|

市场调查报告书

商品编码

1892899

生物样本采集试剂盒市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Biological Sample Collection Kits Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

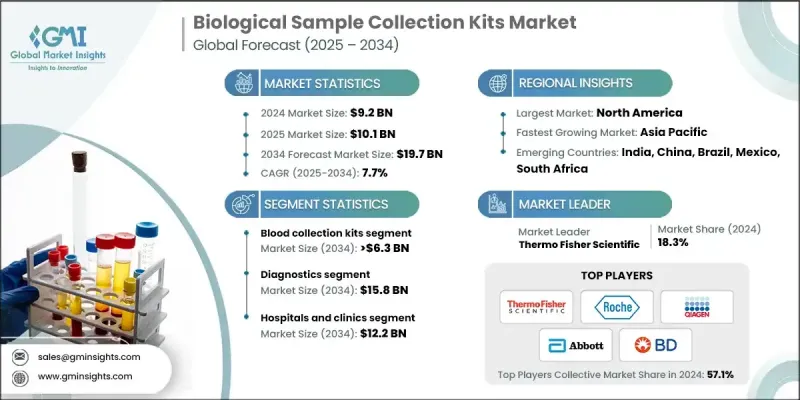

2024 年全球生物样本采集试剂盒市场价值为 92 亿美元,预计到 2034 年将以 7.7% 的复合年增长率增长至 197 亿美元。

随着对诊断检测、生物样本库和个人化医疗等高度依赖精准生物标记分析的项目的需求不断增长,市场持续扩张。这些试剂盒透过保护样本品质和确保结果可靠,为实验室、医疗机构、诊断公司和生物製药企业提供支援。种类繁多的产品,例如血液和尿液采集试剂盒、病毒转运培养基、唾液采集系统和自采样工具,能够实现安全、稳定、无污染的临床和科学研究操作。分子诊断(包括新一代定序和基于PCR的检测)的兴起,进一步推动了先进分析平台优化的专用试剂盒的需求。远距医疗的日益普及也加速了居家采集解决方案的推广,这些方案不仅方便患者,还能减轻临床机构的负担。此外,监管机构对样本安全性和可追溯性的关注,也促进了条码包装、防篡改设计和耐温包装等方面的创新。实验室自动化程度的提高以及针对特定样本类型客製化试剂盒的需求,进一步支撑了市场的长期发展势头。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 92亿美元 |

| 预测值 | 197亿美元 |

| 复合年增长率 | 7.7% |

预计到2034年,拭子市场将以7.2%的复合年增长率成长。成长的主要驱动因素是传染病诊断、微生物组研究和快速检测流程中对非侵入性采样需求的不断增长。拭子具有可靠性和广泛的可用性,使其成为医院、实验室和即时检测环境中不可或缺的工具。

2024年,诊断业务占据78.9%的市场份额,预计2034年将达到158亿美元。全球慢性病和传染病发病率的上升推动了诊断检测的持续应用,以支持早期发现和治疗方案的发展。采集试剂盒是这些工作流程中的关键环节,它们能够保持样本的完整性,并透过及时的健康评估来帮助降低医疗成本。

预计到2024年,北美生物样本采集试剂盒市占率将达到32.4%。强大的医疗基础设施、先进诊断技术的广泛应用以及健全的研究生态系统,持续支撑着生物样本采集试剂盒的高利用率。代谢性疾病、心臟病、肿瘤和传染病病例的不断增加,进一步凸显了该地区对可靠诊断工具的需求。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 实验室检测数量不断增加

- 实验室检验在精准疾病诊断的应用日益广泛

- 样品采集技术的研发活动日益增多,技术也不断进步。

- 生物样本库和个人化医疗的扩展

- 产业陷阱与挑战

- 先进试剂盒价格昂贵,且采样过程复杂。

- 市场机会

- 居家和远端采样工具包的使用率不断提高

- 自动化和数位追踪解决方案的集成

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 技术格局

- 当前技术趋势

- 便携式和家用生物样本采集试剂盒的成长

- 支援远端样本追踪的数位健康平台

- 方便患者自行采集且微创的试剂盒

- 新兴技术

- 人工智慧驱动的样品品质监测和预测分析

- 穿戴式和连网的样本采集设备

- 具备自适应稳定和保存功能的智慧套件

- 当前技术趋势

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

- 人工智慧、数位医疗和互联诊断的融合

- 扩大居家自取样检测方案

- 新兴市场成长,医疗基础建设得到改善

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 竞争定位矩阵

- 主要市场参与者的竞争分析

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 采血包

- 尿液采集套装

- 拭子

- 鼻咽拭子

- 口咽拭子

- 鼻拭子

- 病毒运输培养基

- 其他产品

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 诊断

- 研究

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 医院和诊所

- 诊断中心

- 居家照护

- 其他最终用途

第八章:市场估算与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Abbott

- Altona Diagnostics

- Becton, Dickinson and Company (BD)

- CTK Biotech

- Hardy Diagnostics

- HiMedia Laboratories

- Labcorp

- Lucence Health

- Miraclean Technology

- Puritan Medical

- QIAGEN

- Roche

- Seegene

- Thermo Fisher Scientific

- VIRCELL MEDICAL

The Global Biological Sample Collection Kits Market was valued at USD 9.2 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 19.7 billion by 2034.

