|

市场调查报告书

商品编码

1885927

家用电器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Electric Household Appliances Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

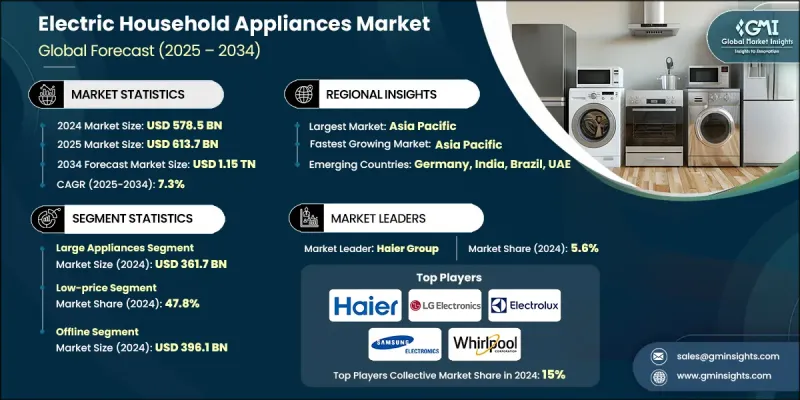

2024 年全球家用电器市场价值为 5,785 亿美元,预计到 2034 年将以 7.3% 的复合年增长率增长至 1.15 兆美元。

在科技进步的驱动下,家电产业正经历快速转型,科技进步正在重塑日常生活的便利性和效率。具备物联网连接、人工智慧驱动的自动化和语音控制功能的智慧家电正无缝融入智慧家庭生态系统,实现远端监控、预测性维护和个人化设定。製造商日益重视节能技术,以实现永续发展目标并遵守环境法规,同时吸引具有环保意识的消费者。城市化进程正在影响家电设计,小型住宅催生了对紧凑型多功能设备的需求,例如洗衣干衣一体机和节省空间的厨房电器。双薪家庭和快节奏的生活方式进一步推动了自动化和智慧设备的普及,这些设备能够节省时间并减少体力劳动。此外,消费者对现代设计、美观和高端功能的需求也在推动创新,因为城市消费者寻求兼具时尚外观和卓越性能的家电。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 5785亿美元 |

| 预测值 | 1.15兆美元 |

| 复合年增长率 | 7.3% |

2024年,大型家电市场规模达3,617亿美元。该市场涵盖冰箱、洗衣机、烤箱和空调等产品,由于其必需品的特性,即使在经济低迷时期,大型家电仍然是消费者的优先购买选择,因此占据市场主导地位。产品更新换代以及消费者向节能智慧型机型升级的需求,持续推动该市场的营收成长。

2024年,低价产品市占率达47.8%。这个细分市场主要由新兴市场和农村地区对价格高度敏感的消费者所驱动,在这些地区,价格实惠比高级功能更为重要。风扇、熨斗和简易厨房电器等具备基本功能和耐用性的产品被视为家庭必需品,销售可观。

美国家用电器市场占66.8%的市场份额,预计2024年市场规模将达860亿美元。美国市场需求成长的驱动因素包括:智慧环保电器的日益普及、物联网和人工智慧控制技术的进步,以及消费者对永续性和能源效率日益增长的关注。此外,生活方式的改变,例如房屋装修增加和居家时间延长,也促进了高端电器的消费。

全球家用电器市场的主要参与者包括日立、伊莱克斯、LG电子、美的集团、沃尔顿集团、三星电子、博世、松下、夏普、格力电器、惠而浦、博世家电、海尔集团、西门子和美诺。这些公司正采取多种策略来巩固市场地位并扩大市场占有率。他们大力投资研发,以提高能源效率、增强智慧功能并整合人工智慧。策略合作、併购有助于拓展分销网络并渗透新兴市场。产品组合多元化,尤其註重多功能和节省空间的电器,以满足城市消费者的需求。为了吸引具有环保意识的消费者,各公司强调永续生产实践、环保认证以及遵守全球能源标准。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 技术进步

- 都市化与生活方式的改变

- 可支配所得增加

- 产业陷阱与挑战

- 前期成本高

- 监理复杂性

- 机会

- 智慧互联家电

- 节能环保的解决方案

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 大型家电

- 冰箱

- 烹饪用具

- 洗衣设备

- 清洁设备

- 气候控制设备

- 小家电

- 烤麵包机

- 咖啡机

- 搅拌机和搅拌器

- 铁

- 吹风机

- 水过滤器

- 其他(电水壶、蒸笼等)

第六章:市场估计与预测:依价格划分,2021-2034年

- 主要趋势

- 低的

- 中等的

- 高的

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 住宅

- 商业的

第八章:市场估算与预测:依配销通路划分,2021-2034年

- 主要趋势

- 在线的

- 电子商务

- 公司网站

- 离线

- 大型零售商店

- 超市/大型超市

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- BSH Hausgerate

- Electrolux

- Gree Electric Appliances

- Haier Group

- Hitachi

- LG Electronics

- Midea Group

- Miele

- Panasonic

- Robert Bosch

- Samsung Electronics

- Sharp

- Siemens

- Walton Group

- Whirlpool

The Global Electric Household Appliances Market was valued at USD 578.5 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 1.15 trillion by 2034.

