向养猪户普及预防保健知识,优化冷链物流,并提供猪群健康监测计画等加值服务。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 人畜共患病发生率上升

- 畜牧业扩张与粮食安全问题

- 疫苗技术的进步

- 动物疾病爆发日益增多

- 产业陷阱与挑战

- 研发成本高且开发週期长

- 冷链基础设施的限制

- 监理复杂性和审批延误

- 市场机会

- mRNA和下一代平台的应用

- 耐热疫苗的研发

- 联合疫苗创新

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

- 疫苗技术发展与创新

- 当前技术趋势

- 新兴技术

- 未来市场趋势

- 定价分析

- 专利分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依类型划分,2021-2034年

- 主要趋势

- 减毒活疫苗

- 灭活疫苗

- 病毒载体疫苗

- mRNA疫苗

- 其他疫苗

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 细菌感染

- 病毒感染

- 寄生虫感染

- 其他应用

第七章:市场估计与预测:依给药途径划分,2021-2034年

- 主要趋势

- 注射疫苗

- 口服疫苗

- 浸泡/喷洒疫苗

第八章:市场估算与预测:依配销通路划分,2021-2034年

- 主要趋势

- 兽医院药房

- 零售药局

- 电子商务

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 阿联酋

第十章:公司简介

- Addison Biological Laboratory

- Bioveta, as

- Boehringer Ingelheim

- Ceva Sante Animale

- Colorado Serum Company

- Elanco Animal Health Incorporated

- HIPRA SA

- Indian Immunologicals

- Merck

- biogenesis Bago

- Vaxxinova (EW Group)

- Virbac

- Zoetis

The Global Swine Vaccines Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 2.7 billion by 2034.

Market growth is driven by the rising global consumption and production of pork, one of the most widely consumed meats worldwide. Ensuring the health and productivity of swine herds has become a priority as the livestock industry expands to meet the growing demand for animal protein, fueled by rising populations, urbanization, and shifting dietary preferences. Intensification of swine production for higher efficiency and yield emphasizes preventive healthcare, with vaccines playing a critical role in minimizing disease risks that can impact animal survival and economic returns. Additionally, food security remains a pressing concern in regions heavily reliant on pork, making disease prevention through vaccination crucial to maintain stable supply chains, prevent price spikes, and safeguard the availability of this key protein source.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.7 Billion |

| CAGR | 6.1% |

The inactivated or killed vaccines segment held a 57.6% share and was valued at USD 862.4 million in 2024. These vaccines are preferred for their proven safety, stability, and long shelf life, making them ideal for large-scale vaccination programs, particularly in areas with established cold chain systems. Their reliability in preventing common swine diseases ensures ongoing demand across global markets.

The viral infections segment generated USD 990.6 million in 2024 and is expected to grow at a CAGR of 6.3% through 2034. This segment's growth is driven by the high prevalence and economic impact of contagious viral diseases that affect swine, including those that cause reproductive failures, growth retardation, and significant financial losses. High transmissibility in densely populated farms makes vaccination the most effective preventive strategy, sustaining this segment's market dominance.

North America Swine Vaccines Market generated USD 650.8 million in 2024 and is expected to reach USD 1.1 billion by 2034, growing at a CAGR of 5.6% between 2025 and 2034. The region's leadership is supported by advanced livestock management practices, robust veterinary healthcare infrastructure, and strong demand for high-quality pork. Major commercial swine operations, frequent outbreaks of contagious diseases, and the presence of leading animal health companies drive vaccine adoption and reinforce North America's dominant market position.

Key players operating in the Global Swine Vaccines Market include Addison Biological Laboratory, Bioveta, a.s., Boehringer Ingelheim, Ceva Sante Animale, Colorado Serum Company, Elanco Animal Health Incorporated, HIPRA S.A., Indian Immunologicals, Merck, biogenesis Bago, Vaxxinova (EW Group), Virbac, and Zoetis. Companies in the Swine Vaccines Market strengthen their presence by investing in research and development to create innovative, high-efficacy vaccines targeting emerging viral and bacterial swine diseases. They expand global reach through strategic partnerships, mergers, and acquisitions, while improving supply chain efficiency to ensure vaccine availability in key regions. Firms focus on educating swine producers about preventive healthcare benefits, optimizing cold chain logistics, and offering value-added services such as herd health monitoring programs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of zoonotic diseases

- 3.2.1.2 Expanding livestock industry and food security concerns

- 3.2.1.3 Advancements in vaccine technology

- 3.2.1.4 Increasing outbreaks of animal diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High R&D costs & long development timelines

- 3.2.2.2 Cold chain infrastructure limitations

- 3.2.2.3 Regulatory complexity & approval delays

- 3.2.3 Market opportunities

- 3.2.3.1 mRNA & next-generation platform adoption

- 3.2.3.2 Thermostable vaccine development

- 3.2.3.3 Combination vaccine innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Vaccine technology evolution and innovation

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Live attenuated vaccines

- 5.3 Inactivated/killed vaccines

- 5.4 Viral vector vaccines

- 5.5 mRNA vaccines

- 5.6 Other vaccines

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Bacterial infections

- 6.3 Viral infections

- 6.4 Parasitic infections

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Injection vaccines

- 7.3 Oral vaccines

- 7.4 Immersion/spray vaccines

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 UAE

Chapter 10 Company Profiles

- 10.1 Addison Biological Laboratory

- 10.2 Bioveta, a.s.

- 10.3 Boehringer Ingelheim

- 10.4 Ceva Sante Animale

- 10.5 Colorado Serum Company

- 10.6 Elanco Animal Health Incorporated

- 10.7 HIPRA S.A.

- 10.8 Indian Immunologicals

- 10.9 Merck

- 10.10 biogenesis Bago

- 10.11 Vaxxinova (EW Group)

- 10.12 Virbac

- 10.13 Zoetis