|

市场调查报告书

商品编码

1892786

开源情报(OSINT)市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Open-Source Intelligence (OSINT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球开源情报 (OSINT) 市场价值为 127 亿美元,预计到 2035 年将以 26.7% 的复合年增长率增长至 1336 亿美元。

网路威胁(包括勒索软体、诈欺和资料外洩)的日益频繁和复杂化,正促使各组织采用开源情报(OSINT)解决方案,以实现即时威胁侦测和风险缓解。 2024年企业网路遭受的网路攻击激增,促使企业广泛采用开源情报平台,以增强威胁情报并提供预警系统。企业正在利用来自社群媒体、部落格、新闻入口网站、物联网设备和网路论坛的日益增长的公开资料,以获取可操作的洞察。人工智慧、机器学习、自然语言处理和巨量资料分析等领域的技术进步,实现了资料收集的自动化,提高了预测性威胁侦测能力,并增强了分析能力。一些开源情报平台现在整合了由人工智慧驱动的商业智慧解决方案,使商业组织和政府机构能够快速存取准确的资料、情报和可操作的洞察,从而支援决策和安全营运。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 127亿美元 |

| 预测值 | 1336亿美元 |

| 复合年增长率 | 26.7% |

解决方案业务部门占据62%的市场份额,预计2025年将创造79.2亿美元的收入。该板块涵盖软体平台、资料收集工具、分析应用以及完全整合的智慧套件,旨在支援端到端的开源情报(OSINT)行动,包括资料收集、分析、监控和分发。云端架构和行动导向的API优先整合等创新预计将持续推动成长。

到2025年,云端部署市场占有率将达到67%,预计到2035年将以27.3%的复合年增长率成长。基于云端的开源情报(OSINT)平台提供订阅定价、弹性扩展、快速部署、持续更新和多租户高效性等优势。这些优势使全球各地的分散式团队无需维护本地基础设施即可存取先进的情报工具。采用公共云端还使中型组织能够实施开源情报解决方案,促进协作,并在全面的安全营运中与其他云端服务无缝整合。

预计到2025年,美国开源情报(OSINT)市场规模将达到30.6亿美元。联邦政府的支出、雄厚的国防预算、金融和科技业的大型企业以及完善的供应商生态系统,共同支撑着该市场的成熟。联邦机构和商业安全团队高度依赖可扩展的威胁情报平台、连结分析和暗网监控来增强安全态势和提升营运效率。

目录

第一章:方法论

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 网路威胁与安全问题日益加剧

- 数位足迹和资料可用性不断增长

- 监理合规与风险管理

- 技术进步

- 产业陷阱与挑战

- 资料隐私和监管限制

- 复杂性及对专业人才的需求

- 市场机会

- 新兴市场和中小企业

- 拓展至非传统领域

- 高级分析服务

- 与安全生态系统集成

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- CISA(网路安全与基础设施安全局)

- 个人资讯保护与电子文件法(PIPEDA)

- 欧洲

- 联邦资料保护法 (BDSG)

- 隐私代码(Codice in materia di protezione dei dati individuali)

- 国家网路安全局(ANSSI)指令

- 2018年资料保护法

- 亚太地区

- 个人资讯保护法 (PIPL)

- 2023年数位个人资料保护法

- PIPA(个人资讯保护法)

- 1979年电信(截取与存取)法

- 拉丁美洲

- LGPD(Lei Geral de Protecao de Dados)

- 国家个人资料保护局法规

- 联邦法律关于保护私人持有的个人数据

- 中东和非洲

- 个人资料保护法 (PDPL)

- 反网路犯罪法

- 电子通讯和交易法

- 北美洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 定价分析

- 副产品

- 按地区

- 成本細項分析

- 供应商成本结构

- 成本构成要素的实施

- 持续营运成本

- 间接客户成本

- 专利分析

- 案例研究

- 政府网路安全机构

- 全球银行诈欺侦测与合规监控

- 零售及消费品牌声誉及仿冒品追踪

- 电信公司地缘政治与基础设施情报

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来展望与机会

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2022-2035年

- 解决方案/平台

- 开源情报分析平台

- 社群媒体情报工具

- 地理空间工具

- 文字探勘引擎

- 服务

- 专业服务

- 咨询

- 部署与集成

- 支援与维护

- 託管服务

- 专业服务

第六章:市场估算与预测:依证券类型划分,2022-2035年

- 人类智能

- 内容智能

- 巨量资料安全

- 人工智慧安全

- 数据分析

- 暗网分析

- 链路/网路分析

第七章:市场估算与预测:依部署模式划分,2022-2035年

- 云

- 现场

第八章:市场估算与预测:依应用领域划分,2022-2035年

- 国家安全

- 军事与国防

- 私部门

- 公部门

- 其他的

第九章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球公司

- Accenture

- Babel Street

- Cellebrite

- IBM

- Maltego Technologies

- Microsoft

- NICE

- Palantir Technologies

- Recorded Future

- SAIL Labs

- Thales

- 区域玩家

- BAE Systems Applied Intelligence

- Ciqurix Intelligence

- CybelAngel

- DarkOwl

- Digimind (Onclusive)

