|

市场调查报告书

商品编码

1892877

汽车火星塞市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Automotive Spark Plug Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

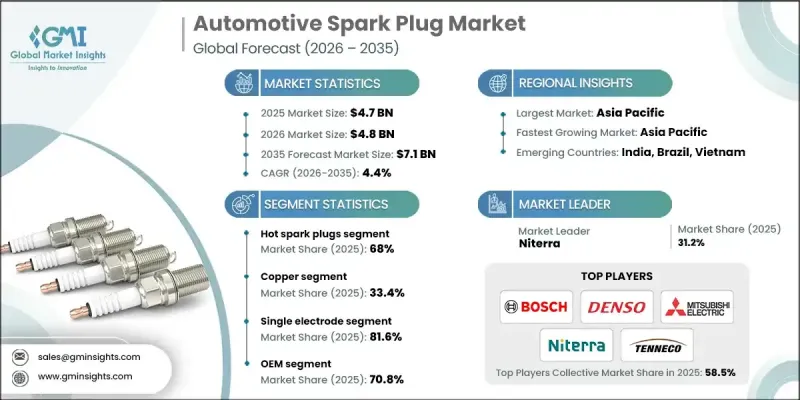

2025年全球汽车火星塞市场价值为47亿美元,预计2035年将以4.4%的复合年增长率成长至71亿美元。

全球新车产量稳定成长以及消费者对汽油动力车型的持续偏好支撑了市场成长。对更高燃油经济性的追求也推动了先进火星塞技术的普及,因为新型引擎架构旨在最大限度地提高效率。製造商正在其产品组合中扩大铱金和铂金等材料的使用,从而提升点火性能的耐用性和效率。现代燃烧系统目前可将燃油效率提高约10%,促使人们更广泛地使用优质火星塞组件。不断增长的城市出行趋势也增加了对采用火星点火系统的紧凑型引擎的需求。售后市场仍是市场的重要动力,尤其是在2024年车辆平均车龄超过12年的情况下,车辆的年度更换週期将会增加。高性能金属的持续改进也将继续延长火星塞的使用寿命并提高点火可靠性。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 47亿美元 |

| 预测值 | 71亿美元 |

| 复合年增长率 | 4.4% |

2025年,热型火星塞市占率达到68%,预计2026年至2035年间将以4.7%的复合年增长率成长。这类火星塞因其在宽广的温度范围内都能保持可靠的点火性能,仍然是传统汽油引擎的首选。其独特的设计有助于有效散热,从而减少在城市低速行驶(全球主要地区的大都市地区普遍存在)时产生的积碳。

到2025年,单电极火星塞市占率将达到81.6%。它们仍然是大众市场乘用车和两轮车的首选,这得益于2024年全球乘用车产量超过7,600万辆。大多数入门级和中级引擎仍依赖单电极系统,该系统运作稳定可靠,维护成本低廉。这使得它们在老旧车辆保有量大的地区,对售后市场尤其具有吸引力。

预计到2024年,中国汽车火星塞市占率将达到46.8%,2025年市场规模将达8.244亿美元。市场成长主要得益于汽车销售上升和城市快速扩张,持续推动乘用车产量超过2800万辆。这加速了主要城市和中小城镇的整车OEM)需求和换装週期。两轮交通仍然是交通运输领域的重要组成部分,预计到2024年,摩托车和踏板车的产量将达到约700万辆,其中大部分使用铜芯或铂金火星塞,因此对火星塞的持续更换需求强劲。

目录

第一章:方法论

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 汽油动力汽车的成长

- 转向高效发动机

- 售后市场活动日益增多

- 采用贵金属插头

- 产业陷阱与挑战

- 电动车渗透率不断提高

- 原料成本上涨

- 市场机会

- 全球售后市场的扩张

- 先进点火系统的开发

- 新兴市场两轮车需求成长

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 电极材料演变(从铜到钌)

- 细丝技术发展

- 多电极设计创新

- 预燃室火星塞技术

- 物联网与智慧诊断集成

- 雷射焊接製造技术的进步

- 热范围优化技术

- 下一代材料

- 新兴技术

- 当前技术趋势

- 价格趋势

- OEM与售后市场价格差异

- 区域价格差异

- 原料成本影响

- 进出口价格分析

- 未来价格走势

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 成本細項分析

- 专利与智慧财产权分析

- 电极材料的活性专利

- 专利地理分布

- 主要专利持有人

- 新兴技术专利(智慧插头)

- 专利到期时间表(2024-2034)

