|

市场调查报告书

商品编码

1885913

新生儿护理市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Neonatal Infant Care Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

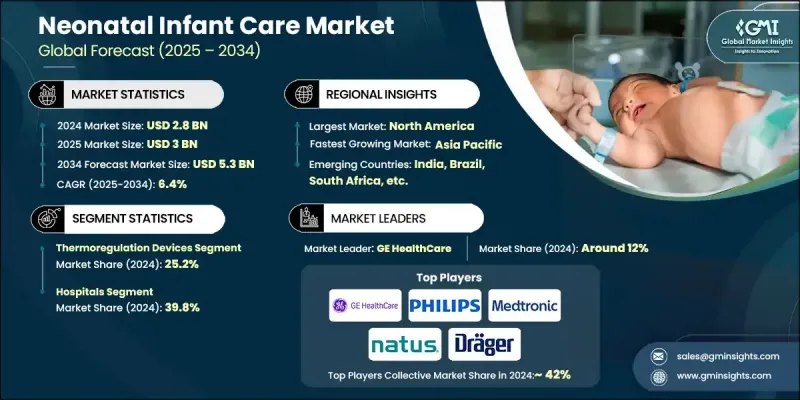

2024 年全球新生儿护理市场价值为 28 亿美元,预计到 2034 年将以 6.4% 的复合年增长率增长至 53 亿美元。

新生儿加护病房(NICU)的日益普及、政府对妇幼保健投入的增加以及早产儿数量的上升,共同推动了市场扩张。新生儿护理技术的进步,以及人们对婴儿死亡率和医疗品质标准的日益关注,都促进了新生儿护理设备的普及。便携式和非侵入性新生儿护理解决方案的开发,以及新兴经济体医疗支出的增加,也是重要的成长动力。公共卫生措施和国际资助支持新生儿设备的普及,而医院补贴和报销政策则使医疗机构能够投资先进技术。总而言之,这些因素共同为全球新生儿护理设备的普及创造了良好的环境。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 28亿美元 |

| 预测值 | 53亿美元 |

| 复合年增长率 | 6.4% |

2024年,体温调节设备市占率达25.2%。诸如保温箱和辐射保暖器等设备能够维持早产儿和低出生体重儿的最佳体温,预防低体温及其相关併发症。政府对妇幼保健计画的支持进一步推动了对这些技术的需求。

预计到2024年,医院市占率将达到39.8%。作为新生儿护理设备的主要用户,医院受益于专业的NICU(新生儿加护病房)和先进的基础设施。不断增长的患者群体和持续的政府资助推动了包括呼吸器、监护系统和保温箱在内的设备的不断升级。由于医院具备整合全面新生儿解决方案的能力,因此仍是市场成长的核心力量。

预计到2024年,北美新生儿护理市场将占据34.1%的市场。美国和加拿大强大的医疗基础设施、日益增强的婴儿健康意识以及先进的新生儿重症监护室(NICU)的普及,都为市场扩张提供了支持。人工智慧和物联网设备的快速普及,以及有利的报销政策,进一步推动了相关技术的采用。

新生儿护理市场的主要参与者包括GE医疗、德尔格、费雪派克医疗、美敦力、ATOM医疗、Masimo、飞利浦、Phoenix、Inspiration Healthcare Group、Cobams、Natus Medical、David、Novos Medical Systems、Fanem Medical Devices、Pluss和AVI Healthcare。这些公司透过投资创新设备技术,例如人工智慧驱动的监护系统和便携式护理解决方案,不断巩固其市场地位。他们专注于与医院和医疗保健机构进行策略合作,以拓展分销网络并提高市场渗透率。持续的研发投入提升了产品的可靠性、能源效率和易用性,并确保符合法规标准。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 早产发生率上升

- 新生儿加护病房的安装数量不断增加

- 政府加大对妇幼保健计画的投入

- 新生儿护理设备的技术进步

- 产业陷阱与挑战

- 先进的新生儿护理设备价格昂贵

- 低收入地区新生儿重症监护设施的可近性有限

- 机会

- 扩大居家新生儿护理解决方案

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 政策环境

- 流行病学情景

- 新生儿加护病房的病人安全与感染控制措施

- 2024年各区新生儿加护病房数量

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 波特的分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 体温调节装置

- 新生儿保温箱

- 保暖器

- 新生儿降温系统

- 光疗设备

- LED光疗系统

- CFL光疗系统

- 监控系统

- 新生儿通气

- 血气监测系统

- 脑监测

- 其他监控系统

- 新生儿復苏装置

- 新生儿听力筛检

- 视力筛检

- 其他产品类型

第六章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 医院

- 儿科和新生儿诊所

- 养老院

第七章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 奈及利亚

- 埃及

第八章:公司简介

- ATOM MEDICAL

- AVI Healthcare

- COBAMS

- DAVID

- Drager

- Fanem Medical Devices

- Fisher & Paykel HEALTHCARE

- GE Healthcare

- INSPIRATION HEALTHCARE GROUP

- MASIMO

- Medtronic

- Natus Medical

- Novos Medical Systems

- PHILIPS

- PHOENIX

- PLUSS

The Global Neonatal Infant Care Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 5.3 billion by 2034.

The market expansion is driven by the increasing establishment of NICU units, rising government investments in maternal and child healthcare, and the growing incidence of premature births. Advances in neonatal care technology, coupled with heightened awareness of infant mortality and healthcare quality standards, are fueling adoption. The development of portable and non-invasive neonatal care solutions and increased healthcare spending in emerging economies are also key growth contributors. Public health initiatives and international grants support access to neonatal devices, while hospital subsidies and reimbursement policies enable institutions to invest in advanced technology. Collectively, these factors are creating a robust environment for the adoption of neonatal infant care devices globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 6.4% |

In 2024, the thermoregulation devices segment accounted for a 25.2% share. Devices such as incubators and radiant warmers maintain optimal body temperature for premature and low-birth-weight infants, preventing hypothermia and related complications. Government support for maternal and child health programs further drives demand for these technologies.

