|

市场调查报告书

商品编码

1892669

乳清蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Whey Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

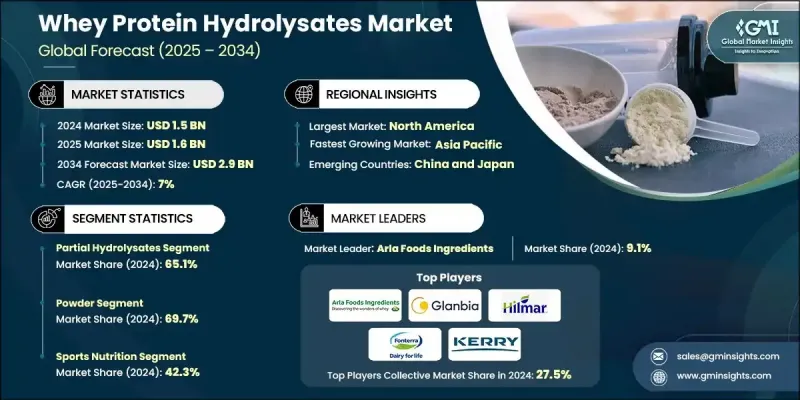

2024 年全球乳清蛋白水解物市场价值为 15 亿美元,预计到 2034 年将以 7% 的复合年增长率增长至 29 亿美元。

随着消费者转向吸收迅速、消化率高且致敏性低的蛋白质成分,市场需求持续成长。乳清蛋白水解物是透过对乳清蛋白浓缩物或分离物进行可控酶解而製成的,将蛋白质分解成更小的胜肽和游离氨基酸,从而提供更佳的生理益处。乳清蛋白水解物在婴幼儿配方奶粉、运动营养、医用营养和功能性食品等领域的应用迅速扩展。全球对乳糖不耐症的日益关注(乳糖不耐症影响着很大一部分成年人口)进一步推动了水解乳蛋白的普及。蛋白质成分产业的这一细分领域依赖于专业的加工系统和严格的品质标准,製造商根据特定的性能需求设计高度一致的胜肽组成和分子量分布。水解程度通常从轻微到深度不等,取决于所需的特性,例如溶解度、耐热性、乳化性能和整体生物利用度。加工方法的进步和消费者对高性能营养成分日益增长的兴趣将继续推动市场的发展。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 15亿美元 |

| 预测值 | 29亿美元 |

| 复合年增长率 | 7% |

2024年,部分水解物市占率达到65.1%,预计到2034年将以6.9%的复合年增长率成长。这些成分保持着均衡的结构,在提高消化率和降低致敏性的同时,保留了理想的功能特性,使其在食品和饮料配方中广泛应用。与深度水解产品相比,部分水解物的苦味更低,从而提高了配方的灵活性,并减少了对添加香精的需求。

2024年,运动营养品市占率达到42.3%,预计到2034年将以7.3%的复合年增长率成长。水解乳清蛋白因其吸收速度快、对肌肉蛋白质合成有显着促进作用以及在运动后恢復中的作用而广受青睐。消费者对蛋白质品质的高度认可以及零售和电商通路的完善,共同推动了该品类的持续成长。

2024 年,北美乳清蛋白水解物市场将占据 36.9% 的市场份额,这得益于其发达的营养产业、强大的加工能力以及对优质蛋白质原料的高接受度。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 运动营养市场及蛋白质补充品市场正蓬勃发展

- 临床营养需求不断成长

- 消费者更青睐成分清洁、功能性强的产品。

- 产业陷阱与挑战

- 生产成本高且对价格敏感

- 苦味和感官上的挑战限制了消费者的接受度

- 市场机会

- 富含生物活性胜肽的水解物有益心血管健康

- 富含乳脂球膜的水解物有益于认知和肌肉健康

- 混合乳蛋白-植物蛋白水解物混合物

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按形式

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依水解度划分,2021-2034年

- 部分水解物

- 高度水解

第六章:市场估算与预测:依形式划分,2021-2034年

- 粉末

- 液体

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 婴儿营养

- 运动营养

- 蛋白质粉

- 即饮奶昔

- 临床营养

- 功能性食品和饮料

- 高蛋白饮料

- 烘焙和糖果

- 乳製品

- 即用型粉末

- 动物营养

- 家畜

- 宠物食品

第八章:市场估算与预测:依配销通路划分,2021-2034年

- 零售通路

- 超市和大型超市

- 犹太洁食专卖店

- 便利商店

- 线上和电子商务

- 直接面向消费者的销售

- 品牌网站销售

- 订阅服务

- 电子商务平台

- 餐饮服务管道

第九章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Arla Foods Ingredients

- Glanbia Nutritionals

- Hilmar Ingredients

- Fonterra Co-operative Group

- Kerry Group

- FrieslandCampina Ingredients

- Nestle Health Science

- Carbery Group

- Agropur Ingredients

- Lactalis Ingredients

- Saputo Dairy Ingredients

- Ingredia

The Global Whey Protein Hydrolysates Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 2.9 billion by 2034.