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 投资与融资分析

- 製造商研发投资趋势

- 替代燃料适应性投资

- 製造能力扩张

- 策略伙伴关係与合资企业

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依产品划分,2022-2035年

- 热火星塞

- 冷火星塞

第六章:市场估算与预测:依材料划分,2022-2035年

- 铜

- 铂

- 铱

- 其他的

第七章:市场估算与预测:依电极类型划分,2022-2035年

- 单电极

- 双电极

- 多电极

- 表面放电

第八章:市场估算与预测:依销售管道划分,2022-2035年

- OEM

- 售后市场

第九章:市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型

- 中型

- 重负

- 两轮车

- 摩托车

- 小型摩托车

第十章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 土耳其

第十一章:公司简介

- 全球参与者

- ACDelco

- Autolite

- Bosch

- DENSO

- MAHLE

- Mitsubishi Electric

- Niterra

- Tenneco

- Valeo

- 区域玩家

- BorgWarner

- Brisk Spark Plug Company

- E3 Spark Plugs

- Hella

- MAGNETI MARELLI PARTS & SERVICES

- MSD Performance

- Stitt Spark Plug Company

- Zhuzhou Torch Spark Plug

- 新兴参与者/颠覆者

- Iskra Spark Plugs

- Nanjing Leidian

- Prenco Progress & Engineering Corporation

- Pulstar

- SMP Automotive

- Weichai Power

The Global Automotive Spark Plug Market was valued at USD 4.7 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 7.1 billion by 2035.

Growth is supported by the steady rise in new vehicle production worldwide and continued consumer preference for gasoline-powered models. The shift toward better fuel economy is also driving higher adoption of advanced spark plug technologies, as newer engine architectures are built to maximize efficiency. Manufacturers are expanding the use of materials such as iridium and platinum throughout their portfolios, contributing to more durable and efficient ignition performance. Modern combustion systems now deliver around a 10 percent boost in fuel efficiency, which encourages broader use of premium spark plug components. Expanding urban mobility trends are creating more demand for compact engines that rely on spark-ignited systems. The aftermarket remains a strong contributor as well, particularly as the average age of vehicles surpassed 12 years in 2024, increasing annual replacement cycles. Ongoing improvements in high-performance metals also continue to enhance spark plug lifespan and ignition reliability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.7 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 4.4% |

The hot spark plugs segment held a 68% share in 2025, and this category is expected to expand at a CAGR of 4.7% between 2026 and 2035. These plugs remain favored for conventional gasoline engines because they maintain dependable ignition across a wide temperature range. Their design supports effective heat dissipation, helping limit fouling during low-speed driving that is common in metropolitan settings across major global regions.

The single electrode spark plugs segment held 81.6% share in 2025. They remain the primary option for mass-market passenger cars and two-wheel vehicles, supported by more than 76 million units of global passenger car production in 2024. Most entry-level and mid-tier engines still depend on single electrode systems, which offer predictable operation and low maintenance costs. This makes them especially appealing for the aftermarket in regions with a large base of aging vehicles.

China Automotive Spark Plug Market held 46.8% share in 2024 and generated USD 824.4 million in 2025. Growth is tied to rising vehicle sales and rapid urban expansion, which continue to boost passenger car production beyond 28 million units. This accelerates OEM demand and replacement cycles in both major cities and smaller communities. Two-wheel mobility remains a large component of the transportation landscape, with around 7 million motorcycles and scooters produced in 2024, most of which relied on copper or platinum spark plugs, ensuring strong ongoing replacement needs.

Key companies participating in the Automotive Spark Plug Market include ACDelco, Autolite, Bosch, DENSO Corporation, Hyundai Mobis, MAHLE, Mitsubishi Electric, Niterra, Tenneco, and Valeo. Leading Automotive Spark Plug Market is strengthening its presence by expanding advanced material technologies, particularly through wider integration of iridium and platinum to improve durability and ignition precision. Many manufacturers are increasing R&D investments to support next-generation combustion systems and adapt to evolving engine designs. Companies are also focusing on broadening their global manufacturing footprints to reduce costs and improve supply reliability. Strategic collaborations with automakers remain essential for securing long-term OEM contracts, while an enhanced emphasis on aftermarket networks helps capture demand from aging vehicle fleets. In addition, several brands are modernizing their product portfolios with heat-range-optimized designs and cost-efficient options to reach both premium and mass-market customer segments.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Electrode

- 2.2.5 Sales Channel

- 2.2.6 Vehicle

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Growth in gasoline powered vehicles

- 3.2.1.3 Shift toward high efficiency engines

- 3.2.1.4 Increasing aftermarket activity

- 3.2.1.5 Adoption of precious metal plugs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Increasing penetration of electric vehicles

- 3.2.2.2 Rising raw material costs

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of the global aftermarket

- 3.2.3.2 Development of advanced ignition systems

- 3.2.3.3 Growth in two-wheeler demand in emerging markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electrode material evolution (copper to ruthenium)

- 3.7.1.2 Fine wire technology development

- 3.7.1.3 Multi-electrode design innovations

- 3.7.1.4 Pre-chamber spark plug technology

- 3.7.1.5 IoT & smart diagnostics integration

- 3.7.1.6 Laser welding manufacturing advances

- 3.7.1.7 Heat range optimization technologies

- 3.7.1.8 Next-generation materials

- 3.7.2 Emerging technologies

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 OEM vs aftermarket price differential