- OpenText

- Social Links

- ThreatQuotient

- Verint Systems

- ZeroFox

- 新兴玩家

- Dataminr

- Fivecast

- Hetz

- Hypersight

- Kharon

- Skopenow

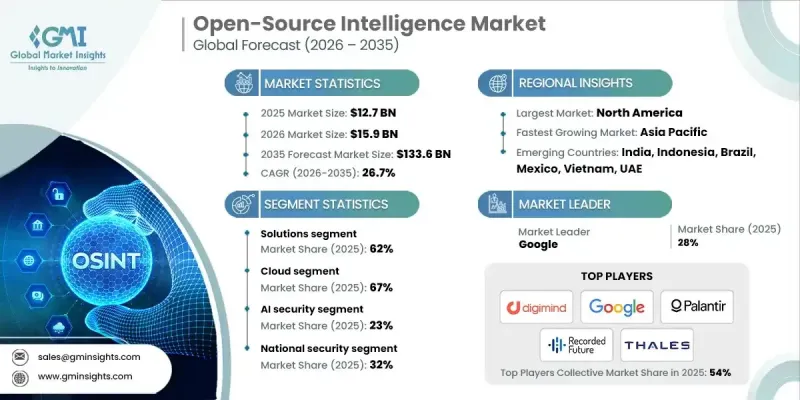

The Global Open-Source Intelligence (OSINT) Market was valued at USD 12.7 billion in 2025 and is estimated to grow at a CAGR of 26.7% to reach USD 133.6 billion by 2035.

The rising frequency and complexity of cyber threats, including ransomware, fraud, and data breaches, are driving organizations to adopt OSINT solutions for real-time threat detection and risk mitigation. The spike in cyber-attacks across enterprise networks in 2024 prompted significant adoption of OSINT platforms to enhance threat intelligence and provide early warning systems. Businesses are leveraging the increasing volume of publicly available data from social media, blogs, news portals, IoT devices, and web forums to gain actionable insights. Technological advancements in artificial intelligence, machine learning, natural language processing, and big data analytics have automated data collection, improved predictive threat detection, and strengthened analysis. Some OSINT platforms now integrate AI-driven business intelligence solutions, allowing both commercial organizations and government agencies to rapidly access accurate data, intelligence, and actionable insights for decision-making and security operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.7 Billion |

| Forecast Value | $133.6 Billion |

| CAGR | 26.7% |

The solutions segment held a 62% share, generating USD 7.92 billion in 2025. This segment includes software platforms, data collection tools, analytical applications, and fully integrated intelligence suites that facilitate end-to-end OSINT operations, covering data acquisition, analysis, monitoring, and dissemination. Innovations such as cloud-based architectures and API-first integration for mobile access are expected to continue fueling growth.

The cloud deployment segment accounted for a 67% share in 2025 and is projected to grow at a CAGR of 27.3% through 2035. Cloud-based OSINT platforms offer subscription pricing, elastic scalability, rapid deployment, continuous updates, and multi-tenant efficiency. These advantages allow distributed teams worldwide to access advanced intelligence tools without maintaining on-premises infrastructure. Public cloud adoption also enables mid-sized organizations to implement OSINT solutions, promote collaboration, and integrate seamlessly with other cloud services within comprehensive security operations.

U.S. Open-Source Intelligence (OSINT) Market reached USD 3.06 billion in 2025. The market's maturity is supported by federal government spending, robust defense budgets, large corporations in the finance and technology sectors, and a well-established vendor ecosystem. Federal agencies and commercial security teams heavily rely on scalable threat intelligence platforms, link analysis, and dark web monitoring to strengthen security posture and operational efficiency.

Key players in the Global Open-Source Intelligence (OSINT) Market include Google, Palantir Technologies, Digimind (Onclusive), Cellebrite, Babelstreet, Maltego Technologies, Recorded Future, Thales, NICE, Sail Labs (Hensoldt), and CybelAngel. Companies in the Global Open-Source Intelligence (OSINT) Market are strengthening their foothold by investing in AI and ML-driven analytics, cloud-enabled deployment, and mobile-friendly solutions. Strategic partnerships with government agencies and enterprises help expand adoption and credibility. Firms are also focusing on API-first integrations to ensure interoperability with existing security infrastructures, while enhancing platform scalability and user experience. Regular updates, threat intelligence enrichment, and tailored industry solutions further differentiate offerings, allowing vendors to capture emerging opportunities in both commercial and public sector segments while maintaining long-term market leadership.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment mode

- 2.2.4 Security

- 2.2.5 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cyber threats & security concerns

- 3.2.1.2 Growing digital footprint & data availability

- 3.2.1.3 Regulatory compliance & risk management

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy & regulatory restrictions

- 3.2.2.2 Complexity & skilled resource requirement

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets & SMEs

- 3.2.3.2 Expansion into non-traditional sectors

- 3.2.3.3 Advanced analytics services

- 3.2.3.4 Integration with security ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 CISA (Cybersecurity & Infrastructure Security Agency)

- 3.4.1.2 Personal Information Protection and Electronic Documents Act (PIPEDA)

