|

市场调查报告书

商品编码

1885905

血小板市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Blood Platelets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

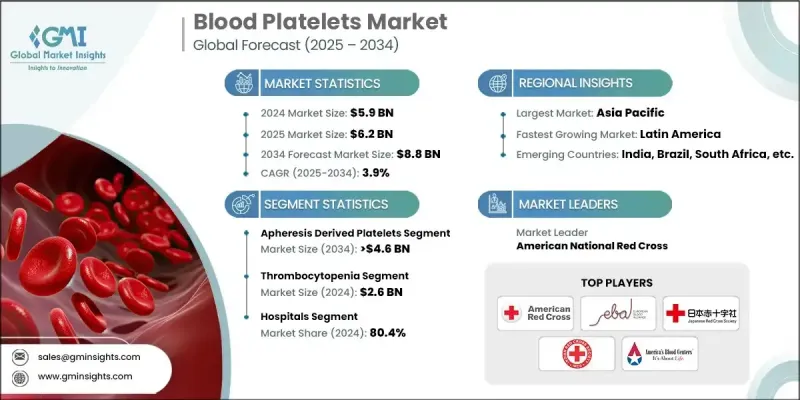

2024 年全球血小板市场价值为 59 亿美元,预计到 2034 年将以 3.9% 的复合年增长率增长至 88 亿美元。

市场扩张的驱动因素包括输血需求的成长、人们对捐血和血小板输注意的提高,以及慢性病和血液疾病盛行率的上升。此外,外科手术和急诊住院人数的增加也进一步刺激了需求。血小板处理和储存技术的创新、人工血小板和冷冻干燥血小板的研发,以及生技公司之间的策略合作,都是关键的成长因素。血小板在凝血和预防过度出血方面发挥着至关重要的作用,因此对于创伤护理、手术以及接受化疗或其他强化治疗的患者来说必不可少。各国政府、医院网路和全球血液组织都在支持血小板输注在全球的应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 59亿美元 |

| 预测值 | 88亿美元 |

| 复合年增长率 | 3.9% |

2024年,单采血小板市占率为53.1%。单采血小板直接从捐血者体内采集,采用自动化单采系统,在分离血小板的同时保留其他血液成分。这种方法每次捐血可获得更高的血小板量,并最大限度地降低同种免疫和输血相关感染的风险。单采血小板对于需要多次输血的患者尤其重要,例如接受癌症治疗或骨髓移植的患者。

2024年,血液肿瘤领域的市场估值为15亿美元。此领域涵盖血液癌症的治疗,包括白血病、淋巴瘤和骨髓瘤,其中血小板输注对于控制化疗引起的血小板减少症至关重要。接受强化癌症治疗的患者通常需要反覆输注血小板以降低出血併发症的风险。

2024年,北美血小板市场占据了26.8%的显着份额。该地区先进的医疗基础设施、民众对捐血的广泛认知以及癌症治疗、创伤治疗和复杂外科手术中对输血的强劲需求,共同推动了市场的发展。自动化血小板分离系统和病原体灭活技术的应用,确保了安全性和营运效率。政府扶持的广泛血小板捐赠网络,提高了血小板的供应量。

全球血小板市场的主要参与者包括美国血液中心、美国血库协会 (AABB)、美国红十字会、美国血液中心、巴西红十字会、加拿大血液服务中心、法国红十字会、德国红十字会、印度红十字会、义大利红十字会、日本红十字会、OneBlood、中国红十字会、南非红十字会、西班牙红十字会、欧洲血液联盟 (EBA) 和义大利国家血统中心。这些血小板企业正透过多种策略巩固其市场地位。他们专注于技术创新,包括自动化血球分离系统和病原体灭活方法,以提高安全性、效率和产品品质。与医院、医疗保健机构和当地捐血网络建立策略合作伙伴关係,可以扩大地域覆盖范围并提高捐血者的可及性。企业也投资研发人工血小板和冷冻干燥血小板,以延长保质期并减少对捐血者的依赖。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 慢性病和血液相关疾病的盛行率不断上升

- 输血需求不断成长

- 提高大众对捐血和血小板输注的认识

- 手术数量不断增加

- 产业陷阱与挑战

- 感染传播风险高

- 治疗费用高昂

- 机会

- 血小板富集血浆(PRP)在再生医学的应用拓展

- 自动化血小板生产技术进步

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 报销方案

- 2021-2034年各地区价格分析

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 北美洲

- 供应链和物流面临的挑战

- 宣传活动对捐款率的影响

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依血小板类型划分,2021-2034年

- 主要趋势

- 全血来源的血小板

- 血浆置换法所获得的血小板

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 血友病

- 血小板减少症

- 围手术期适应症

- 血小板功能障碍

- 血液肿瘤学

- 其他应用

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用途

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- American Association of Blood Banks (AABB)

- American National Red Cross

- America's Blood Centers

- Blood Centers of America

- Brazilian Red Cross

- Canada Blood Services

- French Red Cross

- German Red Cross

- Indian Red Cross Society

- Italian Red Cross

- Japanese Red Cross Society

- OneBlood

- Red Cross Society of China

- South African Red Cross

- Spanish Red Cross

- 欧洲血液联盟(EBA)

- The Italian National Blood Centre

The Global Blood Platelets Market was valued at USD 5.9 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 8.8 billion by 2034.

