|

市场调查报告书

商品编码

1892772

紫外线消毒系统市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)UV Disinfection System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

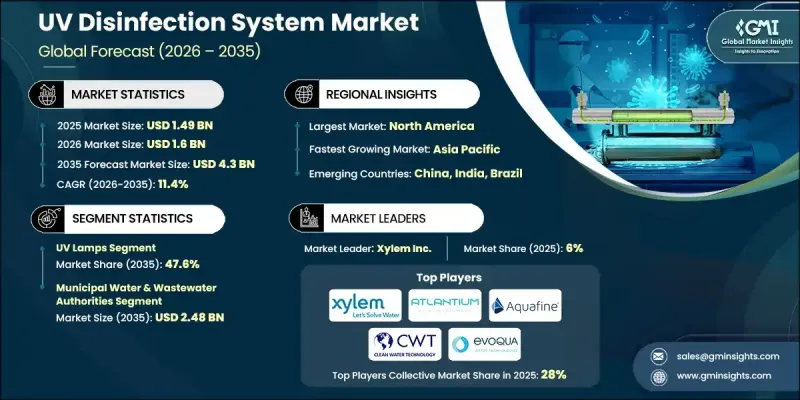

2025 年全球紫外线消毒系统市值为 14.9 亿美元,预计到 2035 年将以 11.4% 的复合年增长率增长至 43 亿美元。

对水质日益严格的监管压力正在推动这一领域的扩张,尤其是在水和废水处理领域。世界各国政府和监管机构正在实施更严格的标准,以确保更安全的饮用水和更清洁的废水排放,从而鼓励采用高效的消毒技术。紫外线消毒系统因其无需使用化学物质即可灭活多种病原体的能力而日益受到青睐。例如,美国环保署的《地表水处理规则》、欧盟的《饮用水指令》以及加拿大、澳洲和日本等国的类似法规,都要求饮用水和处理后的废水中病原体去除率更高。紫外线系统能够有效杀死细菌、病毒和原生动物,并满足这些监管要求。全球日益严格的水质管理趋势,以及传统氯化消毒方式的转变,为紫外线消毒解决方案在市政和工业应用领域创造了巨大的机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 14.9亿美元 |

| 预测值 | 43亿美元 |

| 复合年增长率 | 11.4% |

到 2035 年,紫外线灯市场将以 11.8% 的复合年增长率成长。紫外线灯的强劲普及得益于其作为重要替换组件的作用,以及 UV-C LED 技术的日益融合,这提高了系统性能并拓宽了应用范围。

市政供水和污水处理部门占据 54% 的市场份额,预计到 2025 年将创造 8.095 亿美元的收入。该部门引领市场,因为严格的法规推动了化学系统的替代,以及需要对耐氯微生物进行大规模处理。

美国紫外线消毒系统市场占 84.5% 的市场份额,2025 年市场规模达到 4.626 亿美元,预计到 2035 年将以 12.3% 的复合年增长率成长。市场扩张得益于系统升级的持续投资、高昂的劳动力成本促使自动化紫外线系统的发展,以及先进的 UV-C LED 技术在商业和市政应用中被广泛用于水和空气消毒。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 政府对水质製定了严格的法规。

- 无化学消毒的需求日益增长

- 水/污水基础设施投资不断成长

- 产业陷阱与挑战

- 高额初始资本投入(CapEx)

- UV-C LED效率的技术局限性

- 机会

- 紫外线在空气和表面消毒的应用

- 无汞UV-C LED技术的进步

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依组件划分,2022-2035年

- 紫外线灯

- 镇流器/驱动器

- 石英套管

- 控制系统

- 其他的

第六章:市场估算与预测:依流量划分,2022-2035年

- 小型(1000立方米/天)

- 中(1,000 - 50,000 立方米/天)

- 大型(>50,000立方米/天)

第七章:市场估计与预测:依技术划分,2022-2035年

- 低压紫外线

- 中压紫外线

- 脉衝紫外线

- 紫外线LED

第八章:市场估算与预测:依最终用途划分,2022-2035年

- 市政供水和污水处理机构

- 工业製造商

- 商业设施(例如,饭店、购物中心)

- 住宅/终端消费

第九章:市场估算与预测:依配销通路划分

- 直销

- 间接销售

第十章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- Advanced UV Inc.

- Alfa Laval

- Atlantic Ultraviolet Corporation

- Atlantium Technologies Ltd.

- Aquafine Corporation

- Clean Water Technology

- Evoqua Water Technologies

- ERMA FIRST ESK Engineering SA

- Heraeus Noblelight

- Industrie De Nora SPA

- LIT UV Technologies

- Pentair (Aquionics)

- Severn Trent Services

- Trojan Technologies Group

- Xylem Inc.