- 3.4.2 Europe

- 3.4.2.1 BDSG (Federal Data Protection Act)

- 3.4.2.2 Privacy Code (Codice in materia di protezione dei dati personali)

- 3.4.2.3 National Cybersecurity Agency (ANSSI) directives

- 3.4.2.4 Data Protection Act 2018

- 3.4.3 Asia Pacific

- 3.4.3.1 PIPL (Personal Information Protection Law)

- 3.4.3.2 Digital Personal Data Protection Act 2023

- 3.4.3.3 PIPA (Personal Information Protection Act)

- 3.4.3.4 Telecommunications (Interception and Access) Act 1979

- 3.4.4 Latin America

- 3.4.4.1 LGPD (Lei Geral de Protecao de Dados)

- 3.4.4.2 National Directorate for Personal Data Protection regulations

- 3.4.4.3 Federal Law on the Protection of Personal Data Held by Private Parties

- 3.4.5 Middle East & Africa

- 3.4.5.1 PDPL (Personal Data Protection Law)

- 3.4.5.2 Anti-Cyber Crime Law

- 3.4.5.3 Electronic Communications and Transactions Act

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 By product

- 3.8.2 By region

- 3.9 Cost breakdown analysis

- 3.9.1 Vendor cost structure

- 3.9.2 Implementation of cost components

- 3.9.3 Ongoing operational costs

- 3.9.4 Indirect customer costs

- 3.10 Patent analysis

- 3.11 Case studies

- 3.11.1 Government cyber agency

- 3.11.2 Global bank fraud detection & compliance monitoring

- 3.11.3 Retail & consumer brand reputation and counterfeit product tracking

- 3.11.4 Telecom company geopolitical & infrastructure intelligence

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Solutions/Platforms

- 5.2.1 OSINT analytics platforms

- 5.2.2 Social media intelligence tools

- 5.2.3 Geospatial tools

- 5.2.4 Text-mining engines

- 5.3 Services

- 5.3.1 Professional services

- 5.3.1.1 Consulting

- 5.3.1.2 Deployment & integration

- 5.3.1.3 Support & maintenance

- 5.3.2 Managed services

- 5.3.1 Professional services

Chapter 6 Market Estimates & Forecast, By Security, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Human intelligence

- 6.3 Content intelligence

- 6.4 Big data security

- 6.5 AI security

- 6.6 Data analytics

- 6.7 Dark web analysis

- 6.8 Link/network analysis

Chapter 7 Market Estimates & Forecast, By Deployment mode, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 National security

- 8.3 Military & defense

- 8.4 Private sector

- 8.5 Public sector

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Accenture

- 10.1.2 Babel Street

- 10.1.3 Cellebrite

- 10.1.4 Google

- 10.1.5 IBM

- 10.1.6 Maltego Technologies

- 10.1.7 Microsoft

- 10.1.8 NICE

- 10.1.9 Palantir Technologies

- 10.1.10 Recorded Future

- 10.1.11 SAIL Labs

- 10.1.12 Thales

- 10.2 Regional players

- 10.2.1 BAE Systems Applied Intelligence

- 10.2.2 Ciqurix Intelligence

- 10.2.3 CybelAngel

- 10.2.4 DarkOwl

- 10.2.5 Digimind (Onclusive)

- 10.2.6 OpenText

- 10.2.7 Social Links

- 10.2.8 ThreatQuotient

- 10.2.9 Verint Systems

- 10.2.10 ZeroFox

- 10.3 Emerging players

- 10.3.1 Dataminr

- 10.3.2 Fivecast

- 10.3.3 Hetz

- 10.3.4 Hypersight

- 10.3.5 Kharon

- 10.3.6 Skopenow

2026年全球开放原始码情报市场报告

2026年全球开放原始码情报市场报告 开放原始码情报市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

开放原始码情报市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 全球开放原始码情报市场规模、份额、趋势和成长分析报告(2026-2034)

全球开放原始码情报市场规模、份额、趋势和成长分析报告(2026-2034) 开放原始码情报市场规模、份额、趋势及预测(按资讯来源类型、方法论、最终用户和地区划分),2026-2034 年

开放原始码情报市场规模、份额、趋势及预测(按资讯来源类型、方法论、最终用户和地区划分),2026-2034 年 开放原始码情报市场-全球产业规模、份额、趋势、机会及预测(依技术、资讯来源、部署类型、组织规模、地区及竞争格局划分,2021-2031年)

开放原始码情报市场-全球产业规模、份额、趋势、机会及预测(依技术、资讯来源、部署类型、组织规模、地区及竞争格局划分,2021-2031年) 开放原始码情报市场规模、份额和成长分析(依方法论、资讯来源、部署类型、组织规模、应用和地区划分)-2026-2033年产业预测

开放原始码情报市场规模、份额和成长分析(依方法论、资讯来源、部署类型、组织规模、应用和地区划分)-2026-2033年产业预测 开放原始码情报(OSINT):全球市场份额和排名、总收入和需求预测(2025-2031 年)

开放原始码情报(OSINT):全球市场份额和排名、总收入和需求预测(2025-2031 年)