The industry is undergoing rapid transformation, driven by technological advancements that are reshaping convenience and efficiency in everyday living. Smart appliances featuring IoT connectivity, AI-driven automation, and voice control are integrating seamlessly into smart home ecosystems, enabling remote monitoring, predictive maintenance, and personalized settings. Manufacturers are increasingly prioritizing energy-efficient technologies to meet sustainability goals and comply with environmental regulations, while appealing to eco-conscious consumers. Urbanization is influencing appliance design, with smaller dwellings creating demand for compact, multi-functional devices such as washer-dryer combinations and space-saving kitchen appliances. Dual-income households and busy lifestyles are further boosting the adoption of automated and smart devices that save time and reduce manual effort. Additionally, consumer demand for modern designs, aesthetics, and premium features is shaping innovation, as urban buyers seek appliances that combine style with advanced performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $578.5 Billion |

| Forecast Value | $1.15 Trillion |

| CAGR | 7.3% |

In 2024, the large appliances segment generated USD 361.7 billion. This segment, which includes refrigerators, washing machines, ovens, and air conditioners, dominates due to its essential nature, making them a priority purchase even during economic downturns. Replacement cycles and consumer upgrades toward energy-efficient and smart models continue to drive revenue growth in this segment.

The low-price segment held a 47.8% share in 2024. This segment is primarily driven by highly price-sensitive consumers in emerging markets and rural areas, where affordability takes precedence over advanced features. Products with basic functionality and durability, such as fans, irons, and simple kitchen appliances, are considered household essentials, generating significant sales volumes.

United States Electric Household Appliances Market held a 66.8% share, generating USD 86 billion in 2024. Demand in the U.S. is fueled by the growing popularity of smart and eco-friendly appliances, advancements in IoT and AI-enabled controls, and increasing consumer focus on sustainability and energy efficiency. Lifestyle changes, such as increased home renovations and more time spent at home, are also boosting the consumption of premium appliances.

Key players in the Global Electric Household Appliances Market include Hitachi, Electrolux, LG Electronics, Midea Group, Walton Group, Samsung Electronics, Bosch, Panasonic, Sharp, Gree Electric Appliances, Whirlpool, BSH Hausgerate, Haier Group, Siemens, and Miele. Companies in the Electric Household Appliances Market are employing several strategies to strengthen their presence and expand market share. They are investing heavily in research and development to enhance energy efficiency, smart features, and AI integration. Strategic partnerships, mergers, and acquisitions help broaden distribution networks and penetrate emerging markets. Product portfolio diversification, focusing on multi-functional and space-saving appliances, caters to urban consumers. Firms emphasize sustainable manufacturing practices, eco-friendly certifications, and compliance with global energy standards to appeal to environmentally conscious buyers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Price

- 2.2.4 End use

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements

- 3.2.1.2 Urbanization & changing lifestyles

- 3.2.1.3 Rising disposable income

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial costs

- 3.2.2.2 Regulatory complexity

- 3.2.3 Opportunities

- 3.2.3.1 Smart & connected appliances

- 3.2.3.2 Energy-efficient & sustainable solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Million units)

- 5.1 Key trends

- 5.2 Large appliances

- 5.2.1 Refrigerators

- 5.2.2 Cooking appliances

- 5.2.3 Laundry appliances

- 5.2.4 Cleaning appliances

- 5.2.5 Climate control appliances

- 5.3 Small appliances

- 5.3.1 Toasters

- 5.3.2 Coffee makers

- 5.3.3 Blenders & mixers

- 5.3.4 Irons

- 5.3.5 Hair dryers

- 5.3.6 Water filters

- 5.3.7 Others (electric kettles, steamers, etc.)

Chapter 6 Market Estimates and Forecast, By Price, 2021 - 2034 (USD Billion) (Million units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Million units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Million units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Company website

- 8.3 Offline

- 8.3.1 Mega retail stores

- 8.3.2 Supermarket/hypermarket stores

- 8.3.3 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Million units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 BSH Hausgerate

- 10.2 Electrolux

- 10.3 Gree Electric Appliances

- 10.4 Haier Group

- 10.5 Hitachi

- 10.6 LG Electronics

- 10.7 Midea Group

- 10.8 Miele

- 10.9 Panasonic

- 10.10 Robert Bosch

- 10.11 Samsung Electronics

- 10.12 Sharp

- 10.13 Siemens

- 10.14 Walton Group

- 10.15 Whirlpool