The Global UV Disinfection System Market was valued at USD 1.49 billion in 2025 and is estimated to grow at a CAGR of 11.4% to reach USD 4.3 billion by 2035.

Rising regulatory pressure on water quality is driving this expansion, especially in the water and wastewater treatment sectors. Governments and regulatory bodies worldwide are implementing stricter standards to ensure safer drinking water and cleaner wastewater discharge, encouraging the adoption of efficient disinfection technologies. UV disinfection systems are increasingly preferred for their ability to inactivate a wide range of pathogens without using chemicals. Regulations such as the EPA's Surface Water Treatment Rule in the US, European Drinking Water Directives, and similar mandates in countries like Canada, Australia, and Japan require higher pathogen reduction in both drinking water and treated wastewater. UV systems effectively eliminate bacteria, viruses, and protozoa, meeting these regulatory demands. The global trend toward stricter water quality management, alongside the shift from traditional chlorination, is creating significant opportunities for UV disinfection solutions in both municipal and industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.49 Billion |

| Forecast Value | $4.3 Billion |

| CAGR | 11.4% |

The UV lamps segment will grow at a CAGR of 11.8% through 2035. Their strong adoption is driven by their role as essential replacement components and the rising integration of UV-C LED technology, which improves system performance and broadens applicability.

The municipal water and wastewater authorities segment held a 54% share, generating USD 809.5 million in 2025. This segment leads the market due to stringent regulations driving the replacement of chemical-based systems and the need for large-scale treatment against chlorine-resistant microorganisms.

United States UV Disinfection System Market held 84.5% share, generating USD 462.6 million in 2025 and is expected to grow at a CAGR of 12.3% through 2035. Market expansion is supported by continuous investment in system upgrades, high labor costs favoring automated UV systems, and widespread adoption of advanced UV-C LED technologies for both water and air disinfection in commercial and municipal applications.

Major players in the Global UV Disinfection System Market include Pentair (Aquionics), Atlantic Ultraviolet Corporation, Heraeus Noblelight, Industrie De Nora SPA, LIT UV Technologies, Severn Trent Services, Evoqua Water Technologies, Advanced UV Inc., Alfa Laval, Aquafine Corporation, ERMA FIRST ESK Engineering SA, Atlantium Technologies Ltd., Clean Water Technology, and Trojan Technologies Group. Companies in the Global UV Disinfection System Market are strengthening their foothold by investing in innovative UV-C LED technology to enhance efficiency and extend lifespan. They are expanding service networks and offering turnkey solutions to improve client adoption and reliability. Strategic partnerships with municipalities and industrial clients help ensure long-term contracts and recurring revenue streams. Additionally, firms are focusing on research and development to introduce energy-efficient, low-maintenance systems that meet evolving regulatory standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Flow Rate

- 2.2.4 Technology

- 2.2.5 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent Government Regulations on Water Quality

- 3.2.1.2 Growing Demand for Chemical-Free Disinfection

- 3.2.1.3 Rising Investments in Water/Wastewater Infrastructure

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial Capital Investment (CapEx)

- 3.2.2.2 Technical Limitations in UV-C LED Efficiency

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of UV in Air & Surface Disinfection

- 3.2.3.2 Advancements in Mercury-Free UV-C LED Technology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By Region

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Components, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 UV lamps

- 5.3 Ballasts/drivers

- 5.4 Quartz sleeves

- 5.5 Control systems

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Flow Rate, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Small (1,000 m3/day)

- 6.3 Medium (1,000 - 50,000 m3/day)

- 6.4 Large (>50,000 m3/day)

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Low-pressure UV

- 7.3 Medium pressure UV

- 7.4 Pulsed UV

- 7.5 UV LED

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Municipal water & wastewater authorities

- 8.3 Industrial manufacturers

- 8.4 Commercial facilities (e.g., Hotels, Malls)

- 8.5 Residential/point-of-use

Chapter 9 Market Estimates & Forecast, By Distribution Channel, (USD Million) (Thousand units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Advanced UV Inc.

- 11.2 Alfa Laval

- 11.3 Atlantic Ultraviolet Corporation

- 11.4 Atlantium Technologies Ltd.

- 11.5 Aquafine Corporation

- 11.6 Clean Water Technology

- 11.7 Evoqua Water Technologies

- 11.8 ERMA FIRST ESK Engineering SA

- 11.9 Heraeus Noblelight

- 11.10 Industrie De Nora SPA

- 11.11 LIT UV Technologies

- 11.12 Pentair (Aquionics)

- 11.13 Severn Trent Services

- 11.14 Trojan Technologies Group

- 11.15 Xylem Inc.