|

市场调查报告书

商品编码

1913305

萘市场机会、成长要素、产业趋势分析及2026年至2035年预测Naphthalene Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

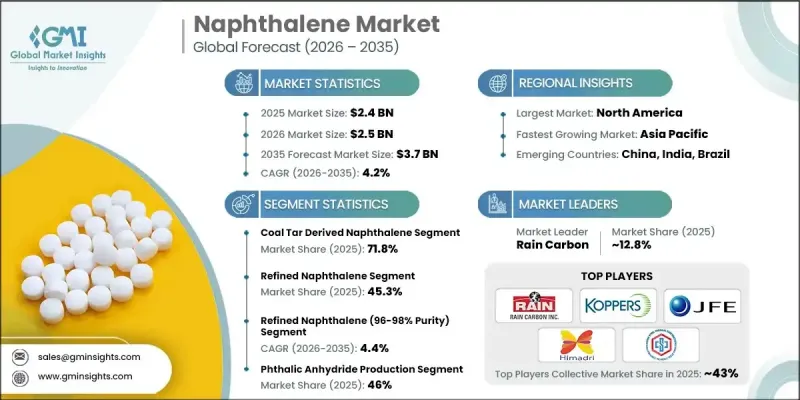

全球萘市场预计到 2025 年将达到 24 亿美元,到 2035 年将达到 37 亿美元,年复合成长率为 4.2%。

萘(化学式:CH)是一种多环芳烃,主要透过煤焦油加工和石油炼製生产。其商业供应形式多样,包括精製萘、烷基萘和固体萘,纯度从90-95%的麤品到99%以上的纯度不等。萘广泛用作化工生产链的核心原料、建筑组合药物以及成熟的工业应用。邻邻苯二甲酐需求的成长、建筑化学品应用的扩展以及特种化学品应用的发展,共同推动了全球市场的扩张。生产商致力于清洁生产流程、精密精炼系统和差异化产品等级,以满足不断变化的客户需求。加工效率和稳定性的提高,支撑了多个终端使用者产业和地区稳定的需求。不断增长的需求、技术的进步和多样化的应用,将继续支撑萘市场的长期发展。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 24亿美元 |

| 预测金额 | 37亿美元 |

| 复合年增长率 | 4.2% |

精炼和品位控制技术的进步正在重塑高纯度萘的生产方式。如今,无论是煤焦油原料或石油衍生原料,都能获得纯度超过99%的高纯度萘,满足高性能应用的需求。这得归功于更严格的结晶控制和批次间一致性的提升。这些进步旨在满足高价值化学合成和中间体生产所需的严格品质标准。先进的蒸馏技术、改良的结晶製程和基于氢化的製程在降低杂质含量的同时,提高了功能可靠性,使製造商能够提供性能更可预测、更容易被工业界接受的萘产品。

2025年,煤焦油衍生萘市占率占比高达71.8%,预计2026年至2035年将以4%的复合年增长率持续成长。其市场主导地位主要归功于与钢铁和焦化製程相衔接的成熟生产系统、良好的经济效益以及稳定的产品品质。这项原材料来源受益于全球广泛的煤焦油基础设施,该基础设施支持大规模生产,同时保持了成本效益和供应稳定性。在主要消费地区拥有稳固的地位,并长期融入产业价值链,这些因素不断巩固了其在全球萘市场的主导地位。

2025年,精製萘市占率占比达45.3%,预计到2035年将以3.6%的复合年增长率成长。由于其纯度稳定、操作性能优异,精製萘仍是大宗化学品加工的首选原料。其在综合性化工生产设施中的广泛应用,有助于高效的下游加工和可靠的运作性能。其完善的生产网络和显着的经济优势,使其在全球化学品生产领域中持续占据主导地位。

预计到2025年,美国萘市场规模将达到9.299亿美元,反映了强劲的区域需求,而工业和建筑相关行业的稳定消费则支撑了这一需求。成熟的生产设施、完善的加工基础设施以及持续的终端用户需求,共同支撑了国内市场的稳定性。持续投资于提高加工效率和供应链可靠性,将继续为北美地区的需求成长奠定基础。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品等级

- 未来市场趋势

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 精製萘

- 烷基萘

- 萘固体

- 其他的

6. 2022-2035年按来源分類的市场估计与预测

- 萘来自煤焦油

- 石油衍生的萘

- 回收和再生材料

第七章 依产品等级分類的市场估算与预测,2022-2035年

- 粗萘(纯度90-95%)

- 精製萘(纯度96-98%)

- 纯萘(纯度99%以上)

- 特殊等级和客製化产品

第八章 按应用领域分類的市场估算与预测,2022-2035年

- 邻苯二甲酐的生产

- 表面活性剂和分散剂

- 减水剂(建筑化学品)

- 染料和颜料(化学中间体)

- 传统用途(驱虫剂、鞣革剂)

- 新兴及其他应用

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Atom Scientific

- CDH Fine Chemical

- China Steel Chemical

- Deza

- Dong-Suh Chemical Ind. Co., Ltd.

