|

市场调查报告书

商品编码

1892710

汽车共享平台技术市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Car-Sharing Platform Technologies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

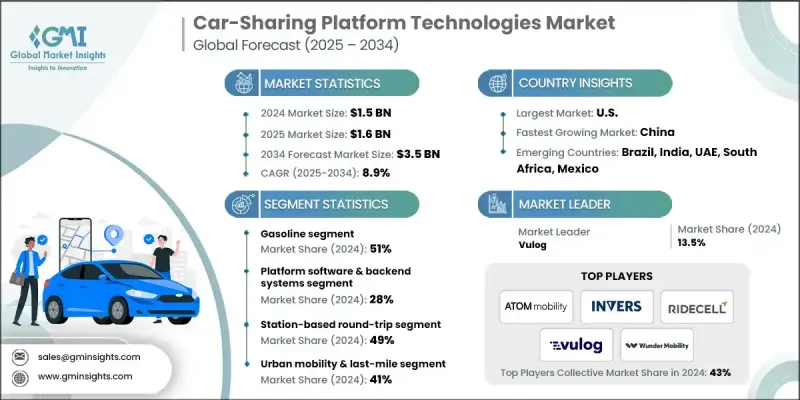

2024 年全球汽车共享平台技术市场价值为 15 亿美元,预计到 2034 年将以 8.9% 的复合年增长率增长至 35 亿美元。

城市密度不断上升,以及人们对更便利的交通模式的需求日益增长,推动了共享出行的发展。这种交通模式旨在减少拥挤街道上的私家车数量,同时提供更便利的旅行体验。随着城市努力应对交通拥堵、停车需求激增以及出行偏好的转变,消费者正逐渐转向由数位生态系统支援的共享车队。从远端资讯处理和连网车辆系统到人工智慧驱动的车队管理,现代平台技术正在改善营运商维护车辆、监控使用情况和降低营运成本的方式。数据驱动的洞察支持车辆重新定位、动态定价和高效调度,最终提高车队可用性并减少停机时间。随着共享出行的发展,订阅和按次付费模式吸引了那些优先考虑灵活性而非所有权的用户。流畅的行动应用程式、整合支付和社交验证功能进一步降低了用户接受共享出行的门槛。年轻用户更喜欢便捷的按需出行,并且越来越多地依赖共享出行进行日常出行和非高峰时段出行,这增强了城市和郊区对共享出行的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 15亿美元 |

| 预测值 | 35亿美元 |

| 复合年增长率 | 8.9% |

2024年,汽油车市占率达到51%,预计2025年至2034年将以8%的复合年增长率成长。由于汽油动力车队拥有可靠的续航里程和快速的加油能力,因此需求仍然旺盛,尤其适用于充电网路覆盖有限的地区。平台技术透过即时车辆监控、燃油效率分析和智慧路线规划,提升了汽油动力车队的性能,延长了车队的使用寿命,同时降低了营运成本。

平台软体和后端系统细分市场在2024年占据28%的市场份额,预计到2034年将以9.8%的复合年增长率成长。营运商越来越依赖自动化软体堆迭来处理车队调度、门禁控制、路线规划和驾驶员身份验证。这些系统显着减少了人工操作,提高了准确性,并支援更高的车队利用率。即时分析也使得预测性地平衡车辆配置成为可能,并在竞争激烈的市场中保持一致的服务水准。

美国汽车共享平台技术市场占据86%的市场份额,预计2024年将创造5.074亿美元的市场规模。人口高度集中、停车位有限以及交通成本不断上涨,促使美国主要都会区对灵活的出行方式需求日益增长。汽车共享技术提供了一种灵活、经济高效的选择,符合永续发展目标以及人们对车辆所有权态度的转变。

