|

市场调查报告书

商品编码

1913286

离心式帮浦市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Centrifugal Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

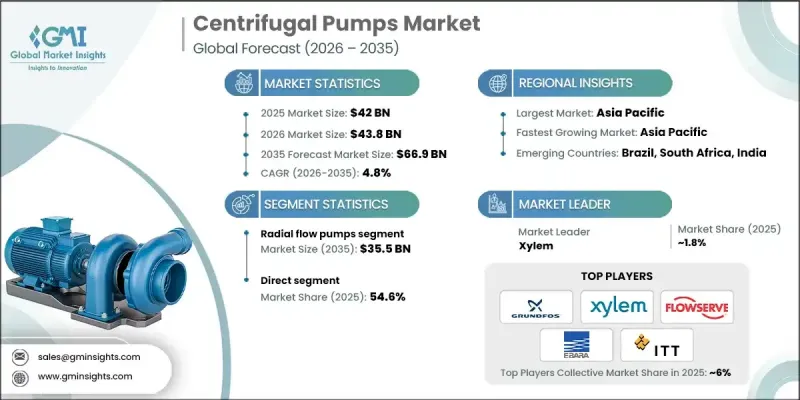

全球离心式帮浦市场预计到 2025 年将达到 420 亿美元,到 2035 年将达到 669 亿美元,年复合成长率为 4.8%。

全球城市化进程的加速和工业活动的扩张显着提升了对可靠流体输送解决方案的需求。全球水资源日益紧张,推动了高效水处理、再利用和净化系统的发展,而离心式帮浦仍是这些系统的核心部件。监管机构对永续性和资源效率的重视将进一步推动长期需求,因为各行业都在寻求合规且节能的泵送解决方案。同时,能源生产和加工基础设施的持续成长也维持了对高容量、高可靠性泵送系统的需求。离心式帮浦在采矿、加工和配送等环境中发挥至关重要的作用,为流体输送作业提供支援。随着产量的增加和运作的重要性日益凸显,泵浦的可靠性和效率也变得越来越重要。製造商正受益于持续的资本投资,这些投资旨在升级基础设施、提高营运韧性并优化生命週期性能。这些因素共同创造了一个稳定的需求环境,使离心式帮浦成为全球工业和市政系统中不可或缺的资产。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 420亿美元 |

| 预测金额 | 669亿美元 |

| 复合年增长率 | 4.8% |

预计到 2025 年,辐流泵市场规模将达到 223 亿美元,到 2035 年将达到 355 亿美元。径流泵能够在可控的流量下提供持续的压力,因此在需要稳定运行性能的製程中得到广泛应用。

到2025年,销售管道将达到230亿美元,占市场份额的54.6%。直接参与能够促进製造商和终端用户之间的更紧密合作,从而实现系统优化、更快解决问题,并透过直接获取技术专长和原厂配件来改善生命週期管理。

美国离心式帮浦市场预计到 2025 年将达到 82 亿美元,从 2026 年到 2035 年的复合年增长率为 4.8%。持续的大规模基础设施投资和现代化计画正在推动对先进泵送系统的需求,以支持全国范围内高效的水资源和公共产业管理。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 价格趋势

- 按地区和泵浦类型

- 原料成本

- 原料供应中现实与认知之间的差距

- 检验供应商价格上涨情况

- 法律规范

- 按地区

- 贸易统计

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 产品系列基准测试

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按泵浦类型分類的市场估算与预测,2022-2035年

- 轴流泵

- 混流泵

- 辐流泵

第六章 2022-2035年依设计分類的市场估算与预测

- 水平离心式帮浦

- 立式离心式帮浦

第七章 按类型分類的市场估计与预测,2022-2035年

- 可携式的

- 固定类型

第八章 2022-2035年各阶段市场估算与预测

- 单级泵浦

- 多级泵浦

第九章 2022-2035年各细分市场的估计与预测

- 电动帮浦

- 引擎驱动帮浦

第十章 依最终用途产业分類的市场估计与预测,2022-2035年

- 矿业

- 建筑/施工

- 石油和天然气

- 一般工业

- 水和污水处理

- 化学品

- 发电

- 其他(农业等)

第十一章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接

第十二章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

第十三章:公司简介

- Andritz AG

- Ebara Corporation

- Flowserve Corporation

- Grundfos

- ITT Inc.

