|

市场调查报告书

商品编码

1892812

射钉枪市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Nail Guns Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

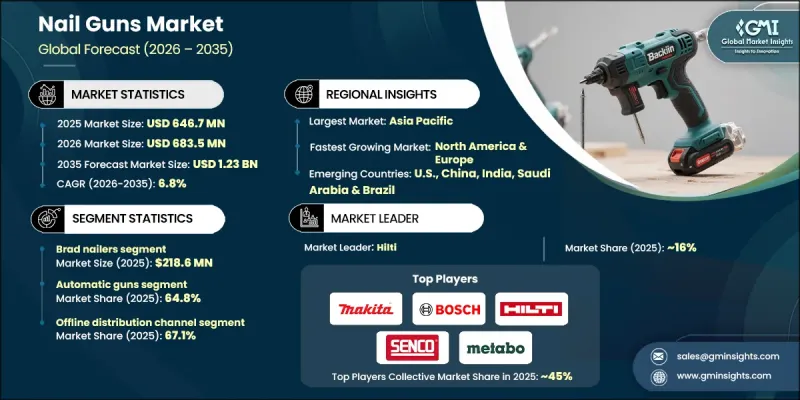

2025 年全球射钉枪市场价值为 6.467 亿美元,预计到 2035 年将以 6.8% 的复合年增长率增长至 12.3 亿美元。

随着建筑相关活动中对更快、更有效率的紧固解决方案的需求不断增长,市场持续保持成长势头。建筑活动的扩张、基础设施投资的增加以及在控制劳动力成本的同时提高生产力的需求,都推动了市场成长。由于射钉枪能够提供快速、均匀的紧固效果并减少体力消耗,因此越来越受到人们的青睐,优于手动紧固方法。承包商和专业用户正在采用这些工具来满足更紧迫的工期要求,并确保专案品质的一致性。同时,简化的产品设计以及使用者认知度的提高,也促进了非专业使用者群体的广泛采用。动力系统、人体工学和安全机制的持续进步也使市场受益,这些进步不断提升了工具的性能和可靠性。随着建筑实践的演变和效率的提升,射钉枪正从可选工具转变为必备设备,从而增强了其在专业和消费领域的长期需求。人们对个人改造计画的兴趣日益浓厚,也进一步推动了市场扩张。消费者越来越依赖电动紧固工具,以最少的努力获得干净、持久的紧固效果。製造商们正在积极回应,推出设计便利、安全、精准的用户友善产品,这有助于该领域保持稳定成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 6.467亿美元 |

| 预测值 | 12.3亿美元 |

| 复合年增长率 | 6.8% |

2025年,射钉枪市场规模达2.186亿美元,预计2026年至2035年将以7.3%的复合年增长率成长。此品类产品广泛应用于需要精准安装和表面保护的场合,较小的紧固件有助于维持材质的完整性。不断成长的装修活动和消费者对专业级饰面效果的追求,持续支撑着该品类的需求。

2025年,自动射钉枪市占率达到64.8%,预计到2035年将以6.9%的复合年增长率成长。这些工具支援连续作业,因此非常适合效率和劳动力最佳化至关重要的高产量环境。自动化、数位整合以及与智慧型系统的兼容性方面的进步,正在提升其对专业用户和工业用户的吸引力。

2025年美国射钉枪市场规模达1.367亿美元,预计2026年至2035年将以6.8%的复合年增长率成长。市场成长得益于持续的建筑活动、房地产开发的不断推进以及对提高生产效率工具的强劲需求。基础设施投资和持续的翻新改造活动进一步强化了对高效紧固解决方案的需求。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 建筑和基础设施的快速扩张

- 对效率和生产力的需求日益增长

- DIY与居家装潢趋势

- 技术进步

- 产业陷阱与挑战

- 初始成本高,维修需求高

- 无线机型的电池续航时间限制

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2022-2035年

- 框架钉枪

- 布拉德钉枪

- 钉枪

- 屋顶钉枪

- 地板钉枪

- 其他的

第六章:市场估算与预测:依电源类型划分,2022-2035年

- 气动钉枪

- 瓦斯/汽油动力钉枪

- 电动钉枪

- 电池供电

第七章:市场估算与预测:依营运模式划分,2022-2035年

- 手持枪械

- 自动枪

第八章:市场估算与预测:依价格划分,2022-2035年

- 低的

- 中等的

- 高的

第九章:市场估算与预测:依最终用途划分,2022-2035年

- 建筑与基础设施

- 家具及家居装修

- 汽车

- 包装

- 其他的

第十章:市场估价与预测:依配销通路划分,2022-2035年

- 在线的

- 电子商务平台

- 公司网站

- 离线

- 居家装修中心

- 专业工具商店

- 其他的

第十一章:市场估计与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙乌地阿拉伯

- 阿联酋

- 南非

第十二章:公司简介

- Bostitch

- DEWALT

- Freeman Tools

- Hilti Corporation

- Hitachi

- Makita Corporation

- Max Corporation

- Metabo

- Milwaukee Tool

- Paslode

- Ridgid

- Robert Bosch Tool Corporation

- Ryobi

- Senco

- Stanley Black & Decker

The Global Nail Guns Market was valued at USD 646.7 million in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 1.23 billion by 2035.

