|

市场调查报告书

商品编码

1892808

眼科缝合线市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Ophthalmic Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

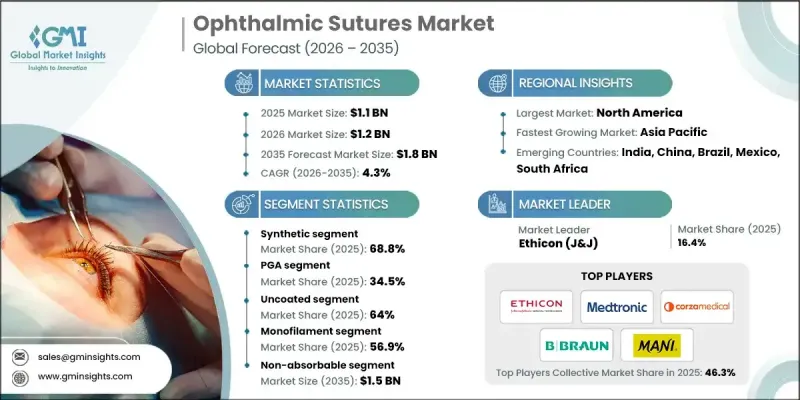

2025 年全球眼科缝合线市场价值为 11 亿美元,预计到 2035 年将以 4.3% 的复合年增长率增长至 18 亿美元。

眼科手术数量的增加、人口老化、技术创新、眼部疾病盛行率上升以及优质医疗保健服务的普及,共同推动了市场扩张。眼科缝合线为医院、专科眼科诊所和门诊手术中心提供至关重要的手术解决方案,可改善患者预后,实现精准的伤口管理,并提高白内障、角膜、青光眼和视网膜手术的手术效率。这些缝合线,包括先进的可吸收和不可吸收缝合线,经过精心设计,具有优异的操作性能、最小的组织损伤和可靠的术后癒合,使眼科医生能够更精确、更安全地进行精细手术。显微外科技术的进步以及门诊和日间眼科手术的日益普及,增加了对能够减少发炎、加速癒合并提供可预测恢復效果的缝合线的需求。新兴经济体医疗基础设施的扩建和支出的成长也提高了患者接受矫正性眼科手术的机会,从而支撑了市场的持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 11亿美元 |

| 预测值 | 18亿美元 |

| 复合年增长率 | 4.3% |

到2025年,合成缝合线市占率预计将达到68.8%,这主要得益于其高拉伸强度、可预测的吸收性和广泛的临床应用。合成缝合线由聚乳酸-羟基乙酸共聚物、聚乙醇酸和聚二氧杂环己酮等材料製成,具有组织反应性低、感染或发炎风险小等优点,因此非常适合用于精细的眼科手术。

由于其可生物降解性和优异的抗拉强度,PGA(聚乙醇酸)缝合线预计在2025年将占据34.5%的市场份额,价值达6.07亿美元。 PGA缝合线可在体内逐渐降解,无需取出,从而减轻患者不适,减少復诊次数,尤其有利于儿科和老年患者。

2025年,北美眼科缝合线市占率预计将达到38.1%,这主要得益于先进的医疗基础设施、高昂的医疗支出以及眼部疾病盛行率的不断上升。该地区拥有庞大的医院、门诊手术中心和专科眼科诊所网络,进行大量的白内障、青光眼和视网膜手术,从而确保了对眼科缝合线的持续需求。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 眼疾发生率不断上升