目录

第一章:方法论

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 都市化及朝向共享出行方式的转变

- 互联汽车技术的发展

- 电动车共享车队的普及率不断提高

- 多模式交通生态系的整合

- 产业陷阱与挑战

- 高昂的部署和整合成本

- 监理合规的复杂性

- 故意破坏、滥用和资产损坏风险

- 低利用率下获利能力低

- 市场机会

- 拓展新兴智慧城市市场

- 电动车与脱碳政策

- 企业流动性计划

- MaaS 和 API 货币化

- 成长驱动因素

- 成长潜力分析

- 主要市场趋势和颠覆性因素

- 未来市场趋势

- 监管环境

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 目前技术

- 即时车队管理平台

- 连网车辆远端资讯处理

- 基于行动装置的预订和存取系统

- 整合支付和计费解决方案

- 新兴技术

- 人工智慧驱动的车队优化和预测性维护

- 自动驾驶车辆集成

- 基于区块链的智能合约

- 支援5G的车联网(V2X)通信

- 目前技术

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 市场吸引力分析

- 按技术类型分類的市场吸引力

- 商业模式的市场吸引力

- 按地区分類的市场吸引力

- 市场饱和指数

- 采纳障碍热图

- 成本分析与获利能力洞察

- 总拥有成本 (TCO) 分析

- 投资报酬率(ROI)分析

- 成本结构细分

- 获利能力模型与单位经济效益

- 成本降低策略和最佳实践

- 产业基准和关键绩效指标

- 营运绩效指标

- 使用者体验指标

- 财务绩效指标

- 技术性能指标

- 战略框架与决策工具

- 技术选择框架

- 自建、购买或合作决策框架

- 市场进入策略框架

- 规模化与成长策略框架

- 数位转型路线图

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依技术划分,2021-2034年

- 平台软体和后端系统

- 行动和用户介面应用程式

- 车载资讯系统和物联网硬体

- 车辆出入控制系统

- 支付和帐单系统

- 车队营运与优化系统

- 其他的

第六章:市场估算与预测:以推进方式划分,2021-2034年

- 汽油

- 柴油引擎

- 纯电动车

- 插电式混合动力汽车

- 戊型肝炎病毒

第七章:市场估计与预测:依营运模式划分,2021-2034年

- 车站往返

- 车站单行道

- 居家区域汽车共享

- 自由浮动单向

- 点对点

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 城市交通与最后一公里

- MaaS平台集成

- 企业车队管理

- 其他的

第九章:市场估算与预测:依最终用途划分,2021-2034年

- 汽车共享营运商

- 汽车原厂设备製造商

- 公共交通管理部门

- 技术平台提供商和整合商

- 其他的

第十章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- 全球参与者

- ATOM

- Getaround

- INVERS

- Ridecell

- Smartcar

- Turo

- Unbound

- Vulog

- Wunder

- Zipcar

- 区域玩家

- Car2 Go

- DriveNow

- Modo

- GoGet

- Car Club

- GreenMobility

- Sixt Share

- ShareNow

- BlueIndy

- Communauto

- Convadis

- Fluctuo

- 新兴参与者

- BluSmart

- Zuch

- Koenigsegg

- P2 P CarShare

- Ubeeqo

- DriveMyCar

- RidePark

- Karhoo

The Global Car-Sharing Platform Technologies Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 3.5 billion by 2034.

Growth is fueled by rising urban density and the increasing need for transportation models that provide greater convenience without adding more personal vehicles to crowded streets. With cities managing congestion, soaring parking demand, and shifting mobility preferences, consumers are gravitating toward shared fleets supported by digital ecosystems. Modern platform technologies ranging from telematics and connected vehicle systems to AI-powered fleet management are improving how operators maintain vehicles, monitor usage, and reduce operating costs. Data-driven insights support vehicle repositioning, dynamic pricing, and efficient dispatching, ultimately boosting fleet availability and reducing downtime. As shared mobility evolves, subscription-based and pay-per-use options appeal to users who prioritize flexibility over ownership. Seamless mobile applications, integrated payments, and social validation features further reduce adoption barriers. Younger users prefer convenient, on-demand transportation and are increasingly relying on shared mobility for both routine and off-peak travel, strengthening demand across urban and suburban areas.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.5 Billion |

| CAGR | 8.9% |

The gasoline vehicle segment held a 51% share in 2024 and is anticipated to grow at a CAGR of 8% from 2025 to 2034. Gasoline-powered fleets remain in demand due to dependable driving range and fast refueling, making them suitable for regions where charging networks are still limited. Platform technologies improve their performance through real-time vehicle monitoring, fuel-efficiency analytics, and intelligent routing that extends fleet life while lowering operational expenses.

The platform software and backend systems segment held a 28% share in 2024 and is expected to grow at a CAGR of 9.8% through 2034. Operators increasingly rely on automated software stacks that handle fleet dispatch, access control, routing, and driver verification. These systems significantly reduce manual labor, enhance accuracy, and support higher fleet utilization. Real-time analytics also make it possible to balance vehicles predictively and maintain consistent service levels across competitive markets.

U.S Car-Sharing Platform Technologies Market held an 86% share, generating USD 507.4 million in 2024. High population concentration, limited parking, and rising traffic costs are contributing to the demand for flexible transportation alternatives across major US metropolitan areas. Car-sharing technologies offer adaptable, cost-efficient options that align with sustainability goals and changing attitudes toward vehicle ownership.

