|

市场调查报告书

商品编码

1913293

IT资产处置市场机会、成长要素、产业趋势分析及预测(2026-2035年)IT Asset Disposition (ITAD) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

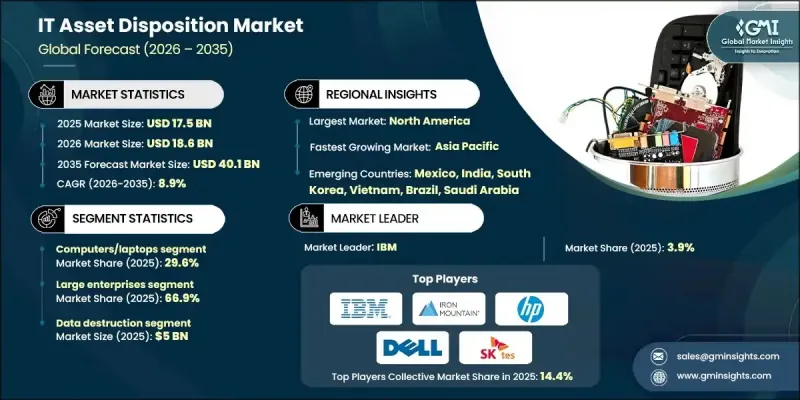

全球 IT 资产处置 (ITAD) 市场预计到 2025 年将达到 175 亿美元,到 2035 年将达到 401 亿美元,年复合成长率为 8.9%。

全球电子废弃物数量的不断增长推动了这个市场的扩张,电子垃圾问题已成为企业和政府面临的紧迫挑战。过去,废弃的IT设备往往最终被掩埋,造成严重的环境问题。如今,电信、金融、製造、媒体和政府等行业的机构越来越倾向于回收、翻新和转售废弃的IT资产。这种转变为ITAD(资讯科技资产处置)服务提供者创造了巨大的机会,帮助他们帮助企业实现永续性和净零排放目标。随着企业社会责任(CSR)日益受到重视,企业也逐渐意识到负责任地管理废弃电子产品的重要性。透过采用经认证的ITAD流程,企业可以确保资料安全擦除、减少环境影响、满足不断变化的监管要求,同时也能从回收的资产中获得潜在收益。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 175亿美元 |

| 预测金额 | 401亿美元 |

| 复合年增长率 | 8.9% |

到2025年,电脑和笔记型电脑市场将占29.6%的份额,创造52亿美元的收入。这些设备的平均使用寿命为3至8年,因此对ITAD服务有持续的需求。云端运算的普及和资料中心的扩张进一步增加了需要安全处置、回收或翻新的设备数量。这一趋势为拥有区域或本地营运的ITAD服务供应商带来了强劲的成长前景。

到2025年,大型企业将占据66.9%的市场份额,这主要得益于其在多个地点管理的庞大IT设备数量。人工智慧、云端运算和其他新兴技术推动的频繁硬体更新换代,每年都会产生大量废弃资产。大型企业依赖经过认证的ITAD服务来遵守GDPR、HIPAA和ESG标准等法规,降低资料外洩风险,并履行环境义务。

预计2025年,美国IT资产处分(ITAD)市场规模将达53亿美元。推动市场成长的主要因素包括:大型企业对IT的高需求、频繁的技术升级以及严格的法规环境。在政府推行企业社会责任(CSR)和永续性政策的支持下,企业正积极采用经认证的ITAD服务,以确保资料安全擦除和环保回收。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 电子废弃物产生量呈上升趋势

- 安全资料抹除的需求日益增长

- 云端采用率不断提高和资料中心整合

- 回收和翻新的IT资产的需求日益增长

- 产业潜在风险与挑战

- 全球公司复杂的逆向物流

- 发展中地区回收基础建设有限

- 市场机会

- 对永续回收解决方案的需求日益增长

- 在新兴市场拓展ITAD服务

- 资料中心退役创造新机会

- 扩大与原始设备製造商和云端服务供应商的合作关係

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国的资料保护与电子废弃物法规

- 加拿大个人资讯保护与电子文件法

- 欧洲

- 一般资料保护规则(GDPR)

- 欧盟废弃电子电气设备指令(WEEE)

- ISO/IEC 27001 和 EN 标准

- 亚太地区

- 中国个人资讯保护法(PIPL)

- 日本个人资讯保护法(APPI)

- 印度的《资讯科技法》、《资料保护规则》和《电子废弃物(管理)规则》

- 拉丁美洲

- 巴西通用资料保护法(LGPD)

- 墨西哥个人资讯保护法(LFPDPPP)