- 3.8.2 Regional price variations

- 3.8.3 Raw material cost impact

- 3.8.4 Import/export price analysis

- 3.8.5 Future price trajectory

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent & intellectual property analysis

- 3.11.1 Active patents by electrode material

- 3.11.2 Geographic patent distribution

- 3.11.3 Key patent holders

- 3.11.4 Emerging technology patents (smart plugs)

- 3.11.5 Patent expiration timeline (2024-2034)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Investment & Funding Analysis

- 3.13.1 R&D investment trends by manufacturer

- 3.13.2 Alternative fuel adaptation investments

- 3.13.3 Manufacturing capacity expansion

- 3.13.4 Strategic partnerships & joint ventures

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Hot spark plug

- 5.3 Cold spark plug

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Copper

- 6.3 Platinum

- 6.4 Iridium

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Electrode, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Single Electrode

- 7.3 Twin Electrode

- 7.4 Multi-Electrode

- 7.5 Surface Discharge

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Passenger car

- 9.2.1 Hatchback

- 9.2.2 Sedan

- 9.2.3 SUV

- 9.3 Commercial vehicle

- 9.3.1 Light duty

- 9.3.2 Medium duty

- 9.3.3 Heavy duty

- 9.4 Two-wheeler

- 9.4.1 Motorcycle

- 9.4.2 Scooter

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ACDelco

- 11.1.2 Autolite

- 11.1.3 Bosch

- 11.1.4 DENSO

- 11.1.5 MAHLE

- 11.1.6 Mitsubishi Electric

- 11.1.7 Niterra

- 11.1.8 Tenneco

- 11.1.9 Valeo

- 11.2 Regional Players

- 11.2.1 BorgWarner

- 11.2.2 Brisk Spark Plug Company

- 11.2.3 E3 Spark Plugs

- 11.2.4 Hella

- 11.2.5 MAGNETI MARELLI PARTS & SERVICES

- 11.2.6 MSD Performance

- 11.2.7 Stitt Spark Plug Company

- 11.2.8 Zhuzhou Torch Spark Plug

- 11.3 Emerging Players / Disruptors

- 11.3.1 Iskra Spark Plugs

- 11.3.2 Nanjing Leidian

- 11.3.3 Prenco Progress & Engineering Corporation

- 11.3.4 Pulstar

- 11.3.5 SMP Automotive

- 11.3.6 Weichai Power

火星塞导线市场按应用、产品类型、车辆类型、材料和分销管道划分,全球预测(2026-2032年)

火星塞导线市场按应用、产品类型、车辆类型、材料和分销管道划分,全球预测(2026-2032年) 点火变压器市场规模、份额和成长分析:按产品类型、额定功率容量、安装类型、最终用户产业、销售管道、地区和产业预测(2026-2033年)

点火变压器市场规模、份额和成长分析:按产品类型、额定功率容量、安装类型、最终用户产业、销售管道、地区和产业预测(2026-2033年) 全球火星塞市场规模、份额、趋势和成长分析报告(2026-2034年)

全球火星塞市场规模、份额、趋势和成长分析报告(2026-2034年) 汽车火星塞市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、产品类型、材料类型、需求类别、地区和竞争格局划分,2021-2031年)

汽车火星塞市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、产品类型、材料类型、需求类别、地区和竞争格局划分,2021-2031年) 火星塞市场规模、份额和成长分析(按类型、电极材料、销售管道、最终用途和地区划分)-2026-2033年产业预测

火星塞市场规模、份额和成长分析(按类型、电极材料、销售管道、最终用途和地区划分)-2026-2033年产业预测 火星塞市场报告,按材料(铜、铱、铂等)、产品类型(热火星塞、冷火星塞)、应用(汽车、船舶、航太等)、配销通路(OEM、售后市场)和地区划分,2025 年至 2033 年

火星塞市场报告,按材料(铜、铱、铂等)、产品类型(热火星塞、冷火星塞)、应用(汽车、船舶、航太等)、配销通路(OEM、售后市场)和地区划分,2025 年至 2033 年 全球火星塞市场预测(至 2032 年):按类型、材料、销售管道、应用、最终用户和地区

全球火星塞市场预测(至 2032 年):按类型、材料、销售管道、应用、最终用户和地区 全球汽车火星塞市场2026 年至 2032 年火星塞市场(按产品、车型、销售管道和地区划分)

全球汽车火星塞市场2026 年至 2032 年火星塞市场(按产品、车型、销售管道和地区划分) 汽车用火星塞的全球市场:各车辆类型,各电极材料类型,各销售管道,各地区,机会,预测,2018年~2032年

汽车用火星塞的全球市场:各车辆类型,各电极材料类型,各销售管道,各地区,机会,预测,2018年~2032年