|

市场调查报告书

商品编码

1885917

耐用医疗设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Durable Medical Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

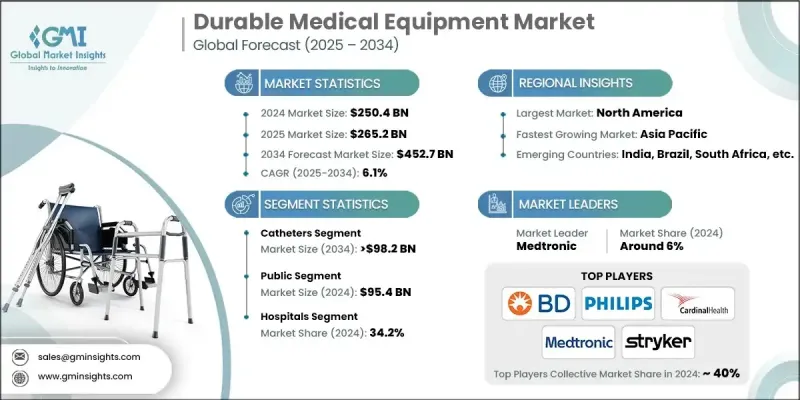

2024 年全球耐用医疗设备市场价值为 2,504 亿美元,预计到 2034 年将以 6.1% 的复合年增长率成长至 4,527 亿美元。

全球慢性病盛行率上升、医疗技术进步、居家医疗保健需求成长以及有利的报销政策是推动市场成长的主要因素。对復健、以患者为中心的照护以及符合人体工学且易于使用的设备日益重视,进一步刺激了市场需求。人口老化也增加了对专用设备的需求。各公司正积极进行产品创新,整合新型材料,并建立区域合作伙伴关係以拓展地理市场。技术整合正成为市场的核心驱动力,如今的设备提供无线监测、人工智慧诊断和行动应用程式连接功能,从而实现即时资料共享和个人化护理。随着医疗保健向数位化和价值导向模式转型,科技增强型耐用医疗设备对于高效、以患者为中心的治疗至关重要,这为差异化和市场成长开闢了新的机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2504亿美元 |

| 预测值 | 4527亿美元 |

| 复合年增长率 | 6.1% |

2024年,导尿管市场占有率预计将达到22.3%,主要得益于外科手术和泌尿科相关治疗数量的成长。导尿管在引流液体、给药和建立循环系统路径方面发挥着至关重要的作用。它们广泛应用于医院、长期照护机构和家庭照护场所,尤其适用于尿液滞留、心血管疾病或接受透析治疗的患者。

2024年,公共医疗支付方市场规模预估为954亿美元。公共医疗支付者包括政府支持的医疗项目和保险计划,为受保人员提供医疗保障。他们通常透过大量采购的方式进行价格谈判,并强调提供经济实惠的基本耐用医疗设备(DME)。公共医疗支付方在扩大医疗服务覆盖范围方面发挥着至关重要的作用,尤其是在低收入和农村地区,其报销政策直接影响产品的供应和市场需求。

2024年,北美耐用医疗设备市场占了相当大的份额,这主要得益于其先进的医疗基础设施、高昂的医疗支出以及庞大的老龄人口。糖尿病、心血管疾病和呼吸系统疾病等慢性病的高发生率推动了医疗设备的长期使用。家庭医疗保健和数位健康技术的日益普及加速了对便携式连网设备的需求。包括联邦医疗保险(Medicare)和联邦医疗补助(Medicaid)在内的政府倡议进一步支持了人们获得必要的耐用医疗设备,尤其是老年人和残疾人群体。

全球耐久性医疗设备市场的主要参与者包括B Braun、Baxter、BD、Cardinal Health、CAREX、Coloplast、COMPASS HEALTH、ConvaTec、Drive DeVilbiss Healthcare、Getinge、Graham-Field、INTCO MEDICAL、INVACARE、Koninklijke Philips、WISEMED 或ReLINE、Rexax、Et.市场领导者专注于产品创新,开发符合人体工学、患者客製化和互联互通的设备,以增强易用性并改善临床疗效。各公司大力投资研发,将人工智慧、无线监测和行动连接功能整合到设备中,在市场中脱颖而出。与区域分销商、医疗服务提供者和技术公司建立策略合作伙伴关係和合作,有助于扩大地域覆盖范围并加快市场渗透速度。各公司也利用併购来扩展产品组合併加强供应链。此外,各公司也注重监管合规、品质认证和政府报销计划,以确保市场信誉和准入。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 患者越来越倾向于选择居家护理

