|

市场调查报告书

商品编码

1892849

等离子切割机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Plasma Cutting Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

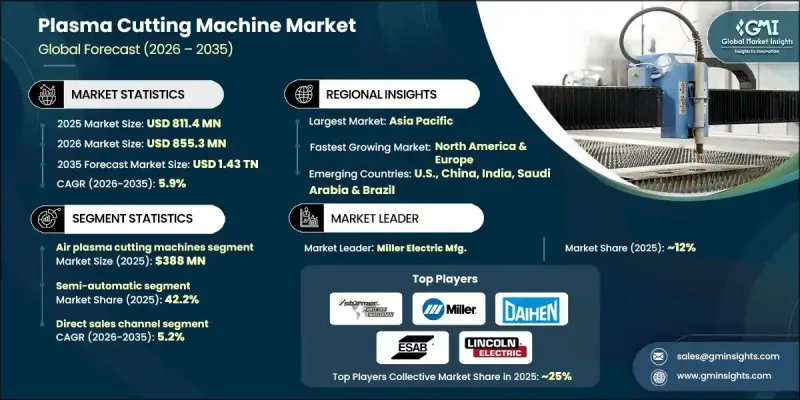

2025 年全球等离子切割机市值为 8.114 亿美元,预计到 2035 年将以 5.9% 的复合年增长率增长至 1.43 兆美元。

市场成长主要得益于数控技术和自动化在等离子切割系统中的日益普及。数控技术的整合使製造商能够持续生产高精度零件,从而减少人为误差并提高整体生产效率。自动化也支援工业4.0计画的实施,包括物联网监控、预测性维护以及製造系统间的无缝连接,进而提升生产效率。航太、汽车和重型工程等产业正是由于这些优势而高度依赖等离子切割机。此外,对节能高效、高精度等离子切割系统的需求不断增长,促使製造商致力于研发能够在保持卓越切割品质的同时,以更低功率位准运作的新型机器。这些技术能够减少切割过程中的热产生,最大限度地减少材料浪费,并防止热致变形,从而带来经济和环境效益。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 8.114亿美元 |

| 预测值 | 1.43兆美元 |

| 复合年增长率 | 5.9% |

2025年,空气等离子切割机市场规模达到3.88亿美元,预计2026年至2035年将以6.2%的复合年增长率成长。空气等离子系统使用压缩空气作为等离子气体,因此对中小企业而言经济高效且便利。这些机器切割低碳钢和其他常用金属的效率极高,由于其维护需求低、易于安装,与氧气或氢气等离子系统相比,在製造和轻工业应用中更受欢迎。

到 2025 年,直销通路的市占率将达到 64.4%,预计到 2035 年将以 5.2% 的复合年增长率成长。直接合作使製造商能够提供客製化的切割解决方案、技术支援和及时的备件交付,从而加强客户关係并提高营运效率。

2025年美国等离子切割机市场规模达1.389亿美元,预计2026年至2035年将以3.5%的复合年增长率成长。美国先进的工业基础、强大的製造业基础设施以及对自动化技术的早期应用,推动了对数控高精度等离子切割机的强劲需求。汽车、航太和重型机械等关键产业对精密切割的需求,进一步促进了市场成长。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 数控技术和自动化技术的广泛应用

- 节能型及高画质技术

- 快速城市化和基础设施项目

- 产业陷阱与挑战

- 来自替代技术的激烈竞争

- 高昂的资本成本和推广障碍

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过切割技术

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依切割技术划分,2022-2035年

- 空气等离子切割机

- 氧等离子切割机

- 氮气等离子切割机

- 氢等离子切割机

第六章:市场估算与预测:依营运模式划分,2022-2035年

- 自动的

- 半自动

- 手动的

第七章:市场估算与预测:依最终用途划分,2022-2035年

- 汽车

- 製造业

- 航太与国防

- 航运和海事

- 建筑和基础设施

- 其他的

第八章:市场估算与预测:依配销通路划分,2022-2035年

- 直销

- 间接销售

第九章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙乌地阿拉伯

- 阿联酋

- 南非

第十章:公司简介

- ACM Inc.

- Ador Welding Ltd.

- AJAN ELEKTRONIK

- C & G Systems

- ERMAKSAN

- ESAB Welding and Cutting Products

- DAIHEN Corporation

- Haco

- Hypertherm, Inc.

- Jinan Huaxia Machinery Equipment Co. Ltd.

- Kjellberg Finsterwalde Plasma und Maschinen GmbH

- Koike Aronson

- Komatsu cutting systems

- Lincoln Electric Holdings, Inc.

- Miller Electric Mfg

- Sturmer maschinen gmbh

- Victor Technologies

- Voortman Steel

The Global Plasma Cutting Machine Market was valued at USD 811.4 million in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 1.43 trillion by 2035.

