|

市场调查报告书

商品编码

1892896

门诊肿瘤输液市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Outpatient Oncology Infusion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

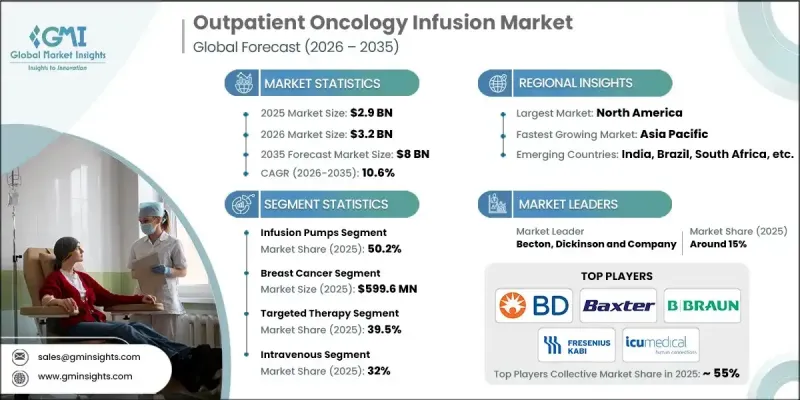

2025 年全球门诊肿瘤输液市场价值为 29 亿美元,预计到 2035 年将以 10.6% 的复合年增长率增长至 80 亿美元。

市场扩张的驱动因素包括:人们对经济实惠的门诊治疗的需求日益增长、癌症发病率上升、政府推行癌症宣传倡议以及输液技术的进步。标靶治疗和免疫疗法的日益普及、以价值为导向的医疗模式的转变以及远距医疗辅助输液服务的兴起,进一步推动了市场需求。生活方式因素、肥胖和环境影响导致癌症病例不断增加,加剧了对有效且便捷治疗的需求。与住院治疗相比,门诊输液中心为患者提供更方便且有效率的治疗模式,同时降低整体成本。此外,先进的智慧输液帮浦整合了自动给药、错误警报和电子健康记录 (EHR) 相容性等功能,提高了安全性和操作效率,进一步增强了门诊肿瘤输液服务在全球范围内的吸引力。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 29亿美元 |

| 预测值 | 80亿美元 |

| 复合年增长率 | 10.6% |

到2025年,输液帮浦市占率将达到50.2%。这些设备采用便携式设计,并整合了智慧系统,能够提升患者舒适度,实现灵活的给药方式,并支援精准给药。输液帮浦技术的进步是门诊输液服务发展的关键。

到2025年,标靶治疗市占率将达到39.5%。这类疗法作用于与癌症相关的特定分子通路,并透过可控输注给药。门诊输注中心是此类疗法的首选给药地点,因此需要先进的输注设备和熟练的医护人员来监测精确的剂量和患者的反应。

北美门诊肿瘤输液市场在2025年占据43.1%的市场份额,预计未来将显着成长。该地区受益于先进的医疗基础设施、庞大的癌症患者群体以及创新输液技术的广泛应用。全面的保险覆盖和以价值为导向的医疗模式的转变,使得患者能够以比住院治疗更低的成本获得门诊癌症治疗。智慧输液帮浦和整合电子病历系统在门诊中心的应用,提高了病患安全性和营运效率,进一步推动了市场成长。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 全球癌症发生率不断上升

- 人们越来越倾向选择经济实惠的门诊服务

- 输液帮浦的技术进步

- 政府加大力度提高癌症防治意识

- 产业陷阱与挑战

- 癌症治疗费用高昂

- 机会

- 采用具有电子健康记录互通性的智慧型输液泵

- 开发生物相似药以降低治疗成本

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价值链分析

- 报销方案

- 政策环境

- 流行病学情景

- 波特的分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 点滴帮浦

- 静脉输液装置

- 静脉导管

- 无针头连接器

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 肺癌

- 肝癌

- 乳癌

- 摄护腺癌

- 其他癌症

第七章:市场估计与预测:依疗法划分,2021-2034年

- 化疗

- 标靶治疗

- 免疫疗法

- 荷尔蒙疗法

第八章:市场估算与预测:依模式划分,2021-2034年

- 肌肉内注射(IM)

- 静脉注射(IV)

- 皮下

- 其他模式

第九章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 奈及利亚

- 埃及

第十章:公司简介

- B. Braun

- Baxter

- Becton, Dickinson and Company

- Fresenius Kabi

- ICU Medical

- IRADIMED

- Medtronic

- Micrel

- MOOG

- NIPRO

- Penlon

- Teleflex

- Terumo

The Global Outpatient Oncology Infusion Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 8 billion by 2035.