Major companies in the Global Car-Sharing Platform Technologies Market include ATOM, Convadis, Fluctuo, INVERS, Karhoo, Ridecell, Smartcar, Unbound, Vulog, and Wunder. Companies in the Car-Sharing Platform Technologies Market are reinforcing their market presence by investing heavily in integrated mobility software, enhanced telematics, and scalable backend systems. Many firms focus on expanding real-time analytics capabilities to improve vehicle repositioning, optimize asset performance, and strengthen pricing strategies. Partnerships with automakers, urban mobility planners, and payment providers help broaden platform reach and support seamless service delivery. Providers are also adding modular and customizable software features to accommodate diverse fleet models and city regulations. Continuous upgrades to app interfaces, in-app payments, and user verification tools strengthen customer experience and retention.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Propulsion

- 2.2.4 Operational model

- 2.2.5 Application

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization & shift toward shared mobility

- 3.2.1.2 Growth in connected vehicle technologies

- 3.2.1.3 Rising adoption of EV-based shared fleets

- 3.2.1.4 Integration of multimodal mobility ecosystems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High deployment & integration costs

- 3.2.2.2 Regulatory compliance complexities

- 3.2.2.3 Vandalism, misuse & asset damage risks

- 3.2.2.4 Low profitability at low utilization

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging smart-city markets

- 3.2.3.2 EV and decarbonization mandates

- 3.2.3.3 Corporate mobility programs

- 3.2.3.4 MaaS and API monetization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current Technologies

- 3.9.1.1 Real-time fleet management platforms

- 3.9.1.2 Connected vehicle telematics

- 3.9.1.3 Mobile-based booking & access systems

- 3.9.1.4 Integrated payment & billing solutions

- 3.9.2 Emerging Technologies

- 3.9.2.1 AI-powered fleet optimization & predictive maintenance

- 3.9.2.2 autonomous vehicle integration

- 3.9.2.3 blockchain-based smart contracts

- 3.9.2.4 5g-enabled vehicle-to-everything (V2X) communication

- 3.9.1 Current Technologies

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

- 3.13 Market attractiveness analysis

- 3.13.1 Market attractiveness by technology type

- 3.13.2 Market attractiveness by business model

- 3.13.3 Market attractiveness by region

- 3.13.4 Market saturation index

- 3.13.5 Adoption barriers heatmap

- 3.14 Cost analysis & profitability insights

- 3.14.1 Total cost of ownership (tco) analysis

- 3.14.2 Return on investment (roi) analysis

- 3.14.3 Cost structure breakdown

- 3.14.4 Profitability models & unit economics

- 3.14.5 Cost reduction strategies & best practices

- 3.15 Industry benchmarks & key performance indicators

- 3.15.1 Operational performance metrics

- 3.15.2 User experience metrics

- 3.15.3 Financial performance indicators

- 3.15.4 Technology performance metrics

- 3.16 Strategy frameworks & decision tools

- 3.16.1 Technology selection framework

- 3.16.2 Build vs. Buy vs. Partner decision framework

- 3.16.3 Market entry strategy framework

- 3.16.4 Scaling & growth strategy framework

- 3.16.5 Digital transformation roadmap

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Platform software & backend systems

- 5.3 Mobile & user interface applications

- 5.4 Telematics & IoT hardware

- 5.5 Vehicle access control systems

- 5.6 Payment & billing systems

- 5.7 Fleet operations & optimization systems

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 BEV

- 6.5 PHEV

- 6.6 HEV

Chapter 7 Market Estimates & Forecast, By Operational Model, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Station-based round-trip

- 7.3 Station-based one-way

- 7.4 Home-zone car-sharing

- 7.5 Free-floating one-way

- 7.6 Peer-to-peer

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Urban mobility & last-mile

- 8.3 MaaS platform integration

- 8.4 Corporate fleet management

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Car-sharing operators

- 9.3 Automotive OEMs

- 9.4 Public transport authorities

- 9.5 Technology platform providers & integrators

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 ATOM

- 11.1.2 Getaround

- 11.1.3 INVERS

- 11.1.4 Ridecell

- 11.1.5 Smartcar

- 11.1.6 Turo

- 11.1.7 Unbound

- 11.1.8 Vulog

- 11.1.9 Wunder

- 11.1.10 Zipcar

- 11.2 Regional players

- 11.2.1. Car2 Go

- 11.2.2 DriveNow

- 11.2.3 Modo

- 11.2.4 GoGet

- 11.2.5 Car Club

- 11.2.6 GreenMobility

- 11.2.7 Sixt Share

- 11.2.8 ShareNow

- 11.2.9 BlueIndy

- 11.2.10 Communauto

- 11.2.11 Convadis

- 11.2.12 Fluctuo

- 11.3 Emerging Players

- 11.3.1 BluSmart

- 11.3.2 Zuch

- 11.3.3 Koenigsegg

- 11.3.4. P2 P CarShare

- 11.3.5 Ubeeqo

- 11.3.6 DriveMyCar

- 11.3.7 RidePark

- 11.3.8 Karhoo