The market continues to gain momentum as demand rises for faster, more efficient fastening solutions across construction-related activities. Growth is supported by expanding building activity, rising investment in infrastructure, and the need to improve productivity while controlling labor expenses. Nail guns are increasingly preferred over manual fastening methods due to their ability to deliver speed, uniform results, and reduced physical effort. Contractors and professional users are adopting these tools to meet tighter schedules and ensure consistent quality across projects. At the same time, broader access to simplified product designs and better user awareness is supporting wider adoption among non-professional users. The market is also benefiting from ongoing advancements in power systems, ergonomics, and safety mechanisms, which continue to improve tool performance and reliability. As construction practices evolve and efficiency becomes a priority, nail guns are being positioned as essential equipment rather than optional tools, strengthening long-term demand across both professional and consumer segments. Growing interest in personal improvement projects is further supporting market expansion. Consumers increasingly rely on powered fastening tools to achieve clean, durable results with minimal effort. Manufacturers are responding by offering user-friendly models designed for convenience, safety, and precision, which is helping this segment sustain steady growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $646.7 Million |

| Forecast Value | $1.23 Billion |

| CAGR | 6.8% |

The brad nailers segment generated USD 218.6 million in 2025 and is forecast to grow at a CAGR of 7.3% from 2026 to 2035. This category is widely adopted for applications that require accuracy and surface protection, where smaller fasteners help preserve material integrity. Rising renovation activity and consumer preference for professional-quality finishes continue to support demand for this segment.

The automatic nail guns segment held 64.8% share in 2025 and is expected to grow at a CAGR of 6.9% through 2035. These tools support continuous operation, making them well-suited for high-output environments where efficiency and labor optimization are critical. Advancements in automation, digital integration, and compatibility with smart systems are enhancing their appeal among professional and industrial users.

US Nail Guns Market reached USD 136.7 million in 2025 and is projected to grow at a CAGR of 6.8% from 2026 to 2035. Market growth is supported by sustained construction activity, ongoing property development, and strong demand for productivity-enhancing tools. Investment in infrastructure and continued renovation activity further reinforces the need for efficient fastening solutions.

Major companies operating in the Global Nail Guns Market include DEWALT, Makita Corporation, Stanley Black & Decker, Milwaukee Tool, Bosch Tool Corporation, Hilti Corporation, Paslode, Ryobi, Metabo, Bostitch, Senco, Freeman Tools, Ridgid, Max Corporation, and Hitachi. Companies in the Nail Guns Market are strengthening their competitive position through continuous product innovation, expanded distribution channels, and targeted branding strategies. Manufacturers are investing in lightweight designs, improved power efficiency, and enhanced safety features to meet evolving user expectations. Strategic partnerships with retailers and professional networks are helping companies broaden market reach and improve customer access. Many players focus on differentiating their portfolios through specialized tools that address distinct user needs while maintaining durability and performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Power source

- 2.2.4 Operation

- 2.2.5 Price

- 2.2.6 End use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid expansion in construction & infrastructure

- 3.2.1.2 Rising demand for efficiency & productivity

- 3.2.1.3 DIY & home improvement trend

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial costs and maintenance requirements

- 3.2.2.2 Battery life limitations for cordless models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Framing nailers

- 5.3 Brad nailers

- 5.4 Pin nailers

- 5.5 Roofing nailers

- 5.6 Flooring nailers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Pneumatic nail guns

- 6.3 Combustion-powered / gas nail guns

- 6.4 Electric nail guns

- 6.5 Battery operated

Chapter 7 Market Estimates & Forecast, By Operation, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Handheld guns

- 7.3 Automatic guns

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Construction & infrastructure

- 9.3 Furniture & home improvement

- 9.4 Automotive

- 9.5 Packaging

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce platforms

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Home improvement centers

- 10.3.2 Specialty tool stores

- 10.3.3 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Bostitch

- 12.2 DEWALT

- 12.3 Freeman Tools

- 12.4 Hilti Corporation

- 12.5 Hitachi

- 12.6 Makita Corporation

- 12.7 Max Corporation

- 12.8 Metabo

- 12.9 Milwaukee Tool

- 12.10 Paslode

- 12.11 Ridgid

- 12.12 Robert Bosch Tool Corporation

- 12.13 Ryobi

- 12.14 Senco

- 12.15 Stanley Black & Decker

2026-2030年全球射钉枪市场

2026-2030年全球射钉枪市场 全球工业射钉枪市场规模、份额、趋势和成长分析报告(2026-2034年)

全球工业射钉枪市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球工业钉枪和订书机市场报告2026年全球气动角钉枪市场报告

2026年全球工业钉枪和订书机市场报告2026年全球气动角钉枪市场报告 螺帽扳手市场 - 全球产业规模、份额、趋势、机会、预测:按类型、分销管道、终端用户产业、地区和竞争格局划分,2021-2031年

螺帽扳手市场 - 全球产业规模、份额、趋势、机会、预测:按类型、分销管道、终端用户产业、地区和竞争格局划分,2021-2031年 锂离子电池供电式无线钉枪市场:按产品类型、电池容量、马达类型、应用、最终用户和分销管道划分-2026年至2032年全球预测

锂离子电池供电式无线钉枪市场:按产品类型、电池容量、马达类型、应用、最终用户和分销管道划分-2026年至2032年全球预测 射钉枪:全球市占率和排名、总销售量和需求预测(2025-2031年)

射钉枪:全球市占率和排名、总销售量和需求预测(2025-2031年) 电池式射钉枪市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)钉枪和订书机市场(按产品类型、电源、最终用户和销售管道)——全球预测,2025-2030 年

电池式射钉枪市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)钉枪和订书机市场(按产品类型、电源、最终用户和销售管道)——全球预测,2025-2030 年 全球工业钉枪和订书机市场

全球工业钉枪和订书机市场