- Kirloskar Brothers Limited

- KSB Group

- Pentair PLC

- Shakti Pumps(India)Ltd.

- SPX Flow, Inc.

- Sulzer Ltd.

- Torishima Pump Manufacturing Co., Ltd.

- Weir Group PLC

- Wilo SE

- Xylem Inc.

The Global Centrifugal Pumps Market was valued at USD 42 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 66.9 billion by 2035.

Accelerating urban development and expanding industrial activity worldwide significantly increase the demand for reliable fluid movement solutions. Rising pressure on global water resources strengthens the need for efficient water handling, reuse, and treatment systems, where centrifugal pumps remain a core component. Regulatory emphasis on sustainability and resource efficiency further supports long-term demand as industries seek compliant and energy-efficient pumping solutions. In parallel, continued growth in energy production and processing infrastructure sustains the requirement for high-capacity and high-reliability pump systems. Centrifugal pumps play a critical role in supporting fluid transfer operations across extraction, processing, and distribution environments. As production volumes rise and operational uptime becomes increasingly important, pump reliability and efficiency gain strategic importance. Manufacturers benefit from steady capital investments aimed at upgrading infrastructure, improving operational resilience, and optimizing lifecycle performance. These combined factors create a consistent demand environment, positioning centrifugal pumps as essential assets across global industrial and municipal systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $42 Billion |

| Forecast Value | $66.9 Billion |

| CAGR | 4.8% |

The radial flow pumps segment generated USD 22.3 billion in 2025 and is projected to reach USD 35.5 billion by 2035. Their ability to deliver sustained pressure at controlled flow rates supports widespread adoption in processes that require consistent operational performance.

The direct sales channel reached USD 23 billion in 2025 and holds 54.6% share. Direct engagement enables closer collaboration between manufacturers and end users, supporting system optimization, faster issue resolution, and improved lifecycle management through direct access to technical expertise and original components.

U.S. Centrifugal Pumps Market garnered USD 8.2 billion in 2025 and is expected to grow at a CAGR of 4.8% between 2026 and 2035. Large-scale infrastructure investment and modernization initiatives continue to drive demand for advanced pumping systems that support efficient water and utility management nationwide.

Key companies operating in the Global Centrifugal Pumps Market include Grundfos, Flowserve Corporation, Sulzer Ltd., Xylem Inc., KSB Group, ITT Inc., Ebara Corporation, Andritz AG, Wilo SE, Pentair PLC, SPX Flow, Inc., Weir Group PLC, Kirloskar Brothers Limited, Torishima Pump Manufacturing Co., Ltd., and Shakti Pumps (India) Ltd. Companies strengthen their position through continuous product innovation, energy-efficiency improvements, and expanded service offerings. Many manufacturers invest in digital monitoring, predictive maintenance solutions, and smart pump technologies to enhance operational reliability. Expanding global manufacturing footprints and localized service networks improves responsiveness and reduces downtime for customers. Strategic partnerships and long-term service agreements support customer retention and recurring revenue streams. Firms also focus on material advancements and modular designs to address diverse operating conditions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Pump type trends

- 2.2.3 Design trends

- 2.2.4 Type trends

- 2.2.5 Stage trends

- 2.2.6 Operation trends

- 2.2.7 End use industry trends

- 2.2.8 Distribution channel trends

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

- 2.5 Strategic recommendations

- 2.5.1 Supply chain diversification strategy

- 2.5.2 Product portfolio enhancement

- 2.5.3 Partnership and alliance opportunities

- 2.5.4 Cost management and pricing strategy

- 2.6 Decision framework

- 2.6.1 Investment priority matrix

- 2.6.2 ROI analysis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Price trends

