|

市场调查报告书

商品编码

1892729

行动支付整合平台市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Mobility Payment Integration Platforms Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

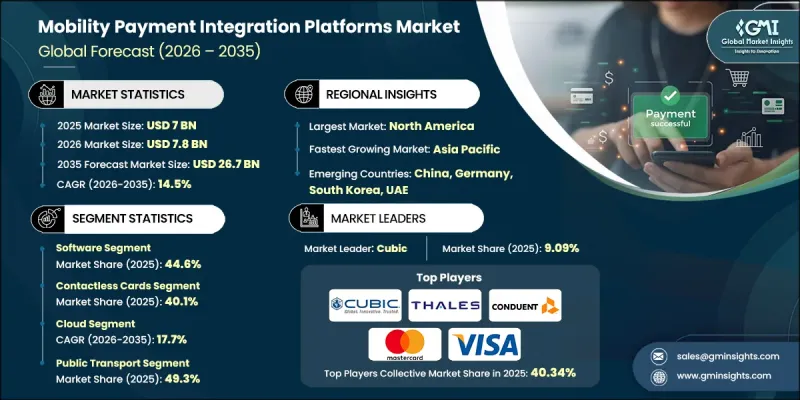

全球行动支付整合平台市场预计在 2025 年达到 70 亿美元,预计到 2035 年将以 14.5% 的复合年增长率成长至 267 亿美元。

全球城市交通系统的快速数位转型推动了这个市场的成长。交通管理部门正在加速向无现金收费模式转型,以提高营运效率、降低实体处理成本,并满足乘客对便利、快速、卫生出行体验日益增长的期望。疫情后对非接触式交易的重视进一步促进了先进支付整合技术的应用。城市越来越注重提供流畅的出行体验,最大限度地减少登车延误,并实现即时票价处理。对整合了交通网络支付、票务和验证功能的集中式平台的日益依赖,也正在重塑竞争格局。这些平台正成为现代城市交通的关键数位基础设施,为营运商提供数据驱动的票价管理、客户个人化服务和长期成本优化。随着各国政府优先发展智慧城市和永续交通,出行支付整合平台正在演变为策略工具,不仅支援更广泛的数位旅游生态系统,还能满足日益精通技术的通勤者的需求。城市中心正积极将公共交通、共享出行、私人交通服务和停车系统整合到统一的「出行即服务」(MaaS)环境中。这种整合需要强大的支付引擎,能够管理多模式票价结构、基于帐户的计费以及跨运营商的自动票价上限。随着统一出行应用的普及,能够无缝衔接多种交通服务的平台需求日益增长。将共享旅游选项纳入城市支付生态系统,并正在扩大这些平台的功能范围。这种整合有助于改善「最后一公里」出行,鼓励环保出行,并使营运商能够引入基于即时资料的灵活定价模式。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 70亿美元 |

| 预测值 | 267亿美元 |

| 复合年增长率 | 14.5% |

预计2026年至2035年间,云端市场将以17.7%的复合年增长率成长。云端基础设施因其可扩展性、较低的维护成本以及与基于帐户的票务和出行即服务(MaaS)架构的高度契合性而备受青睐。云端平台支援即时票价运算、进阶分析、远端系统更新以及第三方出行服务供应商的快速存取。人们对云端安全框架的信任度不断提高,加上符合合规要求的云端服务和混合部署模式的普及,正在加速交通管理部门和旅游运营商对云端技术的采用。

公共运输领域在2025年占总营收的49.3%,预计2026年至2035年将以13.6%的复合年增长率成长。由于帐户式票务、EMV相容支付和多模式票价整合的广泛应用,该领域仍是最大的贡献者。大众运输支付系统必须以近乎瞬时的速度处理极高的交易量,以维持客流。其他复杂因素还包括分层票价政策、转乘规则、折扣结构、地铁系统的离线功能以及跨多个机构和服务提供者的互通性。

2025年,欧洲行动支付整合平台市场规模达到18亿美元,预计2035年将以13.7%的复合年增长率成长。欧洲在整合移动出行和基于帐户的票价系统方面继续引领全球。强而有力的监管架构促进了互通性,鼓励各城市将各种交通服务整合到单一的支付生态系统中,包括跨境出行功能。非接触式支付技术的高普及率,以及成熟的数位支付基础设施,正在推动整个地区的快速应用和一致的用户体验。