The hospitals segment held a 39.8% share in 2024. As primary users of neonatal care devices, hospitals benefit from specialized NICUs and advanced infrastructure. The rising patient population and consistent government funding encourage continuous upgrades, including ventilators, monitoring systems, and incubators. Hospitals remain central to market growth due to their capacity to integrate comprehensive neonatal solutions.

North America Neonatal Infant Care Market held 34.1% share in 2024. Strong healthcare infrastructure, increased awareness of infant health, and the presence of advanced NICUs in the U.S. and Canada support market expansion. The rapid integration of AI- and IoT-enabled devices, along with favorable reimbursement policies, further propels adoption.

Key players in the Neonatal Infant Care Market include GE Healthcare, Drager, Fisher & Paykel Healthcare, Medtronic, ATOM Medical, Masimo, Philips, Phoenix, Inspiration Healthcare Group, Cobams, Natus Medical, David, Novos Medical Systems, Fanem Medical Devices, Pluss, and AVI Healthcare. Companies operating in the Neonatal Infant Care Market are strengthening their position by investing in innovative device technologies, such as AI-driven monitoring systems and portable care solutions. They focus on strategic collaborations with hospitals and healthcare providers to expand distribution networks and increase market penetration. Continuous R&D initiatives enhance product reliability, energy efficiency, and usability, ensuring compliance with regulatory standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of premature birth rate

- 3.2.1.2 Increasing number of installations for NICU units

- 3.2.1.3 Growing government investments in maternal and child health programs

- 3.2.1.4 Technological advancements in neonatal infant care devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced neonatal care equipment

- 3.2.2.2 Limited accessibility to NICU facilities in low-income regions

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of home-based neonatal care solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Policy landscape

- 3.7 Epidemiology scenario

- 3.8 Patient safety and infection control measures in NICUs

- 3.9 Number of neonatal intensive care units, by region, 2024

- 3.9.1 Global

- 3.9.2 North America

- 3.9.3 Europe

- 3.9.4 Asia Pacific

- 3.9.5 Latin America

- 3.9.6 MEA

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Thermoregulation devices

- 5.2.1 Neonatal incubators

- 5.2.2 Warmers

- 5.2.3 Neonatal cooling systems

- 5.3 Phototherapy devices

- 5.3.1 LED phototherapy system

- 5.3.2 CFL phototherapy system

- 5.4 Monitoring systems

- 5.4.1 Neonatal ventilation

- 5.4.2 Blood gas monitoring system

- 5.4.3 Brain monitoring

- 5.4.4 Other monitoring systems

- 5.5 Neonatal infant resuscitator devices

- 5.6 Neonatal hearing screening

- 5.7 Vision screening

- 5.8 Other product types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Pediatric & neonatal clinics

- 6.4 Nursing homes

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

- 7.6.4 Nigeria

- 7.6.5 Egypt

Chapter 8 Company Profiles

- 8.1 ATOM MEDICAL

- 8.2 AVI Healthcare

- 8.3 COBAMS

- 8.4 DAVID

- 8.5 Drager

- 8.6 Fanem Medical Devices

- 8.7 Fisher & Paykel HEALTHCARE

- 8.8 GE Healthcare

- 8.9 INSPIRATION HEALTHCARE GROUP

- 8.10 MASIMO

- 8.11 Medtronic

- 8.12 Natus Medical

- 8.13 Novos Medical Systems

- 8.14 PHILIPS

- 8.15 PHOENIX

- 8.16 PLUSS

胎儿和新生儿护理设备市场报告:按产品类型、最终用户和地区划分(2026-2034 年)

胎儿和新生儿护理设备市场报告:按产品类型、最终用户和地区划分(2026-2034 年) 全球新生儿和婴儿护理市场规模、份额、趋势和成长分析报告(2026-2034年)全球胎儿和新生儿护理设备市场规模、份额、趋势和成长分析报告(2026-2034年)

全球新生儿和婴儿护理市场规模、份额、趋势和成长分析报告(2026-2034年)全球胎儿和新生儿护理设备市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球胎儿和新生儿护理设备市场报告2026年新生儿加护病房(NICU)导管市场报告

2026年全球胎儿和新生儿护理设备市场报告2026年新生儿加护病房(NICU)导管市场报告 新生儿无创血压袖带市场:按袖带类型、袖带设计、尺寸类别、分销管道和最终用户划分,全球预测,2026-2032年

新生儿无创血压袖带市场:按袖带类型、袖带设计、尺寸类别、分销管道和最终用户划分,全球预测,2026-2032年 新生儿护理市场规模、份额和成长分析(按产品类型、最终用户和地区划分)—产业预测(2026-2033 年)

新生儿护理市场规模、份额和成长分析(按产品类型、最终用户和地区划分)—产业预测(2026-2033 年) 全球新生儿护理设备市场(按产品、最终用户和地区)- 预测至 2030 年

全球新生儿护理设备市场(按产品、最终用户和地区)- 预测至 2030 年 胎儿和新生儿护理设备市场报告:2031 年趋势、预测和竞争分析

胎儿和新生儿护理设备市场报告:2031 年趋势、预测和竞争分析 胎儿和新生儿护理设备市场:全球市场洞察、竞争格局和 2032 年预测

胎儿和新生儿护理设备市场:全球市场洞察、竞争格局和 2032 年预测