- 技术进步

- 糖尿病盛行率上升导致眼部疾病

- 有利的政府倡议

- 微创手术的需求和偏好激增

- 产业陷阱与挑战

- 眼科手术后併发症

- 缺乏技术娴熟的眼科医生

- 市场机会

- 特种和高端缝合线的使用率不断提高

- 随着眼科医疗基础设施的改善,新兴市场将迎来扩张。

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 技术进步

- 当前技术趋势

- 精密设计的缝合针组合

- 预装式即用缝合线包

- 微创显微外科缝合技术

- 新兴技术

- 生物可吸收涂层缝合线

- 先进聚合物和复合材料

- 智慧手术工具与机器人辅助缝合

- 当前技术趋势

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

- 数位手术规划与人工智慧辅助显微手术的融合

- 生物工程及药物洗脱缝合线的研发

- 随着眼科基础设施的不断完善,新兴市场将迎来扩张。

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 竞争定位矩阵

- 主要市场参与者的竞争分析

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依类型划分,2022-2035年

- 自然的

- 合成的

第六章:市场估算与预测:依材料划分,2022-2035年

- PGA

- 尼龙

- 丝绸

- 聚丙烯

- 其他材料

第七章:市场估算与预测:依涂料产业划分,2022-2035年

- 涂层

- 未涂层

第八章:市场估算与预测:依材料结构划分,2022-2035年

- 单丝

- 多股/编织

第九章:市场估计与预测:依吸收量划分,2022-2035年

- 可吸收

- 不可吸收

第十章:市场估计与预测:依应用领域划分,2022-2035年

- 白内障手术

- 角膜移植手术

- 青光眼手术

- 玻璃体切除术

- 眼部整形手术

- 其他应用

第十一章:市场估计与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 其他最终用途

第十二章:市场估算与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十三章:公司简介

- Alcon

- Assut Medical

- Aurolab

- Accutome

- B Braun

- Corza Medical

- DemeTECH

- Ethicon

- FCI Ophthalmics

- Geuder AG

- Mani

- Medtronic

- Teleflex Incorporated

- Unilene

The Global Ophthalmic Sutures Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 1.8 billion by 2035.

Market expansion is driven by the rising number of ophthalmic surgeries, an aging population, technological innovations, and increased prevalence of eye disorders, alongside broader access to quality healthcare. Ophthalmic sutures provide crucial surgical solutions to hospitals, specialty eye clinics, and ambulatory surgical centers, enhancing patient outcomes, precise wound management, and surgical efficiency in cataract, corneal, glaucoma, and retinal procedures. These sutures, including advanced absorbable and non-absorbable options, are engineered for superior handling, minimal tissue trauma, and reliable postoperative healing, enabling ophthalmologists to perform delicate surgeries with greater precision and safety. Advancements in microsurgical techniques and the growing trend toward outpatient and ambulatory ophthalmic procedures have increased demand for sutures that reduce inflammation, accelerate healing, and provide predictable recovery outcomes. Expanding healthcare infrastructure and rising expenditure in emerging economies are also improving patient access to corrective eye surgeries, supporting consistent market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $1.8 Billion |

| CAGR | 4.3% |

The synthetic segment held a 68.8% share in 2025, driven by high tensile strength, predictable absorption, and widespread clinical adoption. Synthetic sutures, composed of materials like polyglactin, polyglycolic acid, and polydioxanone, offer reduced tissue reactivity and minimal risk of infection or inflammation, making them highly suitable for delicate eye surgeries.

The PGA segment held a 34.5% share in 2025, valued at USD 607 million, due to its biodegradable properties and excellent tensile strength. PGA sutures degrade gradually in the body, eliminating the need for removal, reducing patient discomfort, and minimizing follow-up visits, particularly benefiting pediatric and geriatric patients.

North America Ophthalmic Sutures Market held a 38.1% share in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and growing prevalence of eye disorders. The region's extensive network of hospitals, ambulatory surgical centers, and specialty eye clinics performing a high volume of cataract, glaucoma, and retinal procedures ensures sustained demand for ophthalmic sutures.

Key players in the Global Ophthalmic Sutures Market include Teleflex Incorporated, Assut Medical, Aurolab, Ethicon, Alcon, Corza Medical, Accutome, Mani, DemeTECH, FCI Ophthalmics, Geuder AG, Medtronic, B Braun, and Unilene. Companies in the Ophthalmic Sutures Market are strengthening their position through continuous product innovation, developing sutures with improved handling, biodegradability, and tensile strength. Strategic partnerships with hospitals, clinics, and distributors enable wider reach and faster adoption of new solutions. Expanding global footprints and entering emerging markets allow manufacturers to capture rising demand in underserved regions. Investment in R&D, clinical training programs, and after-sales support enhances brand loyalty, while regulatory compliance and quality certifications build trust among healthcare providers. Marketing initiatives, educational outreach, and digital engagement strategies further solidify their market presence and competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Material trends