目录

第一章:方法论

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 都市化进程加速与公共运输需求成长

- 消费者对非接触式和行动支付的偏好

- 政府对开放支付系统和互通性的强制性要求

- 旅游即服务 (MaaS) 平台激增

- 透过自动收费降低成本

- 产业陷阱与挑战

- 系统升级需要较高的初始资本投入

- 遗留系统整合复杂性与技术债务

- 异质系统互通性挑战

- 资料隐私与安全问题

- 市场机会

- 基于区块链的结算和智能合约自动化

- 用于非接触式车费支付的生物辨识认证

- 人工智慧驱动的动态定价与需求管理

- 与自动驾驶汽车支付系统集成

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 电子资金转帐法(E条例)

- FINTRAC MSB 法规

- 欧洲

- 2017年支付服务条例(PSRs)

- 一般资料保护条例

- 亚太地区

- 中华人民共和国网路安全法

- 日本支付服务法(PSA)

- 2007年印度支付与结算系统法案

- 拉丁美洲

- 孟加拉国中央银行第3682号通函-支付机构规则

- 金融科技法(Ley para Regular las Instituciones de Tecnologia Financiera)2018

- MEA

- 阿布达比全球市场 - 金融服务与市场监管 (FSMR)

- 金融情报中心法案(FICA)

- 北美洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利分析

- 成本細項分析

- 成本細項分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 未来展望与机会

- 新兴科技趋势

- 监理与政策演变

- 市场拓展机会

- 商业模式创新

- 市场参与者的策略要务

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2022-2035年

- 软体

- 硬体

- 验证者

- NFC终端

- 服务

- 一体化

- 咨询

第六章:市场估算与预测:依支付方式划分,2022-2035年

- 非接触式卡

- 行动钱包

- NFC

- QR 图码

- 其他数位支付方式

第七章:市场估算与预测:依部署方式划分,2022-2035年

- 云

- 现场

第八章:市场估算与预测:依应用领域划分,2022-2035年

- 大众运输

- 叫车

- 自行车共享

- 汽车共享

- 停车处

- 微移动性

第九章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 葡萄牙

- 克罗埃西亚

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 土耳其

第十章:公司简介

- 全球参与者

- Cubic Transportation Systems

- Visa

- Mastercard

- Thales

- IDEMIA

- Conduent

- HID Global

- NXP Semiconductors

- Worldline

- Indra Sistemas

- 区域玩家

- Masabi

- GMV Innovating

- Paragon ID

- INIT Innovation in Traffic Systems

- Scheidt & Bachmann

- Vix Technology

- Flowbird

- Trapeze

- AEP Ticketing

- Snapper Services

- 新兴参与者

- Littlepay

- Token Transit

- Bytemark

- Moovit

The Global Mobility Payment Integration Platforms Market is estimated at USD 7 billion in 2025 and is estimated to grow at a CAGR of 14.5% to reach USD 26.7 billion by 2035.

This market growth is shaped by the rapid digital transformation of urban mobility systems worldwide. Transit authorities are accelerating the shift toward cashless fare collection models to improve operational efficiency, reduce physical handling costs, and meet rising passenger expectations for seamless, fast, and hygienic travel experiences. The post-pandemic emphasis on touch-free transactions has further intensified the adoption of advanced payment integration technologies. Cities are increasingly focused on delivering frictionless mobility journeys that minimize boarding delays while enabling real-time fare processing. The growing reliance on centralized platforms that unify payment, ticketing, and validation across transport networks is also reshaping the competitive landscape. These platforms are becoming critical digital infrastructure for modern urban mobility, enabling data-driven fare management, customer personalization, and long-term cost optimization for operators. As governments prioritize smart city initiatives and sustainable transportation, mobility payment integration platforms are evolving into strategic tools that support broader digital mobility ecosystems while meeting the demands of increasingly tech-savvy commuters. Urban centers are actively merging public transit, shared mobility, private transport services, and parking systems into cohesive Mobility-as-a-Service environments. This integration requires robust payment engines capable of managing multimodal fare structures, account-based billing, and automated fare caps across operators. As unified mobility applications gain traction, platforms that can function seamlessly across multiple transport services are witnessing growing demand. The inclusion of shared mobility options into citywide payment ecosystems is expanding the functional scope of these platforms. This integration supports improved last-mile connectivity, encourages environmentally responsible travel behavior, and allows operators to introduce flexible pricing models driven by real-time data.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7 Billion |