- 中东和非洲

- 阿联酋个人资料保护法及危险废弃物及电子废弃物管理条例

- 南非的《个人资讯保护法》(POPIA) 和当地电子废弃物标准

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过服务

- 成本細項分析

- 永续性和环境影响

- 环境影响评估

- 社会影响力和社区服务

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 碳足迹考量

- 案例研究

- 未来前景与机会

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依资产类型分類的市场估算与预测,2022-2035年

- 电脑/笔记型电脑

- 智慧型手机和平板电脑

- 周边设备

- 贮存

- 伺服器

- 其他的

第六章 依公司规模分類的市场估计与预测,2022-2035年

- 小型企业

- 大公司

第七章 按服务分類的市场估计与预测,2022-2035年

- 资料清除

- 逆向物流

- 再行销

- 恢復价值

- 拆卸和拆除处理

- 回收利用

- 物流管理

- 其他的

第八章 依实施类型分類的市场估算与预测,2022-2035年

- 现场 ITAD 服务

- 异地/设施内ITAD

第九章 2022-2035年各通路市场估算与预测

- 直接销售(OEM 直接面向客户)

- 第三方ITAD提供者

第十章 2022-2035年各产业市场估计与预测

- BFSI

- 资讯科技/通讯

- 政府

- 能源与公共产业

- 卫生保健

- 媒体与娱乐

- 其他的

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 新加坡

- 马来西亚

- 印尼

- 越南

- 泰国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 世界公司

- Iron Mountain

- Sims Lifecycle

- Dell

- HP

- IBM

- SK Tes

- Park Place Technologies

- Ingram Micro

- ERI

- Arrow Electronics

- Apto Solutions

- CompuCom Systems

- LifeSpan

- Blancco Technology

- EPC Global Solutions

- 本地公司

- Quantum Lifecycle Partners

- Securis

- Sage Sustainable Electronics

- Wisetek

- Vyta

- GreenTek

- DMD Systems Recovery

- Excess Logic

- Technimove

- 新兴企业

- ITAMG

- Hummingbird International

- CloudBlue

- DataServ

- Dynamic Lifecycle Innovations

The Global IT Asset Disposition (ITAD) Market was valued at USD 17.5 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 40.1 billion by 2035.

The expansion of this market is fueled by the rising volume of e-waste worldwide, which has become a pressing concern for businesses and governments alike. In the past, discarded IT equipment often ended up in landfills, creating significant environmental challenges. Today, organizations are increasingly turning to recycling, refurbishing, and reselling of retired IT assets across industries such as telecommunications, finance, manufacturing, media, and government. This shift has created a substantial opportunity for ITAD providers to support companies in achieving their sustainability and net-zero emission goals. Corporate social responsibility is emerging as a priority, with businesses recognizing the value of responsibly managing retired electronics. By adopting certified ITAD processes, companies can ensure secure data destruction, reduce environmental impact, and meet evolving regulatory requirements while generating potential revenue from recovered assets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.5 Billion |

| Forecast Value | $40.1 Billion |

| CAGR | 8.9% |

The computers and laptops segment held a 29.6% share in 2025, generating USD 5.2 billion. With an average lifespan of three to eight years, these assets create recurring demand for ITAD services. Growing cloud adoption and data center expansion further increase the volume of equipment requiring secure disposal, recycling, or refurbishment. This trend supports strong growth prospects for ITAD providers with local or regional operations.

The large enterprises segment held a 66.9% share in 2025, driven by the sheer volume of IT devices managed across multiple locations. Frequent hardware upgrades prompted by AI, cloud computing, and other emerging technologies result in significant volumes of retired assets annually. Large organizations rely on certified ITAD services to comply with regulations such as GDPR, HIPAA, and ESG standards, mitigate data breach risks, and meet environmental obligations.

U.S. IT Asset Disposition (ITAD) Market reached USD 5.3 billion in 2025. Growth is driven by the concentration of large companies with high IT demands, frequent technology upgrades, and a strong regulatory environment. Companies are adopting certified ITAD services for secure data destruction and environmentally responsible recycling, supported by government policies promoting corporate social responsibility and sustainability.

Leading players in the Global IT Asset Disposition (ITAD) Market include IBM, Dell, Iron Mountain, HP, SK Tes, Sims Lifecycle, LifeSpan, Park Place Technologies, Technimove, and Apto Solutions. Companies in the IT Asset Disposition (ITAD) Market strengthen their position through several strategic approaches. They invest in certified processes and secure data destruction services to build trust with large enterprises and comply with global regulations. Expanding geographic presence and establishing regional hubs ensure timely service delivery and support international clients. Firms also focus on technology-enabled tracking systems, reporting tools, and automated logistics to improve operational efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Asset

- 2.2.3 Enterprise Size

- 2.2.4 Services

- 2.2.5 Deployment

- 2.2.6 Channel

- 2.2.7 Industry Vertical

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising volume of e-waste generation

- 3.2.1.2 Increasing need for secure data destruction

- 3.2.1.3 Growth of cloud adoption and data center consolidation

- 3.2.1.4 Growing demand for value recovery & refurbished IT assets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex reverse logistics for global enterprises

- 3.2.2.2 Limited recycling infrastructure in developing regions

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable recycling solutions

- 3.2.3.2 Expansion of ITAD services in emerging markets

- 3.2.3.3 Rising opportunities in data center decommissioning

- 3.2.3.4 Increasing partnerships with OEMs & cloud providers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. data protection and e-waste rules

