|

市场调查报告书

商品编码

1913279

金属成型设备市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Metal Forming Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

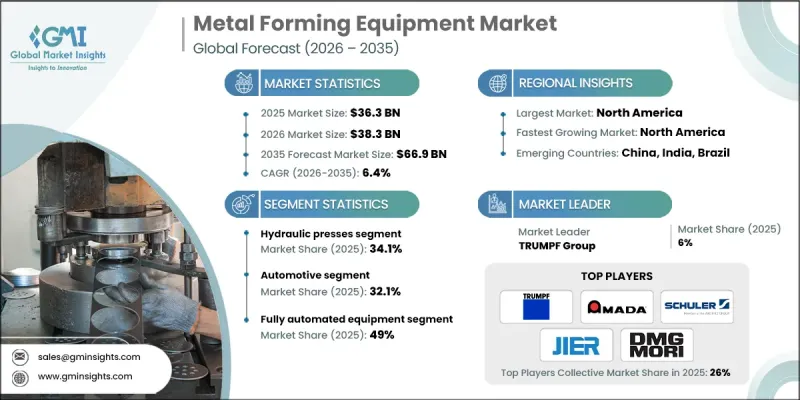

全球金属成型设备市场预计到 2025 年将达到 363 亿美元,到 2035 年将达到 669 亿美元,年复合成长率为 6.4%。

随着製造商采用先进的数位化製造方法和新一代设备架构,整个产业正经历着翻天覆地的变革。智慧製造框架日益整合基于感测器的监控、即时数据处理和预测性维护,以提高精度、一致性和运作可靠性。数位化生产环境能够更精确地控製成形参数,进而提高能源效率和产品品质。一场重大的技术变革也在进行中,伺服电动压力机系统的应用日益广泛,与传统方案相比,它具有更卓越的运动控制和更低的能耗。随着各产业优先考虑轻量材料和复杂几何形状,需求模式也不断演变,推动着成形方法和模具设计的创新。交通运输和航太製造业的电气化趋势正在推动对高精度、高重复性成形解决方案的需求。这些因素共同重塑了资本投资策略,并迫使设备供应商提供更智慧、更柔软性、更自动化的平台。长期的工业现代化倡议以及全球生产基地对高性能製造设备的持续需求,正使市场受益匪浅。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 363亿美元 |

| 预测金额 | 669亿美元 |

| 复合年增长率 | 6.4% |

到2035年,汽车产业将以7.3%的复合年增长率成长,巩固其作为设备创新关键驱动力的地位。向电动化移动平台的转型正在推动对先进成型系统的需求,这些系统能够处理轻质高强度材料,同时保持精度和结构完整性。

到 2025 年,全自动金属成型设备市占率将达到 49% 。人事费用上升、劳动力短缺以及对连续生产日益增长的需求,正促使製造商采用整合机器人、智慧控制和最大限度减少人为干预的自动化技术。

美国金属成型设备市场占全球市场份额的82.1%,营收达115亿美元,年复合成长率达7%。强有力的联邦投资计画和工业现代化倡议正在推动多个产业对精密成型零件的需求。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 电动车(EV)的兴起和轻量化

- 工业4.0和自动化集成

- 全球基础设施发展与工业化

- 产业潜在风险与挑战

- 高额资本投入和较长的投资回收期

- 技术纯熟劳工和工程师短缺

- 机会

- 新兴经济体尚未开发的市场

- 实体世界与数位世界的融合(STEAM)

- 绿色製造和节能设备

- 将供应链迁回邻近地区

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 油压机

- 机械压力机

- 轧延

- 其他的

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 车

- 航太/国防

- 建造

- 电子设备

- 其他的

7. 依自动化程度分類的市场估算与预测,2022-2035 年

- 全自动设备

- 半自动化设备

第八章 按分销管道分類的市场估算与预测,2022-2035年

- 在线的

- 离线

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- TRUMPF Group

- Amada Co., Ltd.

- Schuler AG

- JIER Machine-Tool Group

- DMG Mori

- AIDA Engineering

- Komatsu Ltd.

- Fagor Arrasate

- Haas Automation

- BYSTRONIC

- Mitsubishi HI Machine Tool

- Cincinnati Incorporated

- LVD Group

- MAG IAS

- Bliss-Bret Industries

- WardJet

- Prima Industrie

- Salvagnini

- Ermaksan

- Hyundai Rotem

The Global Metal Forming Equipment Market was valued at USD 36.3 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 66.9 billion by 2035.

The industry undergoes a structural transformation as manufacturers adopt advanced digital manufacturing practices and next-generation equipment architectures. Smart manufacturing frameworks increasingly integrate sensor-based monitoring, real-time data processing, and predictive maintenance to enhance precision, consistency, and operational reliability. Digitalized production environments allow tighter control over forming parameters while improving energy efficiency and output quality. A major technological transition also takes shape as servo-electric press systems gain wider acceptance due to their superior motion control and reduced energy consumption when compared to legacy alternatives. Demand patterns further evolve as industries prioritize lightweight materials and complex geometries, driving innovation in forming methods and tooling design. Electrification trends across transportation and aerospace manufacturing intensify requirements for highly accurate and repeatable forming solutions. These converging factors reshape capital investment strategies and push equipment suppliers to deliver smarter, more flexible, and automation-ready platforms. The market benefits from long-term industrial modernization initiatives and sustained demand for high-performance manufacturing equipment across global production hubs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.3 Billion |

| Forecast Value | $66.9 Billion |

| CAGR | 6.4% |

The automotive segment will grow at a CAGR of 7.3% through 2035, reinforcing its position as the primary catalyst for equipment innovation. The shift toward electrified mobility platforms increases demand for advanced forming systems capable of handling lightweight and high-strength materials while maintaining precision and structural integrity.