- 3.5.1 By region and pump type

- 3.5.2 Raw material cost

- 3.5.3 Real vs. perceived capacity constraints in supply of raw materials

- 3.5.4 Supplier price increase validation

- 3.6 Regulatory framework

- 3.6.1 By Region

- 3.7 Trade statistics

- 3.7.1 Major importing countries

- 3.7.2 Major exporting countries

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Product portfolio benchmarking

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New Product Launches

- 4.7.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Pump Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Axial flow pump

- 5.3 Mixed flow pump

- 5.4 Radial flow pump

Chapter 6 Market Estimates & Forecast, By Design, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Horizontal centrifugal pump

- 6.3 Vertical centrifugal pump

Chapter 7 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Portable

- 7.3 Stationary

Chapter 8 Market Estimates & Forecast, By Stage, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Single-stage pump

- 8.3 Multi-stage pump

Chapter 9 Market Estimates & Forecast, By Operation, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Electric-driven pump

- 9.3 Engine-driven pump

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Mining

- 10.3 Building & construction

- 10.4 Oil & gas

- 10.5 General industries

- 10.6 Water & wastewater treatment

- 10.7 Chemicals

- 10.8 Power generation

- 10.9 Others (agriculture etc.)

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 U.K.

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 13.1 Andritz AG

- 13.2 Ebara Corporation

- 13.3 Flowserve Corporation

- 13.4 Grundfos

- 13.5 ITT Inc.

- 13.6 Kirloskar Brothers Limited

- 13.7 KSB Group

- 13.8 Pentair PLC

- 13.9 Shakti Pumps (India) Ltd.

- 13.10 SPX Flow, Inc.

- 13.11 Sulzer Ltd.

- 13.12 Torishima Pump Manufacturing Co., Ltd.

- 13.13 Weir Group PLC

- 13.14 Wilo SE

- 13.15 Xylem Inc.

全球离心式帮浦市场按类型、级数、运作方式、最终用户和地区划分-预测至2030年

全球离心式帮浦市场按类型、级数、运作方式、最终用户和地区划分-预测至2030年 2026年全球离心式帮浦市场报告

2026年全球离心式帮浦市场报告 离心式帮浦市场 - 全球产业规模、份额、趋势、机会和预测:按类型、叶轮类型、运行类型、级数、最终用户、地区和竞争格局划分,2021-2031年

离心式帮浦市场 - 全球产业规模、份额、趋势、机会和预测:按类型、叶轮类型、运行类型、级数、最终用户、地区和竞争格局划分,2021-2031年 离心式帮浦市场规模、份额和成长分析(按类型、设计、最终用途产业和地区划分)-2026-2033年产业预测

离心式帮浦市场规模、份额和成长分析(按类型、设计、最终用途产业和地区划分)-2026-2033年产业预测 立式多级离心式帮浦:全球市占率及排名、总收入及需求预测(2025-2031年)引擎驱动离心式帮浦:全球市占率和排名、总销售额和需求预测(2025-2031 年)

立式多级离心式帮浦:全球市占率及排名、总收入及需求预测(2025-2031年)引擎驱动离心式帮浦:全球市占率和排名、总销售额和需求预测(2025-2031 年) 双吸泵市场按终端用户行业划分 - 全球预测(2025-2032 年)离心式帮浦市场:按泵类型、材质、流量、压力范围和最终用途行业划分 - 2025-2032 年全球预测

双吸泵市场按终端用户行业划分 - 全球预测(2025-2032 年)离心式帮浦市场:按泵类型、材质、流量、压力范围和最终用途行业划分 - 2025-2032 年全球预测 全球自离心帮浦离心帮浦市场

全球自离心帮浦离心帮浦市场 离心泵市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:按阶段、设计、营运类型、类型、最终用户和地理划分

离心泵市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:按阶段、设计、营运类型、类型、最终用户和地理划分