- 全球慢性病盛行率不断上升

- 老年人口不断增加

- 产品技术进步

- 产业陷阱与挑战

- 高昂的设备成本和价格负担能力方面的挑战

- 对儿科产品的需求不断增长

- 机会

- 人工智慧/机器学习整合和预测分析

- 新兴市场扩张与基础建设发展

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 投资环境

- 报销方案

- 医疗服务模式转型

- 个人化医疗和精准医疗保健应用

- 软体即医疗器材 (SaMD) 整合分析

- 波特的分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 主要趋势

- 个人行动装置

- 轮椅和电动代步车

- 拐杖和手杖

- 沃克

- 其他个人行动装置

- 监测和治疗设备

- 氧气设备

- 血糖分析仪

- 生命征象监测仪

- 点滴帮浦

- 持续性呼吸道正压通气(CPAP)装置

- 雾化器

- 其他监测和治疗设备

- 浴室安全装置

- 医疗家具

- 成人尿垫

- 吸乳器

- 导管

- 耗材和配件

- 其他产品

第六章:市场估计与预测:依支付方划分,2021-2034年

- 主要趋势

- 民众

- 私人的

- 自费

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 医院

- 家庭医疗保健

- 门诊手术中心

- 其他最终用途

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- B Braun

- Baxter

- BD

- Cardinal Health

- CAREX

- Coloplast

- COMPASS HEALTH

- convaTec

- drive DeVilbiss Healthcare

- Getinge

- graham-field

- INTCO MEDICAL

- INVACARE

- Koninklijke Philips

- MEDLINE

- Medtronic

- ResMed

- Stryker

- SUNRISE MEDICAL

The Global Durable Medical Equipment Market was valued at USD 250.4 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 452.7 billion by 2034.

Market growth is driven by the rising prevalence of chronic illnesses worldwide, advancements in medical technology, the growing preference for home healthcare, and supportive reimbursement policies. Increasing emphasis on rehabilitation, patient-centered care, and ergonomic, user-friendly equipment is further fueling demand. The aging population also contributes to the need for specialized devices. Companies are actively innovating products, integrating novel materials, and forming regional partnerships to expand geographically. Technological integration is becoming a core market driver, with devices now offering wireless monitoring, AI-powered diagnostics, and mobile app connectivity to enable real-time data sharing and personalized care. As healthcare shifts toward digital and value-based models, technology-enhanced DME is increasingly critical for efficient, patient-focused treatment, opening new opportunities for differentiation and market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $250.4 Billion |

| Forecast Value | $452.7 Billion |

| CAGR | 6.1% |

The catheters segment held a 22.3% share in 2024, driven by the growing number of surgical procedures and urology-related treatments. Catheters serve essential roles in draining fluids, administering medication, and providing circulatory system access. They are widely used across hospitals, long-term care facilities, and home care settings, particularly among patients with urinary retention, cardiovascular conditions, or those undergoing dialysis.

The public payer segment was valued at USD 95.4 billion in 2024. Public payers include government-backed health programs and insurance plans that provide coverage for insured individuals. They often negotiate bulk pricing and emphasize cost-effective essential DME. Public payers are crucial in expanding access, especially in low-income and rural areas, with reimbursement policies directly influencing product availability and market demand.

North America Durable Medical Equipment Market held a substantial share in 2024, owing to advanced healthcare infrastructure, high medical expenditure, and a significant elderly population. The prevalence of chronic illnesses such as diabetes, cardiovascular disorders, and respiratory diseases drives long-term equipment use. The growing adoption of home healthcare and digital health technologies has accelerated demand for portable, connected devices. Government initiatives, including Medicare and Medicaid, further support access to essential DME products, particularly for geriatric and disabled populations.

Prominent players in the Global Durable Medical Equipment Market include B Braun, Baxter, BD, Cardinal Health, CAREX, Coloplast, COMPASS HEALTH, ConvaTec, Drive DeVilbiss Healthcare, Getinge, Graham-Field, INTCO MEDICAL, INVACARE, Koninklijke Philips, MEDLINE, Medtronic, ResMed, Stryker, and SUNRISE MEDICAL. Market leaders focus on product innovation, developing ergonomic, patient-specific, and connected devices to enhance usability and improve clinical outcomes. Companies invest heavily in R&D to integrate AI, wireless monitoring, and mobile connectivity into their equipment, differentiating themselves in the market. Strategic partnerships and collaborations with regional distributors, healthcare providers, and technology firms allow broader geographic reach and faster market penetration. Firms also leverage mergers and acquisitions to expand portfolios and strengthen supply chains. Focus on regulatory compliance, quality certifications, and government reimbursement programs to ensure market credibility and access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Payer trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising patient preference for home-based care

