|

市场调查报告书

商品编码

1892895

心臟消融市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Cardiac Ablation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

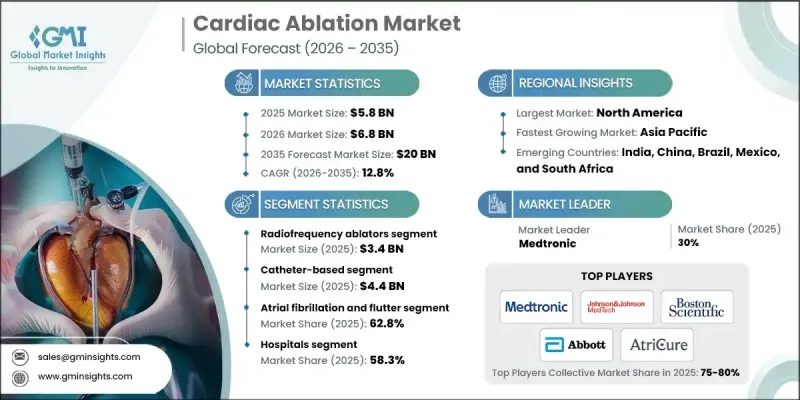

2025 年全球心臟消融市场价值为 58 亿美元,预计到 2035 年将以 12.8% 的复合年增长率增长至 200 亿美元。

心血管疾病(尤其是心律不整)发生率的上升,以及对微创手术和消融技术创新日益增长的需求,推动了心臟消融市场的扩张。人口老化加剧、生活方式的改变以及糖尿病和高血压等合併症发病率的上升,都加剧了心律不整病例的激增。患者往往需要传统药物治疗以外的干预措施,因此心臟消融术成为至关重要的解决方案。这些手术能够有效长期控制心律不整,减少住院次数,并提升病患的生活品质。随着医疗系统致力于降低死亡率和控制慢性心臟疾病,先进的消融技术在全球范围内广泛应用,推动了市场的发展。微创手术的普及是推动心臟消融市场发展的重要因素。与传统开胸手术相比,这些技术能够减少手术创伤、缩短住院时间、加快康復速度并降低併发症发生率。基于导管的射频消融和冷冻消融术在提供有效治疗的同时,最大限度地减少了患者的不适感,并改善了患者的预后。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 58亿美元 |

| 预测值 | 200亿美元 |

| 复合年增长率 | 12.8% |

射频消融器市场预计在2025年达到34亿美元,占58.1%的市场。这类设备透过向心肌组织输送可控热量来治疗心律不整,形成微小的病灶,阻断异常电讯号,进而恢復正常心律。由于其临床疗效显着,射频消融术被广泛认为是心律不整治疗的黄金标准。

预计到2025年,导管消融术市场规模将达44亿美元。导管消融术使用细而柔软的导管经血管插入心臟,将能量输送至致心律不整组织。这种微创方法可减少患者创伤、缩短復原时间并减少住院时间。心房颤动盛行率的上升以及患者对微创手术的日益青睐,使得导管消融术成为全球主要的治疗方法。

2025年,美国心臟消融市场规模预计将达23亿美元,反映了心血管疾病的高发生率。凭藉先进的医疗基础设施、庞大的手术量以及对创新解决方案的持续投入,美国在消融技术的应用和发展方面处于领先地位。先进的消融系统能够提供精准的治疗、更高的成功率和更低的併发症发生率,进而推动市场成长。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 患有心血管疾病(包括心律不整)的患者人数不断增加

- 对微创手术的需求不断增长

- 心臟消融装置的技术进步

- 产业陷阱与挑战

- 心臟消融手术风险较高

- 严格的监管环境

- 市场机会

- 脉衝场消融术的应用日益广泛

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 技术进步

- 当前技术趋势

- 新兴技术

- 2024年定价分析

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2022-2035年

- 射频消融器

- 电消融器

- 冷冻消融装置

- 超音波消融器

- 其他产品

第六章:市场估算与预测:依方法划分,2022-2035年

- 基于导管的

- 开放式/外科手术

第七章:市场估计与预测:依应用领域划分,2022-2035年

- 心房颤动和扑动

- 心跳过速

- 房性心搏过速

- 室性心搏过速

- 其他心跳过速

- 其他应用

第八章:市场估算与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 心臟中心

- 其他最终用途

第九章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Abbott Laboratories

- AngioDynamics

- AtriCure

- Biotronik

- Boston Scientific

- CardioFocus

- Japan Lifeline

- Johnson & Johnson MedTech

- Koninklijke Philips

- Medtronic

- MicroPort Scientific

- Olympus

- Osypka Medical

The Global Cardiac Ablation Market was valued at USD 5.8 billion in 2025 and is estimated to grow at a CAGR of 12.8% to reach USD 20 billion by 2035.

