|

市场调查报告书

商品编码

1892795

医疗器材分销服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Medical Device Distribution Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

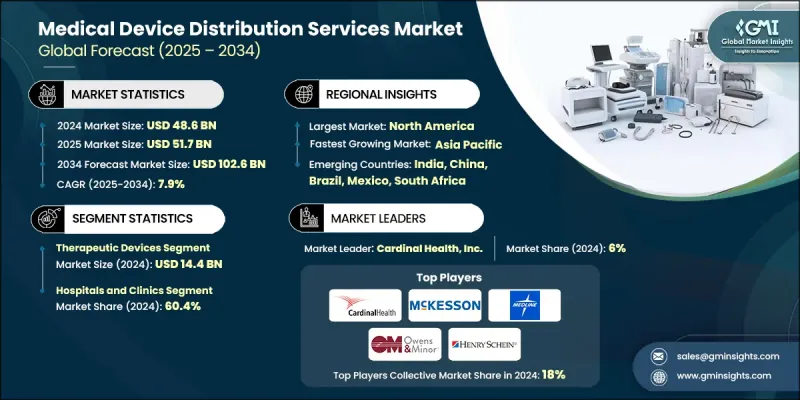

2024 年全球医疗器材分销服务市场价值为 486 亿美元,预计到 2034 年将以 7.9% 的复合年增长率增长至 1026 亿美元。

慢性病盛行率上升、家庭医疗保健和远端监测解决方案的快速普及以及对数位化供应链能力的大量投资是推动这一增长的主要因素。经销商日益成为医疗保健系统的策略合作伙伴,不仅提供物流服务,还提供安装、校准、培训、冷链管理和UDI可追溯性等加值服务,从而加速从商品运输到整合式临床供应解决方案的转变。同时,医院庞大的采购量和集团采购组织(GPO)的运作模式也增加了对先进分销服务的需求,这些服务能够减少缺货、缩短交货时间并确保跨多个司法管辖区的合规性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 486亿美元 |

| 预测值 | 1026亿美元 |

| 复合年增长率 | 7.9% |

依产品类型划分,治疗器材领域在2024年以144亿美元的市场规模领跑,反映出市场对输液帮浦、呼吸器材、心血管支架、人工植入物、透析系统和其他关键治疗技术的强劲需求。治疗器械通常需要特殊处理、冷炼或条件敏感型物流以及售后支援(安装、维修、员工培训),这提高了分销商的利润率,并巩固了与医院和诊所的长期合作关係。

从终端用户角度来看,医院和诊所预计在2024年将占据60.4%的市场份额,这主要归因于其广泛的设备需求、集中采购流程以及为应对急诊和外科手术而需要维持较高的内部库存。医院倾向于选择包含物流、安装和售后支援的捆绑式服务,这凸显了能够确保产品可追溯性、快速回应维修和合规性报告的分销合作伙伴的战略重要性。

2024年,北美医疗器材分销服务市占率达到39.2%,反映了该地区成熟的医疗保健基础设施、高手术量以及对数位化物流技术(物联网、人工智慧、区块链等可追溯性技术)的早期应用。美国市场动态,包括庞大的医院网路、集中式集团采购组织(GPO)合约以及完善的家庭医疗保健报销体系,都为分销商提供了更高的利润空间,并促使其投资于先进的冷炼和自动化补货系统。此外,北美在供应链韧性、分销中心技术现代化以及诸如UDI等监管框架方面的大量公共和私人资金投入,进一步巩固了其领先地位,这些监管框架激励着可追溯、品质保证的分销模式。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 慢性病盛行率不断上升

- 研究投资激增和医疗器材审批数量成长

- 家庭医疗保健和远端监测的需求不断增长

- 医疗器材技术的进步

- 产业陷阱与挑战

- 需要高额的初始资本支出

- 严格的监理合规性

- 市场机会

- 线上分销服务和数位订购系统的成长

- 加强公私合作以强化供应链

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 技术进步

- 当前技术趋势

- 新兴技术

- 供应链分析

- 报销方案

- 2024年定价分析

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 诊断设备

- 治疗设备

- 病患监护设备

- 家用医疗保健设备

- 其他产品类型

第六章:市场估算与预测:依最终用途划分,2021-2034年

- 医院和诊所

- 诊断中心

- 门诊手术中心(ASC)

- 长期照护机构

- 家庭护理机构

第七章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第八章:公司简介

- Alfresa Holdings Corporation

- Avantor, Inc.

- Bunzl plc

- CAN-med Healthcare

- Cardinal Health, Inc.

- Henry Schein, Inc.

- KEBOMED Europe AG

- McKesson Corporation

- Meditek Systems Pvt. Ltd.

- Medline Industries, LP.

- Owens & Minor, Inc.