- 2.2.4 Coating trends

- 2.2.5 Material structure trends

- 2.2.6 Absorption trends

- 2.2.7 Application trends

- 2.2.8 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of eye diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising prevalence of diabetes leading to ophthalmic disorders

- 3.2.1.4 Favorable government initiatives

- 3.2.1.5 Surging demand and preference for minimally invasive surgeries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Postoperative complications associated with ophthalmic procedures

- 3.2.2.2 Lack of skilled ophthalmologist

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of specialty and premium sutures

- 3.2.3.2 Expansion in emerging markets with improving eye care infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.1.1 Precision-engineered suture-needle combinations

- 3.5.1.2 Preloaded and ready-to-use suture kits

- 3.5.1.3 Minimally invasive microsurgical suturing techniques

- 3.5.2 Emerging technologies

- 3.5.2.1 Bio-absorbable and coated sutures

- 3.5.2.2 Advanced polymer and composite materials

- 3.5.2.3 Smart surgical tools and robotic-assisted suturing

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Integration of digital surgical planning and AI-assisted microsurgery

- 3.9.2 Development of bioengineered and drug-eluting sutures

- 3.9.3 Expansion in emerging markets with advancing ophthalmic infrastructure

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Natural

- 5.3 Synthetic

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 PGA

- 6.3 Nylon

- 6.4 Silk

- 6.5 Polypropylene

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Coating, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Coated

- 7.3 Uncoated

Chapter 8 Market Estimates and Forecast, By Material Structure, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Monofilament

- 8.3 Multifilament/Braided

Chapter 9 Market Estimates and Forecast, By Absorption, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Absorbable

- 9.3 Non-absorbable

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Cataract surgery

- 10.3 Corneal transplantation surgery

- 10.4 Glaucoma surgery

- 10.5 Vitrectomy

- 10.6 Oculoplastic surgery

- 10.7 Other applications

Chapter 11 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 Hospitals

- 11.3 Ambulatory surgical centers

- 11.4 Other End use

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Alcon

- 13.2 Assut Medical

- 13.3 Aurolab

- 13.4 Accutome

- 13.5 B Braun

- 13.6 Corza Medical

- 13.7 DemeTECH

- 13.8 Ethicon

- 13.9 FCI Ophthalmics

- 13.10 Geuder AG

- 13.11 Mani

- 13.12 Medtronic

- 13.13 Teleflex Incorporated

- 13.14 Unilene

2026年全球眼科缝合线市场报告

2026年全球眼科缝合线市场报告 眼科缝线市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、最终用户、地区和竞争格局划分,2021-2031年

眼科缝线市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、最终用户、地区和竞争格局划分,2021-2031年 一次性眼科手术刀市场:按材料、应用、最终用户和分销管道划分,全球预测(2026-2032年)

一次性眼科手术刀市场:按材料、应用、最终用户和分销管道划分,全球预测(2026-2032年) 一次性眼科手术产品市场(2025):2024年至2030年全球分析一次性手术器械市场(按器械类型、材料类型、应用、最终用户和分销管道)—2025-2030 年全球预测

一次性眼科手术产品市场(2025):2024年至2030年全球分析一次性手术器械市场(按器械类型、材料类型、应用、最终用户和分销管道)—2025-2030 年全球预测 全球眼科缝合线市场全球一次性眼科手术器械市场

全球眼科缝合线市场全球一次性眼科手术器械市场 全球一次性手术器材市场(按产品类型、应用、医疗环境和地区划分)- 预测至 2030 年

全球一次性手术器材市场(按产品类型、应用、医疗环境和地区划分)- 预测至 2030 年 一次性眼科手术设备市场规模、份额、成长分析(按产品、按应用、按最终用户、按地区)- 行业预测,2025-2032 年

一次性眼科手术设备市场规模、份额、成长分析(按产品、按应用、按最终用户、按地区)- 行业预测,2025-2032 年 全球眼科缝合线市场规模、份额、趋势分析报告:按类型、吸收能力、应用、最终用途、地区和细分市场预测(2025-2030)

全球眼科缝合线市场规模、份额、趋势分析报告:按类型、吸收能力、应用、最终用途、地区和细分市场预测(2025-2030)