The market is propelled by the rising adoption of CNC technologies and automation in plasma cutting systems. CNC integration allows manufacturers to produce high-precision components consistently, reducing human error and increasing overall production efficiency. Automation also supports the implementation of Industry 4.0 initiatives, including IoT-enabled monitoring, predictive maintenance, and seamless connectivity between manufacturing systems, enhancing productivity. Industries such as aerospace, automotive, and heavy engineering rely heavily on plasma cutting machines due to these capabilities. Additionally, the growing demand for energy-efficient and high-definition plasma systems is driving manufacturers to innovate machines that operate at lower power levels while maintaining superior cut quality. These technologies reduce heat generation during cutting, minimize material wastage, and prevent heat-induced distortion, offering both economic and environmental benefits.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $811.4 Million |

| Forecast Value | $1.43 Trillion |

| CAGR | 5.9% |

The air plasma cutting machines segment generated USD 388 million in 2025 and is expected to grow at a CAGR of 6.2% from 2026 to 2035. Air plasma systems use compressed air as the plasma gas, making them cost-effective and convenient for small and medium-sized enterprises. These machines are highly efficient for cutting mild steel and other widely used metals and are preferred in fabrication and light industrial applications due to their low maintenance requirements and ease of setup compared to oxygen or hydrogen plasma systems.

The direct sales channel held a 64.4% share in 2025 and is anticipated to grow at a CAGR of 5.2% through 2035. Direct engagement allows manufacturers to provide customized cutting solutions, technical support, and timely delivery of spare parts, strengthening customer relationships and improving operational efficiency.

U.S. Plasma Cutting Machine Market generated USD 138.9 million in 2025 and is expected to grow at a CAGR of 3.5% from 2026 to 2035. The country's advanced industrial base, strong manufacturing infrastructure, and early adoption of automation technologies drive high demand for CNC-controlled and high-definition plasma cutting machines. Key sectors such as automotive, aerospace, and heavy machinery require precision cutting, boosting market growth.

Major players operating in the Plasma Cutting Machine Market include Voortman Steel, Haco, ERMAKSAN, Lincoln Electric Holdings, Inc., Hypertherm, Inc., C & G Systems, Victor Technologies, Komatsu Cutting Systems, Miller Electric Mfg, DAIHEN Corporation, AJAN ELEKTRONIK, Sturmer Maschinen GmbH, Koike Aronson, Jinan Huaxia Machinery Equipment Co., Ltd., ACM Inc., Ador Welding Ltd., and ESAB Welding and Cutting Products. Companies in the Plasma Cutting Machine Market are employing multiple strategies to strengthen their market foothold. They are heavily investing in research and development to introduce high-definition, energy-efficient, and IoT-enabled plasma systems. Strategic collaborations with automotive, aerospace, and heavy engineering firms help expand customer reach and ensure product customization. Geographic expansion and the development of local service and support networks enhance accessibility for clients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cutting technology

- 2.2.3 Operation

- 2.2.4 End Use

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Widespread adoption of CNC and automation

- 3.2.1.2 Energy-efficient models & high-definition technology

- 3.2.1.3 Rapid urbanization and infrastructure projects

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Intense competition from alternative technologies

- 3.2.2.2 High capital costs & adoption barriers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Cutting technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Cutting Technology, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Air plasma cutting machines

- 5.3 Oxygen plasma cutting machines

- 5.4 Nitrogen plasma cutting machines

- 5.5 Hydrogen plasma cutting machine

Chapter 6 Market Estimates & Forecast, By Operation, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Automatic

- 6.3 Semi-automatic

- 6.4 Manual

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Manufacturing

- 7.4 Aerospace and defense

- 7.5 Shipping and maritime

- 7.6 Construction and infrastructure

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 ACM Inc.

- 10.2 Ador Welding Ltd.

- 10.3 AJAN ELEKTRONIK

- 10.4 C & G Systems

- 10.5 ERMAKSAN

- 10.6 ESAB Welding and Cutting Products

- 10.7 DAIHEN Corporation

- 10.8 Haco

- 10.9 Hypertherm, Inc.

- 10.10 Jinan Huaxia Machinery Equipment Co. Ltd.

- 10.11 Kjellberg Finsterwalde Plasma und Maschinen GmbH

- 10.12 Koike Aronson

- 10.13 Komatsu cutting systems

- 10.14 Lincoln Electric Holdings, Inc.

- 10.15 Miller Electric Mfg

- 10.16 Sturmer maschinen gmbh

- 10.17 Victor Technologies

- 10.18 Voortman Steel

全球等电浆切割机市场规模、份额、趋势和成长分析报告(2026-2034)全球等离子切割机市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034)

全球等电浆切割机市场规模、份额、趋势和成长分析报告(2026-2034)全球等离子切割机市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034) 采矿业等离子体处理市场规模、份额和趋势分析报告:按应用、材料、地区和细分市场预测(2025-2033 年)

采矿业等离子体处理市场规模、份额和趋势分析报告:按应用、材料、地区和细分市场预测(2025-2033 年) 2025-2029年全球等电浆切割机市场

2025-2029年全球等电浆切割机市场 等离子切割机市场,按技术、按自动化类型、按切割类型、按材料类型、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

等离子切割机市场,按技术、按自动化类型、按切割类型、按材料类型、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 等离子切割机市场(按产品类型、控制、配置、最终用户和地区划分)2025 年至 2033 年

等离子切割机市场(按产品类型、控制、配置、最终用户和地区划分)2025 年至 2033 年 全球等离子切割机市场:产业分析、规模、占有率、成长、趋势与预测(2024-2031 年)

全球等离子切割机市场:产业分析、规模、占有率、成长、趋势与预测(2024-2031 年)