| Forecast Value | $26.7 Billion |

| CAGR | 14.5% |

The cloud-based segment is expected to grow at a CAGR of 17.7% between 2026 and 2035. Cloud infrastructure is favored due to its scalability, reduced maintenance burden, and strong alignment with account-based ticketing and MaaS architectures. Cloud platforms support real-time fare computation, advanced analytics, remote system updates, and rapid onboarding of third-party mobility providers. Increasing trust in cloud security frameworks, combined with the availability of compliance-ready cloud services and hybrid deployment models, is accelerating adoption among transit authorities and mobility operators.

The public transportation segment accounted for a 49.3% share in 2025 and is forecast to grow at a CAGR of 13.6% from 2026 to 2035. This segment remains the largest contributor due to widespread implementation of account-based ticketing, EMV-compatible payments, and multimodal fare integration. Public transport payment systems must handle extremely high transaction volumes with near-instant processing speeds to maintain passenger flow. Additional complexities include layered fare policies, transfer rules, discount structures, offline functionality for underground systems, and interoperability across multiple agencies and service providers.

Europe Mobility Payment Integration Platforms Market generated USD 1.8 billion in 2025 and is expected to grow at a CAGR of 13.7% throughout 2035. Europe continues to lead global adoption of integrated mobility and account-based fare systems. Strong regulatory frameworks promoting interoperability are encouraging cities to unify various transport services under a single payment ecosystem, including cross-border travel capabilities. High penetration of contactless payment technologies, supported by a mature digital payments infrastructure, is enabling rapid adoption and consistent user experiences across the region.

Key companies operating in the Global Mobility Payment Integration Platforms Market include Mastercard, Cubic, Thales, Visa, Masabi, Siemens Mobility, Conduent, Scheidt & Bachmann, INIT Innovations, and NXP Semiconductors. Companies operating in the Mobility Payment Integration Platforms Market are strengthening their market position through continuous platform innovation, strategic partnerships, and geographic expansion. Leading players are investing heavily in cloud-native architectures, cybersecurity enhancements, and real-time analytics capabilities to support large-scale deployments. Collaboration with transit authorities, technology providers, and mobility operators is being used to accelerate multimodal integration and expand service offerings. Firms are also focusing on interoperability standards to ensure seamless deployment across diverse transport ecosystems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Payment Mode

- 2.2.4 Deployment

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerating Urbanization & Public Transit Demand

- 3.2.1.2 Consumer Preference for Contactless & Mobile Payments

- 3.2.1.3 Government Mandates for Open Payment Systems & Interoperability

- 3.2.1.4 Mobility-as-a-Service (MaaS) Platform Proliferation

- 3.2.1.5 Cost Reduction Through Automated Fare Collection

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Capital Investment for System Upgrades

- 3.2.2.2 Legacy System Integration Complexity & Technical Debt

- 3.2.2.3 Interoperability Challenges Across Heterogeneous Systems

- 3.2.2.4 Data Privacy & Security Concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Blockchain-Based Settlement & Smart Contract Automation

- 3.2.3.2 Biometric Authentication for Touchless Fare Payment

- 3.2.3.3 AI-Powered Dynamic Pricing & Demand Management

- 3.2.3.4 Integration with Autonomous Vehicle Payment Systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Electronic Fund Transfer Act (Reg E)

- 3.4.1.2 FINTRAC MSB Regulations

- 3.4.2 Europe

- 3.4.2.1 Payment Services Regulations 2017 (PSRs 2017)

- 3.4.2.2 General Data Protection Regulation (Regulation (EU) 2016/679)

- 3.4.3 Asia Pacific

- 3.4.3.1 Cybersecurity Law of the PRC

- 3.4.3.2 Payment Services Act (PSA) Japan

- 3.4.3.3 Indian Payment and Settlement Systems Act, 2007

- 3.4.4 LATAM

- 3.4.4.1 BCB Circular No. 3,682 - Payment Institutions Rules

- 3.4.4.2 FinTech Law (Ley para Regular las Instituciones de Tecnologia Financiera) 2018