- 帕特森公司

- Soquelec Ltd.

- Southmedic Inc.

- The Stevens Company Limited

The Global Medical Device Distribution Services Market was valued at USD 48.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 102.6 billion by 2034.

The expansion is driven by rising chronic disease prevalence, rapid adoption of home-healthcare and remote monitoring solutions, and significant investments in digital supply-chain capabilities. Distributors are increasingly positioned as strategic partners to healthcare systems, providing not just logistics but value-added services such as installation, calibration, training, cold-chain management, and UDI traceability, which is accelerating the shift from commodity shipping to integrated clinical supply solutions. Simultaneously, hospitals' large procurement volumes and Group Purchasing Organization (GPO) dynamics are increasing demand for sophisticated distribution services that reduce stockouts, shorten lead times, and ensure regulatory compliance across multiple jurisdictions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48.6 Billion |

| Forecast Value | $102.6 Billion |

| CAGR | 7.9% |

By product type, the therapeutic devices segment led the market in 2024 with USD 14.4 billion, reflecting strong demand for infusion pumps, respiratory devices, cardiovascular stents, prosthetic implants, dialysis systems, and other treatment-critical technologies. Therapeutic devices typically require specialized handling, cold-chain or condition-sensitive logistics, and after-sales support (installation, servicing, staff training), which amplifies distributor margins and cements long-term partnerships with hospitals and clinics.

On an end-use basis, the hospitals and clinics segment held 60.4% share in 2024, owing to their broad device requirements, centralized procurement processes, and need to maintain high in-house inventories for emergency and surgical care. Hospitals' preference for bundled service offerings combining logistics, installation, and post-sale support heightens the strategic importance of distribution partners who can guarantee traceability, rapid response repair, and compliance reporting.

North America Medical Device Distribution Services Market held 39.2% share in 2024, reflecting the region's mature healthcare infrastructure, high procedural volumes, and early adoption of digital logistics technologies (IoT, AI, blockchain for traceability). The U.S. market dynamics, including large hospital networks, centralized GPO contracting, and strong home-healthcare reimbursement systems, support higher distributor margins and investment in advanced cold-chain and automated replenishment systems. North America's leadership is further reinforced by substantial private and public funding for supply-chain resilience, technology modernization in distribution centers, and regulatory frameworks such as UDI that incentivize traceable, quality-assured distribution models.

Key players shaping the Global Medical Device Distribution Services Market include Cardinal Health, Inc.; McKesson Corporation; Medline Inc.; Owens & Minor, Inc.; Henry Schein, Inc.; Patterson Companies, Inc.; Bunzl plc; Avantor, Inc.; Alfresa Holdings Corporation; CAN-med Healthcare; KEBOMED Europe AG; Meditek Systems Pvt. Ltd.; Soquelec Ltd.; Southmedic Inc.; and The Stevens Company Limited. These companies are competing on breadth of coverage, cold-chain and compliance capabilities, digital ordering platforms, and value-added clinical services. Market leaders are investing in smart warehouses, temperature-validated storage, last-mile home care delivery capabilities, and partnerships with OEMs and telehealth providers to capture higher margin service revenues and lock in long-term procurement agreements. Companies in the medical device distribution services market are strengthening footprints through vertical integration, digital platform investments, and strategic partnerships with hospitals, GPOs, and device OEMs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic diseases

- 3.2.1.2 Surge in investments for research purpose and growth in medical device approvals

- 3.2.1.3 Rising demand for home healthcare and remote monitoring

- 3.2.1.4 Advancements in medical device technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Requirement for high initial capital expenditure

- 3.2.2.2 Presence of stringent regulatory compliance

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in online distribution services and digital ordering system

- 3.2.3.2 Increasing public private partnership to strengthen supply chain

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostic devices

- 5.3 Therapeutic devices

- 5.4 Patient monitoring devices

- 5.5 Home healthcare devices

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals and clinics

- 6.3 Diagnostic centers

- 6.4 Ambulatory surgical centers (ASCs)

- 6.5 Long-term care facilities

- 6.6 Homecare settings

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Alfresa Holdings Corporation

- 8.2 Avantor, Inc.

- 8.3 Bunzl plc

- 8.4 CAN-med Healthcare

- 8.5 Cardinal Health, Inc.

- 8.6 Henry Schein, Inc.

- 8.7 KEBOMED Europe AG

- 8.8 McKesson Corporation

- 8.9 Meditek Systems Pvt. Ltd.

- 8.10 Medline Industries, LP.

- 8.11 Owens & Minor, Inc.

- 8.12 Patterson Companies, Inc.

- 8.13 Soquelec Ltd.

- 8.14 Southmedic Inc.

- 8.15 The Stevens Company Limited