This market expansion is fueled by the rising prevalence of cardiovascular diseases, particularly cardiac arrhythmias, along with the increasing demand for minimally invasive procedures and innovations in ablation technologies. The growing aging population, lifestyle changes, and higher incidence of comorbidities such as diabetes and hypertension are contributing to the surge in arrhythmia cases. Patients often require interventions beyond conventional drug therapies, making cardiac ablation a critical solution. These procedures provide effective long-term management of arrhythmias, reducing hospital admissions and enhancing quality of life. As healthcare systems focus on lowering mortality and managing chronic cardiac conditions, advanced ablation technologies are gaining traction worldwide, driving the market. The adoption of minimally invasive procedures is a significant factor propelling the cardiac ablation market. These techniques offer reduced surgical trauma, shorter hospital stays, faster recovery, and lower complication rates compared to traditional open-heart surgery. Catheter-based radiofrequency and cryoablation procedures provide effective treatment while minimizing discomfort and improving patient outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.8 Billion |

| Forecast Value | $20 Billion |

| CAGR | 12.8% |

The radiofrequency ablators segment accounted for USD 3.4 billion in 2025, holding a 58.1% share. These devices treat arrhythmias by delivering controlled heat to cardiac tissue, creating small lesions that block abnormal electrical signals and restore normal heart rhythm. RF ablation is widely regarded as the gold standard in arrhythmia therapy due to its proven clinical success.

The catheter-based segment reached USD 4.4 billion in 2025. Catheter-based ablation uses thin, flexible tubes inserted through blood vessels to access the heart and deliver energy to arrhythmogenic tissue. This minimally invasive approach reduces patient trauma, shortens recovery, and lowers hospital stays. Rising atrial fibrillation prevalence and growing preference for minimally invasive interventions have made catheter-based ablation the dominant treatment method globally.

U.S. Cardiac Ablation Market was valued at USD 2.3 billion in 2025, reflecting the high prevalence of cardiovascular diseases. The country leads in the adoption and development of ablation technologies due to its advanced healthcare infrastructure, high procedural volumes, and continuous investment in innovative solutions. Advanced ablation systems provide precise treatment, high success rates, and reduced complications, reinforcing market growth.

Key players in the Cardiac Ablation Market include Medtronic, Boston Scientific, Abbott Laboratories, Olympus, Japan Lifeline, AtriCure, Biotronik, Johnson & Johnson MedTech, Koninklijke Philips, MicroPort Scientific, CardioFocus, Osypka Medical, and AngioDynamics. Companies in the Cardiac Ablation Market are adopting multiple strategies to strengthen their market position. They are heavily investing in research and development to introduce innovative and high-precision ablation devices. Strategic partnerships, collaborations, and mergers are being pursued to expand global reach and enhance technology portfolios. Geographic expansion into emerging markets is a key focus to capture rising demand. Firms are also emphasizing product differentiation through advanced catheter designs, energy modalities, and software integration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Approach trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of patients suffering from cardiovascular diseases including cardiac arrhythmias

- 3.2.1.2 Rising demand for minimally invasive procedures

- 3.2.1.3 Technological advancements in cardiac ablation devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk associated with cardiac ablation procedures

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of pulsed field ablation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Radiofrequency ablators

- 5.3 Electrical ablators

- 5.4 Cryoablation devices

- 5.5 Ultrasound ablators

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Approach, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Catheter-based

- 6.3 Open/Surgical

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Atrial Fibrillation and flutter

- 7.3 Tachycardia

- 7.3.1 Atrial tachycardia

- 7.3.2 Ventricular tachyarrhythmias

- 7.3.3 Other tachycardia

- 7.4 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Cardiac centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 AngioDynamics

- 10.3 AtriCure

- 10.4 Biotronik

- 10.5 Boston Scientific

- 10.6 CardioFocus

- 10.7 Japan Lifeline

- 10.8 Johnson & Johnson MedTech

- 10.9 Koninklijke Philips

- 10.10 Medtronic

- 10.11 MicroPort Scientific

- 10.12 Olympus

- 10.13 Osypka Medical