The market expansion is fueled by increasing preference for cost-efficient outpatient care, rising cancer prevalence, government initiatives promoting cancer awareness, and advancements in infusion technologies. Rising adoption of targeted therapies and immunotherapies, the shift toward value-based care, and telehealth-assisted infusion services are further driving demand. Lifestyle factors, obesity, and environmental influences contribute to the growing number of cancer cases, increasing the need for effective and accessible treatments. Outpatient infusion centers provide patients with a more convenient and efficient treatment model while reducing overall costs compared to hospitalization. Additionally, the integration of advanced smart infusion pumps with automated dosing, error alerts, and electronic health record (EHR) compatibility has enhanced both safety and operational efficiency, strengthening the appeal of outpatient oncology infusion services worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $8 Billion |

| CAGR | 10.6% |

The infusion pumps segment held a 50.2% share in 2025. These devices, featuring portable designs and smart system integration, enhance patient comfort, allow flexible administration, and support precise dosing. Technological improvements in pumps are central to the growth of outpatient infusion services.

The targeted therapy segment accounted for a 39.5% share in 2025. These therapies act on specific molecular pathways linked to cancer and delivered through controlled infusion. Outpatient infusion centers are preferred for their administration, driving the need for advanced infusion devices and skilled personnel to monitor accurate dosing and patient response.

North America Outpatient Oncology Infusion Market held 43.1% share in 2025 and is expected to grow significantly. The region benefits from advanced healthcare infrastructure, a high number of cancer patients, and strong adoption of innovative infusion technologies. Comprehensive insurance coverage and the shift toward value-based care allow patients to access outpatient cancer treatments more affordably than in hospital settings. Adoption of smart infusion pumps and integrated EHR systems in outpatient centers enhances patient safety and operational workflow, further boosting market growth.

Key companies operating in the Global Outpatient Oncology Infusion Market include B. Braun, Baxter, Fresenius Kabi, Medtronic, MOOG, IRADIMED, Micrel, NIPRO, Teleflex, Terumo, ICU Medical, Penlon, and Becton, Dickinson and Company. Companies in the Global Outpatient Oncology Infusion Market focus on strategies such as continuous product innovation in smart infusion pumps, integration of digital health platforms, and development of user-friendly, portable devices to improve patient outcomes. Expansion into new geographic regions and partnerships with healthcare providers enhance market reach. Firms also invest in training programs for clinical staff to ensure accurate administration of therapies. Additionally, collaborations with telehealth services, EHR integration, and value-based care initiatives strengthen operational efficiency, patient safety, and long-term adoption, helping companies solidify their market foothold and maintain leadership in a competitive environment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Therapy trends

- 2.2.5 Mode trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer across the globe

- 3.2.1.2 Increasing preference for cost-effective outpatient care

- 3.2.1.3 Technological advancements in infusion pumps

- 3.2.1.4 Surging government initiatives for cancer awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of cancer therapies

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of smart infusion pumps with EHR interoperability

- 3.2.3.2 Development of biosimilars to reduce treatment costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Reimbursement scenario

- 3.8 Policy landscape

- 3.9 Epidemiology scenario

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Infusion pumps

- 5.3 Intravenous sets

- 5.4 IV cannulas

- 5.5 Needleless connectors

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Lung cancer

- 6.3 Liver cancer

- 6.4 Breast cancer

- 6.5 Prostate cancer

- 6.6 Other cancers

Chapter 7 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chemotherapy

- 7.3 Targeted therapy

- 7.4 Immunotherapy

- 7.5 Hormonal therapy

Chapter 8 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Intramuscular (IM)

- 8.3 Intravenous (IV)

- 8.4 Subcutaneous

- 8.5 Other modes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Nigeria

- 9.6.5 Egypt

Chapter 10 Company Profiles

- 10.1 B. Braun

- 10.2 Baxter

- 10.3 Becton, Dickinson and Company

- 10.4 Fresenius Kabi

- 10.5 ICU Medical

- 10.6 IRADIMED

- 10.7 Medtronic

- 10.8 Micrel

- 10.9 MOOG

- 10.10 NIPRO

- 10.11 Penlon

- 10.12 Teleflex

- 10.13 Terumo