The fully automated metal forming equipment segment accounted for 49% share in 2025. Rising labor costs, workforce shortages, and demand for continuous production encourage manufacturers to deploy automation technologies that integrate robotics, intelligent controls, and minimal human intervention.

U.S. Metal Forming Equipment Market held 82.1% share, generating USD 11.5 billion and achieving a CAGR of 7%. Strong federal investment programs and industrial modernization initiatives drive demand for precision-formed components across multiple sectors.

Key companies operating in the Global Metal Forming Equipment Market include Schuler AG, TRUMPF Group, Amada Co., Ltd., DMG Mori, BYSTRONIC, Komatsu Ltd., Haas Automation, AIDA Engineering, Fagor Arrasate, JIER Machine-Tool Group, Mitsubishi HI Machine Tool, LVD Group, Cincinnati Incorporated, Salvagnini, MAG IAS, Ermaksan, Prima Industrie, WardJet, Bliss-Bret Industries, and Hyundai Rotem. Companies strengthen their position through continuous investment in automation, digital integration, and energy-efficient equipment design. Many manufacturers focus on developing modular systems that offer flexibility across multiple applications while reducing downtime. Strategic partnerships with end users support the co-development of customized solutions aligned with evolving production needs. Expanding service capabilities, including remote monitoring and lifecycle support, improves customer retention and operational reliability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Age group

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise of Electric Vehicles (EVs) & Lightweighting

- 3.2.1.2 Integration of Industry 4.0 & Automation

- 3.2.1.3 Global Infrastructure Development & Industrialization

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Capital Investment and Long ROI

- 3.2.2.2 Shortage of Skilled Labor and Technicians

- 3.2.3 Opportunities

- 3.2.3.1 Untapped Markets in Emerging Economies

- 3.2.3.2 Convergence of Physical and Digital Play (STEAM)

- 3.2.3.3 Green Manufacturing & Energy-Efficient Equipment

- 3.2.3.4 Reshoring and Near-shoring of Supply Chains

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Hydraulic Presses

- 5.3 Mechanical Presses

- 5.4 Rolling Machines

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automotive

- 6.3 Aerospace & Defense

- 6.4 Construction

- 6.5 Electronics

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Automation level, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Fully Automated Equipment

- 7.3 Semi Automated Equipment

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.3 Offline

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 TRUMPF Group

- 10.2 Amada Co., Ltd.

- 10.3 Schuler AG

- 10.4 JIER Machine-Tool Group

- 10.5 DMG Mori

- 10.6 AIDA Engineering

- 10.7 Komatsu Ltd.

- 10.8 Fagor Arrasate

- 10.9 Haas Automation

- 10.10 BYSTRONIC

- 10.11 Mitsubishi HI Machine Tool

- 10.12 Cincinnati Incorporated

- 10.13 LVD Group

- 10.14 MAG IAS

- 10.15 Bliss-Bret Industries

- 10.16 WardJet

- 10.17 Prima Industrie

- 10.18 Salvagnini

- 10.19 Ermaksan

- 10.20 Hyundai Rotem

多功能三轴搅拌机市场:依功能、搅拌技术、容量范围、设计类型、驱动机构和终端用户产业划分-全球预测,2026-2032年辊压成型机及生产线市场:依材料、机器类型、控制技术及最终用户划分,全球预测,2026-2032年全球辊压成型系统市场(按产品类型、材料类型、机器类型、驱动类型、运行速度和最终用途产业划分)预测(2026-2032年)OLED层压机市场:按产品、技术、基板材料、基材和终端用户产业划分,全球预测,2026-2032年液压卷材扩径成型机市场(按机器类型、卷材厚度、卷材宽度、技术、应用和终端用户行业划分),全球预测,2026-2032年冷轧成型机械市场:依机器类型、原料、应用、最终用户、产能和控制系统划分,全球预测(2026-2032年)按机器类型、材料厚度、产能、自动化程度、辊道工位数量和最终用途行业分類的全球自动辊压成型机械市场预测(2026-2032年)线材压扁机市场按产品类型、材料、技术、产能和最终用途划分,全球预测(2026-2032)

多功能三轴搅拌机市场:依功能、搅拌技术、容量范围、设计类型、驱动机构和终端用户产业划分-全球预测,2026-2032年辊压成型机及生产线市场:依材料、机器类型、控制技术及最终用户划分,全球预测,2026-2032年全球辊压成型系统市场(按产品类型、材料类型、机器类型、驱动类型、运行速度和最终用途产业划分)预测(2026-2032年)OLED层压机市场:按产品、技术、基板材料、基材和终端用户产业划分,全球预测,2026-2032年液压卷材扩径成型机市场(按机器类型、卷材厚度、卷材宽度、技术、应用和终端用户行业划分),全球预测,2026-2032年冷轧成型机械市场:依机器类型、原料、应用、最终用户、产能和控制系统划分,全球预测(2026-2032年)按机器类型、材料厚度、产能、自动化程度、辊道工位数量和最终用途行业分類的全球自动辊压成型机械市场预测(2026-2032年)线材压扁机市场按产品类型、材料、技术、产能和最终用途划分,全球预测(2026-2032) 数控卷材成型及展宽机:全球市占率及排名、总收入及需求预测(2025-2031年)

数控卷材成型及展宽机:全球市占率及排名、总收入及需求预测(2025-2031年) 2025-2029年全球辊压成型机市场

2025-2029年全球辊压成型机市场