|

市场调查报告书

商品编码

1892898

分析仪器市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Analytical Instrumentation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

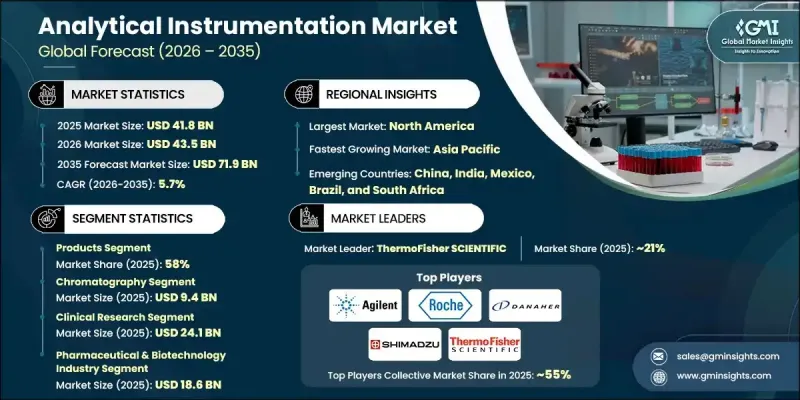

2025年全球分析仪器市场价值为418亿美元,预计到2035年将以5.7%的复合年增长率成长至719亿美元。

製药和生物技术领域研发投入的增加、精准医疗分析系统应用的日益普及、慢性病和传染病的日益流行,以及监管机构对已验证分析方案的合规性要求,共同推动了分析仪器的发展。分析仪器使实验室能够提供高精度测量、即时监测和进阶资料分析,从而支持实证临床决策和优化治疗策略。临床、参考和研究实验室对高通量、高灵敏度检测的需求不断增长,进一步加速了这些系统的应用。这些系统对于杂质分析、生物製剂特性、批次放行和稳定性测试至关重要。这些仪器使科学家和临床医生能够以无与伦比的精度分析样本的化学、物理和分子特性,使其在医疗保健、製药和工业应用领域发挥关键作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 418亿美元 |

| 预测值 | 719亿美元 |

| 复合年增长率 | 5.7% |

到2025年,产品板块占据58%的市场份额,这主要得益于医药研发、诊断和工业检测领域对先进仪器的强劲需求。持续的技术创新以及对精准、高通量分析工具日益增长的需求进一步巩固了这个市场主导地位。

由于色谱技术能够精确分离、鑑定和定量复杂的化学混合物,预计到2025年,该领域将创造94亿美元的产值。实验室高度依赖色谱技术进行品质控制、配方开发、稳定性测试和杂质分析,这巩固了其在研发密集型工作流程中的核心地位。

2025年,美国分析仪器市场规模达到146亿美元,预计2035年将以5.8%的复合年增长率成长。这一领先地位源于成熟的製药、生物技术和临床诊断生态系统、先进的实验室基础设施以及严格的监管要求。 FDA、USP、CDC和CMS/CLIA等机构对药物研发、生物製品生产和临床诊断实施严格的分析验证,从而推动了对高精度仪器的持续需求,包括色谱仪、光谱仪、质谱仪、分子分析平台和颗粒表征工具等,这些仪器广泛应用于研究、品质控制和临床实验室。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 製药业和政府研究机构的研发支出不断增加