- 3.2.1.2 Increasing prevalence of chronic diseases across the globe

- 3.2.1.3 Growing geriatric population

- 3.2.1.4 Technological advancements in products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device costs and affordability challenges

- 3.2.2.2 Growing demand for pediatric-focused products

- 3.2.3 Opportunities

- 3.2.3.1 AI/ML integration and predictive analytics

- 3.2.3.2 Emerging markets expansion and infrastructure development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Investment landscape

- 3.7 Reimbursement scenario

- 3.8 Healthcare delivery model transformation

- 3.9 Personalized medicine and precision healthcare applications

- 3.10 Software as medical device (SaMD) integrated analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Personal mobility devices

- 5.2.1 Wheelchair and scooter

- 5.2.2 Crutches and canes

- 5.2.3 Walkers

- 5.2.4 Other personal mobility devices

- 5.3 Monitoring and therapeutic devices

- 5.3.1 Oxygen equipment

- 5.3.2 Blood glucose analyzers

- 5.3.3 Vital sign monitors

- 5.3.4 Infusion pumps

- 5.3.5 Continuous positive airway pressure (CPAP) devices

- 5.3.6 Nebulizers

- 5.3.7 Other monitoring and therapeutic devices

- 5.4 Bathroom safety devices

- 5.5 Medical furniture

- 5.6 Incontinent pads

- 5.7 Breast pumps

- 5.8 Catheters

- 5.9 Consumables and accessories

- 5.10 Other products

Chapter 6 Market Estimates and Forecast, By Payer, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Public

- 6.3 Private

- 6.4 Out-of-pocket

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Home healthcare

- 7.4 Ambulatory surgical centers

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Baxter

- 9.3 BD

- 9.4 Cardinal Health

- 9.5 CAREX

- 9.6 Coloplast

- 9.7 COMPASS HEALTH

- 9.8 convaTec

- 9.9 drive DeVilbiss Healthcare

- 9.10 Getinge

- 9.11 graham-field

- 9.12 INTCO MEDICAL

- 9.13 INVACARE

- 9.14 Koninklijke Philips

- 9.15 MEDLINE

- 9.16 Medtronic

- 9.17 ResMed

- 9.18 Stryker

- 9.19 SUNRISE MEDICAL

医疗耐用设备市场:2026-2032年全球市场预测(按产品类型、最终用户、分销管道和购买方式划分)

医疗耐用设备市场:2026-2032年全球市场预测(按产品类型、最终用户、分销管道和购买方式划分) 耐用医疗设备(DME)市场规模、份额、趋势和预测:按产品、最终用途和地区划分,2026-2034年

耐用医疗设备(DME)市场规模、份额、趋势和预测:按产品、最终用途和地区划分,2026-2034年 2026年全球耐用医疗设备市场报告

2026年全球耐用医疗设备市场报告 2026-2034年全球耐用医疗设备市场规模、份额、趋势和成长分析报告

2026-2034年全球耐用医疗设备市场规模、份额、趋势和成长分析报告 全球耐用医疗设备市场:市场规模、份额和趋势分析(按产品、最终用途和地区划分),细分市场预测(2026-2033 年)美国呼吸系统耐用医疗设备市场规模、份额和趋势分析报告:按产品供应、分销/服务管道、主要州和细分市场预测,2026-2033年美国耐用医疗设备市场规模、份额和趋势分析报告:按产品、最终用途和细分市场预测(2026-2033 年)

全球耐用医疗设备市场:市场规模、份额和趋势分析(按产品、最终用途和地区划分),细分市场预测(2026-2033 年)美国呼吸系统耐用医疗设备市场规模、份额和趋势分析报告:按产品供应、分销/服务管道、主要州和细分市场预测,2026-2033年美国耐用医疗设备市场规模、份额和趋势分析报告:按产品、最终用途和细分市场预测(2026-2033 年) 耐用医疗设备市场规模、份额和成长分析(按产品、支付方、最终用途和地区划分)-2026-2033年产业预测

耐用医疗设备市场规模、份额和成长分析(按产品、支付方、最终用途和地区划分)-2026-2033年产业预测 全球耐用医疗设备市场:洞察、竞争格局、市场预测:2030年

全球耐用医疗设备市场:洞察、竞争格局、市场预测:2030年