The expansion of the market is driven by the increasing demand for blood transfusions, rising awareness of blood donation and platelet transfusion, and the growing prevalence of chronic and hematological disorders. Additionally, the rising number of surgical procedures and emergency hospitalizations further fuels the demand. Innovations in platelet processing and storage, development of artificial and lyophilized platelets, and strategic collaborations between biotech companies are key growth factors. Platelets play a critical role in clotting and preventing excessive bleeding, making them essential for trauma care, surgery, and patients undergoing chemotherapy or other intensive treatments. Government initiatives, hospital networks, and global blood organizations are supporting the adoption of platelet transfusions worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.9 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 3.9% |

The apheresis-derived platelets segment held a 53.1% share in 2024. Platelets are collected directly from individual donors using automated apheresis systems that separate platelets while returning other blood components. This method produces higher platelet volumes per donation and minimizes risks associated with alloimmunization and transfusion-related infections. Apheresis platelets are especially critical for patients requiring multiple transfusions, such as those undergoing cancer therapy or bone marrow transplants.

The hemato-oncology segment was valued at USD 1.5 billion in 2024. This segment covers blood cancer treatments, including leukemia, lymphoma, and myeloma, where platelet transfusions are vital to manage chemotherapy-induced thrombocytopenia. Patients undergoing intensive cancer treatments frequently require repeated platelet transfusions to reduce the risk of bleeding complications.

North America Blood Platelets Market held a significant 26.8% share in 2024. The region's advanced healthcare infrastructure, robust awareness of blood donation, and strong demand for transfusions in cancer care, trauma treatment, and complex surgical procedures drive the market. Adoption of automated apheresis systems and pathogen reduction technologies ensures safety and operational efficiency. Extensive platelet donation networks supported by government initiatives enhance the availability of blood platelets.

Prominent companies operating in the Global Blood Platelets Market include America's Blood Centers, American Association of Blood Banks (AABB), American National Red Cross, Blood Centers of America, Brazilian Red Cross, Canada Blood Services, French Red Cross, German Red Cross, Indian Red Cross Society, Italian Red Cross, Japanese Red Cross Society, OneBlood, Red Cross Society of China, South African Red Cross, Spanish Red Cross, the European Blood Alliance (EBA), and the Italian National Blood Centre. Companies in the Blood Platelets Market are strengthening their position through multiple strategies. They focus on technological innovation, including automated apheresis systems and pathogen reduction methods, to improve safety, efficiency, and product quality. Strategic partnerships with hospitals, healthcare providers, and local blood donation networks expand geographic reach and improve donor accessibility. Firms invest in R&D to develop artificial and lyophilized platelets that enhance shelf life and reduce dependency on donors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Platelet type trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic and blood-related disorders

- 3.2.1.2 Growing demand for blood transfusions

- 3.2.1.3 Rise in awareness regarding blood donations and platelets transfusions

- 3.2.1.4 Rising number of surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of transmissions of infections

- 3.2.2.2 High cost of the treatment

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of platelet-rich plasma (PRP) applications in regenerative medicine

- 3.2.3.2 Technological advancements in automated platelet production

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis, by region, 2021-2034

- 3.7.1 North America

- 3.7.1.1 U.S.

- 3.7.1.2 Canada

- 3.7.2 Europe

- 3.7.2.1 Germany

- 3.7.2.2 UK

- 3.7.2.3 France

- 3.7.2.4 Spain

- 3.7.2.5 Italy

- 3.7.3 Asia Pacific

- 3.7.3.1 China

- 3.7.3.2 Japan

- 3.7.3.3 India

- 3.7.3.4 Australia

- 3.7.3.5 South Korea

- 3.7.4 Latin America

- 3.7.4.1 Brazil

- 3.7.4.2 Mexico

- 3.7.4.3 Argentina

- 3.7.5 MEA

- 3.7.5.1 South Africa

- 3.7.5.2 Saudi Arabia

- 3.7.5.3 UAE

- 3.7.1 North America

- 3.8 Challenges in supply chain and logistics

- 3.9 Impact of awareness campaigns on donation rates

- 3.10 Future market trends

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Platelet Type, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Whole-blood derived platelet

- 5.3 Apheresis derived platelets

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hemophilia

- 6.3 Thrombocytopenia

- 6.4 Perioperative indications

- 6.5 Platelet function disorders

- 6.6 Hemato-oncology

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 American Association of Blood Banks (AABB)

- 9.2 American National Red Cross

- 9.3 America's Blood Centers

- 9.4 Blood Centers of America

- 9.5 Brazilian Red Cross

- 9.6 Canada Blood Services

- 9.7 French Red Cross

- 9.8 German Red Cross

- 9.9 Indian Red Cross Society

- 9.10 Italian Red Cross

- 9.11 Japanese Red Cross Society

- 9.12 OneBlood

- 9.13 Red Cross Society of China

- 9.14 South African Red Cross

- 9.15 Spanish Red Cross

- 9.16 The European Blood Alliance (EBA)

- 9.17 The Italian National Blood Centre

人类血小板裂解液市场规模、份额及成长分析(按类型、应用、最终用户和地区划分)-2026-2033年产业预测

人类血小板裂解液市场规模、份额及成长分析(按类型、应用、最终用户和地区划分)-2026-2033年产业预测 抗血小板药物市场按药物类型、剂型、适应症、作用机制、给药方法、分销管道和最终用户划分-2025-2032 年全球预测

抗血小板药物市场按药物类型、剂型、适应症、作用机制、给药方法、分销管道和最终用户划分-2025-2032 年全球预测 全球血小板市场

全球血小板市场 人血小板溶解液的全球市场:市场规模·占有率·趋势,产业分析 (各用途·类别·各最终用途·各地区),未来预测 (2025年~2034年)

人血小板溶解液的全球市场:市场规模·占有率·趋势,产业分析 (各用途·类别·各最终用途·各地区),未来预测 (2025年~2034年) 血小板浓缩系统市场(按技术、应用、最终用户和地区)

血小板浓缩系统市场(按技术、应用、最终用户和地区) 血小板浓缩系统市场,按技术、应用、最终用途、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

血小板浓缩系统市场,按技术、应用、最终用途、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测