- 分析仪器的技术进步

- 分析仪器在精准医疗应用的应用日益广泛

- 慢性病和传染病日益普遍,需要准确的检测。

- 监管合规性推动了经验证的分析系统的应用

- 分子诊断和基于PCR的早期检测平台的扩展

- 产业陷阱与挑战

- 仪器成本高昂

- 缺乏熟练专业人员

- 市场机会

- 即时检测的成长

- 药物发现和开发活动激增

- 成长驱动因素

- 成长潜力分析

- 价值链分析

- 管道分析

- 2025年各地区定价分析

- 2022-2035年销售分析

- 未来市场趋势

- 监管环境

- 技术格局

- 目前技术

- 新兴技术

- 差距分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品与服务划分,2022-2035年

- 产品

- 色谱仪器

- 光谱仪

- 分子分析仪器

- 粒子计数器和分析器

- 电化学分析仪

- 其他产品

- 服务和耗材

第六章:市场估算与预测:依技术划分,2022-2035年

- 色谱法

- 液相层析法

- 气相层析法

- 离子色谱法

- 光谱学

- 聚合酶炼式反应

- 颗粒分析

- 其他技术

第七章:市场估计与预测:依应用领域划分,2022-2035年

- 临床研究

- 临床诊断

第八章:市场估算与预测:依最终用途划分,2022-2035年

- 製药和生物技术产业

- 研究和学术机构

- 诊断中心

- 其他最终用途

第九章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 波兰

- 瑞典

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 泰国

- 印尼

- 菲律宾

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 智利

- 秘鲁

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 以色列

- 土耳其

- 伊朗

第十章:公司简介

- Agilent

- Avantor

- BIO RAD

- BRUKER

- Danaher

- Eppendorf

- HITACHI

- Illumina

- Malvern Panalytical (Spectris)

- METTLER TOLEDO

- Metrohm AG

- Revvity

- Roche

- SARTORIUS

- SHIMADZU

- ThermoFisher SCIENTIFIC

- Waters

- ZEISS

The Global Analytical Instrumentation Market was valued at USD 41.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 71.9 billion by 2035.

The growth is fueled by increased R&D investments in the pharmaceutical and biotech sectors, rising adoption of analytical systems for precision medicine, the growing prevalence of chronic and infectious diseases, and regulatory mandates driving compliance with validated analytical protocols. Analytical instrumentation enables laboratories to deliver highly accurate measurements, real-time monitoring, and advanced data analytics, supporting evidence-based clinical decision-making and optimized treatment strategies. The rising demand for high-throughput, sensitive testing in clinical, reference, and research laboratories is further accelerating the adoption of these systems, which are essential for impurity profiling, biologics characterization, batch release, and stability testing. These instruments allow scientists and clinicians to analyze chemical, physical, and molecular properties of samples with unmatched precision, making them critical across healthcare, pharmaceutical, and industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $41.8 Billion |

| Forecast Value | $71.9 Billion |

| CAGR | 5.7% |

The products segment held 58% share in 2025, driven by strong demand for advanced instruments in pharmaceutical R&D, diagnostics, and industrial testing. This dominance is reinforced by continuous technological innovation and the growing need for precise, high-throughput analytical tools.

The chromatography segment generated USD 9.4 billion in 2025, due to its ability to separate, identify, and quantify complex chemical mixtures accurately. Laboratories heavily rely on chromatography for quality control, formulation development, stability testing, and impurity profiling, solidifying its central role in research-intensive workflows.

U.S. Analytical Instrumentation Market reached USD 14.6 billion in 2025 and is expected to grow at a CAGR of 5.8% through 2035. This leadership stems from a mature pharmaceutical, biotechnology, and clinical diagnostics ecosystem, advanced laboratory infrastructure, and stringent regulatory requirements. Agencies such as the FDA, USP, CDC, and CMS/CLIA enforce rigorous analytical validation for drug development, biologics manufacturing, and clinical diagnostics, driving sustained demand for high-precision instruments, including chromatography, spectroscopy, mass spectrometry, molecular analysis platforms, and particle characterization tools across research, quality control, and clinical laboratories.

Key players in the Global Analytical Instrumentation Market include Bruker, Waters, Eppendorf, Agilent, Illumina, Avantor, Revvity, Shimadzu, METTLER TOLEDO, Bio-Rad, Malvern Panalytical (Spectris), Roche, Sartorius, Hitachi, ThermoFisher Scientific, Metrohm AG, Zeiss, and Danaher. To strengthen their Analytical Instrumentation Market position, companies are focusing on product innovation, expanding instrument portfolios, and integrating advanced technologies such as AI, IoT, and automation into their analytical platforms. Strategic collaborations with pharmaceutical, biotech, and research institutions help accelerate the adoption of cutting-edge systems. Firms are investing in digital services, predictive maintenance, and cloud-enabled analytics to improve workflow efficiency and uptime. Global expansion into emerging markets, targeted marketing campaigns, and customized solutions for clinical, industrial, and research applications further reinforce brand presence and foster long-term client relationships.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product & services trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising R&D spending by the pharmaceutical industry and government research organizations

- 3.2.1.2 Technological advancements in analytical instruments

- 3.2.1.3 Increasing adoption of analytical instrumentation for precision medicine applications

- 3.2.1.4 Growing prevalence of chronic and infectious diseases requiring accurate testing

- 3.2.1.5 Regulatory compliance driving adoption of validated analytical systems

- 3.2.1.6 Expansion of molecular diagnostics and PCR-based platforms for early detection