- 3.4.5 MEA

- 3.4.6 ADGM - Financial Services & Markets Regulations (FSMR)

- 3.4.7 Financial Intelligence Centre Act (FICA)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Future Outlook & Opportunities

- 3.12.1 Emerging Technology Trends

- 3.12.2 Regulatory & Policy Evolution

- 3.12.3 Market Expansion Opportunities

- 3.12.4 Business Model Innovation

- 3.12.5 Strategic Imperatives for Market Participants

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Hardware

- 5.3.1 Validators

- 5.3.2 NFC terminals

- 5.4 Services

- 5.4.1 Integration

- 5.4.2 Consulting

Chapter 6 Market Estimates & Forecast, By Payment Mode, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 Contactless cards

- 6.3 Mobile wallets

- 6.4 NFC

- 6.5 QR

- 6.6 Other digital payment

Chapter 7 Market Estimates & Forecast, By Deployment, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 Public transport

- 8.3 Ride-hailing

- 8.4 Bike-sharing

- 8.5 Car-sharing

- 8.6 Parking

- 8.7 Micromobility

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Portugal

- 9.3.9 Croatia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Cubic Transportation Systems

- 10.1.2 Visa

- 10.1.3 Mastercard

- 10.1.4 Thales

- 10.1.5 IDEMIA

- 10.1.6 Conduent

- 10.1.7 HID Global

- 10.1.8 NXP Semiconductors

- 10.1.9 Worldline

- 10.1.10 Indra Sistemas

- 10.2 Regional Players

- 10.2.1 Masabi

- 10.2.2 GMV Innovating

- 10.2.3 Paragon ID

- 10.2.4 INIT Innovation in Traffic Systems

- 10.2.5 Scheidt & Bachmann

- 10.2.6 Vix Technology

- 10.2.7 Flowbird

- 10.2.8 Trapeze

- 10.2.9 AEP Ticketing

- 10.2.10 Snapper Services

- 10.3 Emerging Players

- 10.3.1 Littlepay

- 10.3.2 Token Transit

- 10.3.3 Bytemark

- 10.3.4 Moovit

AI转型(2026):全球及区域应用、企业准备度与数位支付与电子商务的扩张挑战

AI转型(2026):全球及区域应用、企业准备度与数位支付与电子商务的扩张挑战 全球数位支付市场规模、份额、趋势和成长分析报告(2026-2034)

全球数位支付市场规模、份额、趋势和成长分析报告(2026-2034) 医疗保健市场中的数位支付-全球产业规模、份额、趋势、机会和预测:按组件、部署、组织规模、地区和竞争情况划分,2021-2031年

医疗保健市场中的数位支付-全球产业规模、份额、趋势、机会和预测:按组件、部署、组织规模、地区和竞争情况划分,2021-2031年 数位支付市场规模、份额和成长分析(按产品、交易类型、支付方式、采用类型、公司规模、垂直行业和地区划分)—产业预测(2026-2033 年)中国电子商务生态系统中的人工智慧转型:整合监管、基础设施和数位支付(2025)全球电子商务与支付概览(2025):第三卷:欧洲电子商务、支付与人工智慧转型

数位支付市场规模、份额和成长分析(按产品、交易类型、支付方式、采用类型、公司规模、垂直行业和地区划分)—产业预测(2026-2033 年)中国电子商务生态系统中的人工智慧转型:整合监管、基础设施和数位支付(2025)全球电子商务与支付概览(2025):第三卷:欧洲电子商务、支付与人工智慧转型 数位支付市场按支付方式、部署模式、垂直产业、通路、最终用户、交易类型和设备类型划分-2025-2032年全球预测中东的AI市场 (2025年):引进趋势,准备情形,风险形势

数位支付市场按支付方式、部署模式、垂直产业、通路、最终用户、交易类型和设备类型划分-2025-2032年全球预测中东的AI市场 (2025年):引进趋势,准备情形,风险形势 全球数位支付市场:2032 年预测 - 按支付类型、部署方式、交易类型、公司规模、最终用户和地区进行分析

全球数位支付市场:2032 年预测 - 按支付类型、部署方式、交易类型、公司规模、最终用户和地区进行分析 全球数位支付市场

全球数位支付市场