The market continues to grow as demand rises for diagnostic testing, biobanking, and personalized medicine initiatives that rely heavily on accurate biomarker analysis. These kits support laboratories, healthcare facilities, diagnostics companies, and biopharmaceutical organizations by preserving sample quality and ensuring dependable results. A wide range of products, such as blood and urine collection kits, viral transport media, saliva-based systems, and self-sampling tools, enable safe, consistent, contamination-free handling for both clinical and research purposes. The shift toward molecular diagnostics, including next-generation sequencing and PCR-based testing, is expanding the need for specialized kits optimized for advanced analytical platforms. Increasing use of telemedicine is also accelerating the adoption of at-home collection solutions that offer patient convenience and reduce the burden on clinical settings. Additionally, regulatory attention on sample security and traceability is encouraging innovation in barcoded packaging, tamper-resistant designs, and temperature-stable formats. Growing automation in laboratories and the push for kits tailored to specific specimen types are further supporting long-term market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $19.7 Billion |

| CAGR | 7.7% |

The swabs segment is expected to grow at a CAGR of 7.2% through 2034. Growth is influenced by increasing demand for non-invasive sampling across infectious disease diagnostics, microbiome research, and rapid testing workflows. Their reliability and widespread availability make swabs essential in hospitals, laboratory settings, and point-of-care environments.

The diagnostics segment held a 78.9% share in 2024 and is anticipated to achieve USD 15.8 billion by 2034. Rising rates of chronic and infectious illnesses worldwide are driving consistent use of diagnostic testing to support early detection and treatment planning. Collection kits form a critical part of these workflows by maintaining sample integrity and helping reduce medical costs through timely health assessments.

North America Biological Sample Collection Kits Market accounted for a 32.4% share in 2024. Strong healthcare infrastructure, broad access to advanced diagnostic technologies, and robust research ecosystems continue to support high utilization of biological sampling kits. Increasing case numbers for metabolic, cardiac, oncological, and infectious conditions further reinforce the need for reliable diagnostic tools across the region.

Leading companies active in the Global Biological Sample Collection Kits Market include Abbott, Altona Diagnostics, Becton, Dickinson and Company (BD), CTK Biotech, Hardy Diagnostics, HiMedia Laboratories, Labcorp, Lucence Health, Miraclean Technology, Puritan Medical, QIAGEN, Roche, Seegene, Thermo Fisher Scientific, and VIRCELL MEDICAL. Companies competing in the Biological Sample Collection Kits Market use a variety of strategies to strengthen their presence. Many are expanding product portfolios with specialized kits that support molecular testing, personalized medicine, and at-home diagnostics. Investments in automation-ready systems, tamper-proof designs, and advanced tracking features help improve accuracy and traceability. Firms are enhancing global distribution networks and forming partnerships with laboratories, biotech companies, and healthcare providers to widen market access. Significant focus is placed on compliance with evolving regulatory standards to ensure product reliability across regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of laboratory tests

- 3.2.1.2 Rising usage of lab tests for precise disease diagnosis

- 3.2.1.3 Growing R&D activities and technological advancements in sample collection techniques

- 3.2.1.4 Expansion of biobanking and personalized medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced kits and complexities associated with specimen collection

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of at-home and remote sample collection kits

- 3.2.3.2 Integration of automation and digital tracking solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Growth of portable and home-based biological sample collection kits

- 3.5.1.2 Digital health platforms enabling remote sample tracking

- 3.5.1.3 Patient-friendly self-collection and minimally invasive kits

- 3.5.2 Emerging technologies

- 3.5.2.1 AI-powered sample quality monitoring and predictive analytics

- 3.5.2.2 Wearable and connected sample collection devices

- 3.5.2.3 Smart kits with adaptive stabilization and preservation features

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Integration of AI, digital health, and connected diagnostics

- 3.9.2 Expansion of home-based and self-collection testing solutions

- 3.9.3 Growth in emerging markets with enhanced healthcare infrastructure

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Blood collection kits

- 5.3 Urine collection kits

- 5.4 Swabs

- 5.4.1 Nasopharyngeal (NP) swabs

- 5.4.2 Oropharyngeal (OP) swabs

- 5.4.3 Nasal swabs

- 5.5 Viral transport media

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostics

- 6.3 Research

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Diagnostic centers

- 7.4 Homecare

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Altona Diagnostics

- 9.3 Becton, Dickinson and Company (BD)

- 9.4 CTK Biotech

- 9.5 Hardy Diagnostics

- 9.6 HiMedia Laboratories

- 9.7 Labcorp

- 9.8 Lucence Health

- 9.9 Miraclean Technology

- 9.10 Puritan Medical

- 9.11 QIAGEN

- 9.12 Roche

- 9.13 Seegene

- 9.14 Thermo Fisher Scientific

- 9.15 VIRCELL MEDICAL