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of instruments

- 3.2.2.2 Lack of skilled professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in point-of-care testing

- 3.2.3.2 Surge in drug discovery and development activities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Value chain analysis

- 3.5 Pipeline analysis

- 3.6 Pricing analysis, by region, 2025

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Volume analysis, 2022 - 2035

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 MEA

- 3.8 Future market trends

- 3.9 Regulatory landscape

- 3.10 Technology landscape

- 3.10.1 Current technologies

- 3.10.2 Emerging technologies

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product & Services, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Products

- 5.2.1 Chromatography instruments

- 5.2.2 Spectroscopy instruments

- 5.2.3 Molecular analysis instruments

- 5.2.4 Particle counters and analyzers

- 5.2.5 Electrochemical analysis instruments

- 5.2.6 Other products

- 5.3 Services & consumables

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Chromatography

- 6.2.1 Liquid chromatography

- 6.2.2 Gas chromatography

- 6.2.3 Ion chromatography

- 6.3 Spectroscopy

- 6.4 Polymerase chain reaction

- 6.5 Particle analysis

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical research

- 7.3 Clinical diagnostics

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical & biotechnology industry

- 8.3 Research and academic institutes

- 8.4 Diagnostic centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Sweden

- 9.3.8 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Thailand

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.5.5 Chile

- 9.5.6 Peru

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Israel

- 9.6.5 Turkey

- 9.6.6 Iran

Chapter 10 Company Profiles

- 10.1 Agilent

- 10.2 Avantor

- 10.3 BIO RAD

- 10.4 BRUKER

- 10.5 Danaher

- 10.6 Eppendorf

- 10.7 HITACHI

- 10.8 Illumina

- 10.9 Malvern Panalytical (Spectris)

- 10.10 METTLER TOLEDO

- 10.11 Metrohm AG

- 10.12 Revvity

- 10.13 Roche

- 10.14 SARTORIUS

- 10.15 SHIMADZU

- 10.16 ThermoFisher SCIENTIFIC

- 10.17 Waters

- 10.18 ZEISS

全球技术无尘室显微镜销售市场报告、竞争分析及区域商机(2026-2032年)

全球技术无尘室显微镜销售市场报告、竞争分析及区域商机(2026-2032年) 分子交互作用测量仪器市场:按技术、产品、应用和最终用户划分,全球预测,2026-2032年小型垂直电泳系统市场:依产品类型、方法、自动化程度、处理能力、价格范围、凝胶类型、应用、最终用户划分,全球预测,2026-2032年微型电泳槽市场:按类型、模式、产品、应用、最终用户划分,全球预测(2026-2032)旋转式显微镜物镜转换器市场:依产品类型、显微镜类型、物镜转换器设计、应用、最终用户划分,全球预测(2026-2032)科学研究设备市场:依设备类型、设备配置、应用、应用领域及销售管道划分-2026-2032年全球预测高低温培养箱市场:依产品类型、通路、温度范围、应用、最终用户划分,全球预测(2026-2032)显微镜观察管市场:全球预测(2026-2032年),依产品类型、材料、销售管道、应用和最终用户划分高速气相层析市场:按应用、检测器类型、产品类型、最终用户、技术和销售管道,全球预测,2026-2032年高频脉衝器市场:按产品类型、供应类型、应用和最终用户产业划分,全球预测,2026-2032年

分子交互作用测量仪器市场:按技术、产品、应用和最终用户划分,全球预测,2026-2032年小型垂直电泳系统市场:依产品类型、方法、自动化程度、处理能力、价格范围、凝胶类型、应用、最终用户划分,全球预测,2026-2032年微型电泳槽市场:按类型、模式、产品、应用、最终用户划分,全球预测(2026-2032)旋转式显微镜物镜转换器市场:依产品类型、显微镜类型、物镜转换器设计、应用、最终用户划分,全球预测(2026-2032)科学研究设备市场:依设备类型、设备配置、应用、应用领域及销售管道划分-2026-2032年全球预测高低温培养箱市场:依产品类型、通路、温度范围、应用、最终用户划分,全球预测(2026-2032)显微镜观察管市场:全球预测(2026-2032年),依产品类型、材料、销售管道、应用和最终用户划分高速气相层析市场:按应用、检测器类型、产品类型、最终用户、技术和销售管道,全球预测,2026-2032年高频脉衝器市场:按产品类型、供应类型、应用和最终用户产业划分,全球预测,2026-2032年