Demand continues to expand as consumers shift toward protein ingredients that offer rapid absorption, high digestibility, and reduced allergenic potential. Whey protein hydrolysates are produced through controlled enzymatic hydrolysis of whey protein concentrate or isolate, breaking down the proteins into smaller peptides and free amino acids that deliver improved physiological benefits. Their adoption has accelerated across infant formulas, sports nutrition, medical nutrition, and functional food applications. Growing global awareness of lactose intolerance, which affects a large portion of the adult population, further supports the shift toward hydrolyzed dairy proteins. This segment of the protein ingredients industry relies on specialized processing systems and strict quality criteria, as manufacturers design highly consistent peptide compositions and molecular weight profiles tailored to specific performance needs. Hydrolysis levels typically range from mild to extensive, depending on intended characteristics such as solubility, heat tolerance, emulsification behavior, and overall bioavailability. Advancements in processing methods and rising consumer interest in high-performance nutritional ingredients continue to shape the evolution of the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 7% |

The partial hydrolysates segment held 65.1% share in 2024 and is projected to grow at a CAGR of 6.9% through 2034. These ingredients maintain a balanced structure, offering improved digestibility and reduced allergenicity while preserving desirable functional traits that support widespread use in food and beverage formulations. Their lower bitterness compared to extensively hydrolyzed products increases formulation flexibility and reduces the need for added flavor solutions.

The sports nutrition segment accounted for a 42.3% share in 2024 and is anticipated to grow at a CAGR of 7.3% through 2034. Hydrolyzed whey proteins are widely preferred in this category due to their faster uptake rate, strong impact on muscle protein synthesis, and role in post-exercise recovery. High consumer recognition of protein quality and established sales channels across retail and e-commerce contribute to sustained segment momentum.

North America Whey Protein Hydrolysates Market held a 36.9% share in 2024, supported by a well-developed nutrition industry, strong processing capabilities, and high adoption of premium protein ingredients.

Major companies active in the Whey Protein Hydrolysates Market include Arla Foods Ingredients, Glanbia Nutritionals, Kerry Group, Hilmar Ingredients, Saputo Dairy Ingredients, Fonterra Co-operative Group, FrieslandCampina Ingredients, Nestle Health Science, Agropur Ingredients, Ingredia, Lactalis Ingredients, and Carbery Group. Companies competing in the Whey Protein Hydrolysates Market are prioritizing advanced enzymatic technologies to create differentiated peptide profiles with enhanced functional and nutritional performance. Many manufacturers are scaling production capacity and upgrading process controls to maintain consistent hydrolysis levels and meet rising demand from sports, infant, and clinical nutrition sectors. Strategic product diversification, including formulations with improved sensory characteristics, supports broader commercial adoption. Firms are also strengthening long-term partnerships with food, beverage, and supplement brands to secure stable supply channels.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 Degree of hydrolysis

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing sports nutrition market & protein supplementation

- 3.2.1.2 Increasing clinical nutrition demand

- 3.2.1.3 Consumer preference for clean label & functional ingredients

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & price sensitivity

- 3.2.2.2 Bitterness & sensory challenges limiting consumer acceptance

- 3.2.3 Market opportunities

- 3.2.3.1 Bioactive peptide-enriched hydrolysates for cardiovascular health

- 3.2.3.2 MFGM-enriched hydrolysates for cognitive & muscle health

- 3.2.3.3 Hybrid dairy-plant protein hydrolysate blends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By form

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Degree of Hydrolysis, 2021-2034 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Partial hydrolysates

- 5.3 Highly hydrolyzed

Chapter 6 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 Infant nutrition

- 7.3 Sports nutrition

- 7.3.1 Protein Powders

- 7.3.2 Ready to drink shakes

- 7.4 Clinical nutrition

- 7.5 Functional foods & beverages

- 7.5.1 High-Protein Beverages

- 7.5.2 Bakery & Confectionery

- 7.5.3 Dairy Products

- 7.5.4 Ready-to-Mix Powders

- 7.6 Animal nutrition

- 7.6.1 Livestock

- 7.6.2 Pet food

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 Retail channels

- 8.2.1 Supermarkets and hypermarkets

- 8.2.2 Specialty kosher stores

- 8.2.3 Convenience stores

- 8.3 Online and E-commerce

- 8.3.1 Direct-to-consumer sales

- 8.3.2 Brand website sales

- 8.3.3 Subscription services

- 8.3.4 E-commerce platforms

- 8.4 Foodservice channels

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arla Foods Ingredients

- 10.2 Glanbia Nutritionals

- 10.3 Hilmar Ingredients

- 10.4 Fonterra Co-operative Group

- 10.5 Kerry Group

- 10.6 FrieslandCampina Ingredients

- 10.7 Nestle Health Science

- 10.8 Carbery Group

- 10.9 Agropur Ingredients

- 10.10 Lactalis Ingredients

- 10.11 Saputo Dairy Ingredients

- 10.12 Ingredia