- 3.4.1.2 Canadian Personal Information Protection and Electronic Documents Act

- 3.4.2 Europe

- 3.4.2.1 EU General Data Protection Regulation (GDPR)

- 3.4.2.2 EU Waste Electrical and Electronic Equipment (WEEE)

- 3.4.2.3 ISO/IEC 27001 and EN standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China’s Personal Information Protection Law (PIPL)

- 3.4.3.2 Japan’s Act on the Protection of Personal Information (APPI)

- 3.4.3.3 India’s IT Act, data protection rules, and E-waste (Management) Rules

- 3.4.4 Latin America

- 3.4.4.1 Brazil’s General Data Protection Law (LGPD)

- 3.4.4.2 Mexico’s data protection law (LFPDPPP)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE personal data protection law and hazardous/e-waste regulations

- 3.4.5.2 South Africa’s POPIA and local e-waste standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By service

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.10.5 Carbon footprint considerations

- 3.11 Case Studies

- 3.12 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Asset, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Computers/Laptops

- 5.3 Smartphones and Tablets

- 5.4 Peripherals

- 5.5 Storages

- 5.6 Servers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 SMEs

- 6.3 Large enterprises

Chapter 7 Market Estimates & Forecast, By Services, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Data Destruction

- 7.3 Reverse Logistics

- 7.4 Remarketing

- 7.5 Value Recovery

- 7.6 De-Manufacturing

- 7.7 Recycling

- 7.8 Logistics Management

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Deployment, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Onsite ITAD Services

- 8.3 Offsite / Facility-Based ITAD

Chapter 9 Market Estimates & Forecast, By Channel, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Direct (OEM to Client)

- 9.3 Third-Party ITAD Providers

Chapter 10 Market Estimates & Forecast, By Industry Vertical, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 BFSI

- 10.3 IT & Telecom

- 10.4 Government

- 10.5 Energy and Utilities

- 10.6 Healthcare

- 10.7 Media and Entertainment

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Iron Mountain

- 12.1.2 Sims Lifecycle

- 12.1.3 Dell

- 12.1.4 HP

- 12.1.5 IBM

- 12.1.6 SK Tes

- 12.1.7 Park Place Technologies

- 12.1.8 Ingram Micro

- 12.1.9 ERI

- 12.1.10 Arrow Electronics

- 12.1.11 Apto Solutions

- 12.1.12 CompuCom Systems

- 12.1.13 LifeSpan

- 12.1.14 Blancco Technology

- 12.1.15 EPC Global Solutions

- 12.2 Regional companies

- 12.2.1 Quantum Lifecycle Partners

- 12.2.2 Securis

- 12.2.3 Sage Sustainable Electronics

- 12.2.4 Wisetek

- 12.2.5 Vyta

- 12.2.6 GreenTek

- 12.2.7 DMD Systems Recovery

- 12.2.8 Excess Logic

- 12.2.9 Technimove

- 12.3 Emerging companies

- 12.3.1 ITAMG

- 12.3.2 Hummingbird International

- 12.3.3 CloudBlue

- 12.3.4 DataServ

- 12.3.5 Dynamic Lifecycle Innovations

IT资产处置市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、最终用户及解决方案划分

IT资产处置市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、最终用户及解决方案划分 2026年全球企业IT资产处置市场报告

2026年全球企业IT资产处置市场报告 2026-2030年全球IT资产处分(ITAD)市场

2026-2030年全球IT资产处分(ITAD)市场 全球IT资产处置市场规模、份额、趋势和成长分析报告(2026-2034年)

全球IT资产处置市场规模、份额、趋势和成长分析报告(2026-2034年) IT资产再利用市场-全球产业规模、份额、趋势、机会及预测(依产品类型、组织规模、垂直市场、地区及竞争格局划分,2021-2031年)IT资产处置市场-全球产业规模、份额、趋势、机会、预测:按资产类型、最终用途、地区和竞争格局划分,2021-2031年

IT资产再利用市场-全球产业规模、份额、趋势、机会及预测(依产品类型、组织规模、垂直市场、地区及竞争格局划分,2021-2031年)IT资产处置市场-全球产业规模、份额、趋势、机会、预测:按资产类型、最终用途、地区和竞争格局划分,2021-2031年 IT资产迁移市场:2026-2032年全球预测(依资产类型、服务模式、公司规模及产业划分)

IT资产迁移市场:2026-2032年全球预测(依资产类型、服务模式、公司规模及产业划分) 日本IT资产处置市场报告:依服务、资产类型、公司规模、产业及地区划分(2026-2034年)

日本IT资产处置市场报告:依服务、资产类型、公司规模、产业及地区划分(2026-2034年) IT资产处置市场规模、份额和成长分析(按资产类型、服务、组织规模、最终用户产业和地区划分)-2026-2033年产业预测企业IT资产处置市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测

IT资产处置市场规模、份额和成长分析(按资产类型、服务、组织规模、最终用户产业和地区划分)-2026-2033年产业预测企业IT资产处置市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测