- ExxonMobil Chemical

- Himadri Specialty Chemical Ltd.

- JFE Chemical Corporation

- King Industries

- Koppers

- PCC Group

- Rain Carbon

- Tulstar Products

The Global Naphthalene Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 3.7 billion by 2035.

Naphthalene, chemically identified as C10H8, is a polycyclic aromatic hydrocarbon produced mainly through coal tar processing and petroleum refining. The material is supplied in multiple commercial forms such as refined naphthalene, alkyl naphthalene, and solid variants, with purity levels spanning from crude grades of 90-95% to high-purity grades exceeding 99%. It is widely used as a core feedstock in chemical manufacturing chains, construction-related formulations, and established industrial applications. Rising demand for phthalic anhydride, increasing use of construction chemicals, and the development of specialty chemical applications are collectively shaping market expansion worldwide. Producers are focusing on cleaner production routes, precision purification systems, and differentiated product grades to meet evolving customer specifications. Improvements in processing efficiency and consistency are supporting stable demand across multiple end-use industries and regions. This combination of demand growth, technology advancement, and diversified applications continues to support long-term development of the naphthalene market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 billion |

| Forecast Value | $3.7 billion |

| CAGR | 4.2% |

Technological progress in purification and grade control is reshaping naphthalene manufacturing by enabling purity levels above 99% for high-performance uses, tighter crystallization management, and improved batch consistency from both coal tar and petroleum-based sources. These advancements are designed to meet strict quality benchmarks required for high-value chemical synthesis and intermediate production. Enhanced distillation, crystallization refinement, and hydrogenation-based processes are lowering impurity content while improving functional reliability, allowing manufacturers to deliver naphthalene products with more predictable performance and broader industrial acceptance.

The coal tar-based naphthalene segment held 71.8% share in 2025 and is forecast to grow at a CAGR of 4% from 2026 to 2035. Its dominance is attributed to mature production systems aligned with steel and coke processing operations, favorable yield economics, and stable output quality. This source benefits from extensive global coal tar infrastructure that supports large-scale production while maintaining cost efficiency and dependable supply. Its strong foothold across major consuming regions, combined with long-standing integration into industrial value chains, continues to reinforce its leadership in the global naphthalene landscape.

The refined naphthalene segment accounted for 45.3% share in 2025 and is anticipated to register a CAGR of 3.6% through 2035. This form remains the preferred choice for large-volume chemical processing due to its consistent purity and favorable handling characteristics. Its widespread use within integrated chemical manufacturing facilities supports efficient downstream processing and reliable operational performance. Established production networks and proven economic advantages contribute to its continued dominance across global chemical production hubs.

US Naphthalene Market generated USD 929.9 million in 2025, reflecting strong regional demand driven by steady consumption across industrial and construction-related sectors. The presence of established production facilities, integrated processing infrastructure, and sustained end-use requirements supports market stability within the country. Ongoing investment in processing efficiency and supply chain reliability continues to underpin demand growth across North America.

Key companies active in the Naphthalene Market include Rain Carbon, Himadri Specialty Chemical Ltd., ExxonMobil Chemical, Koppers, PCC Group, China Steel Chemical, JFE Chemical Corporation, and Dong-Suh Chemical Ind. Co., Ltd., Deza, King Industries, Atom Scientific, CDH Fine Chemical, and Tulstar Products. Companies operating in the Naphthalene Market are strengthening their market position through capacity optimization, investment in advanced purification technologies, and expansion of high-purity product portfolios. Many players are focusing on operational integration with upstream raw material sources to improve cost control and supply security. Strategic partnerships and long-term supply agreements are being used to stabilize demand and enhance regional presence. Firms are also prioritizing process efficiency, emission reduction, and sustainable production practices to align with evolving regulatory expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Form

- 2.2.3 Product Grade

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product grade

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Refined naphthalene

- 5.3 Alkyl naphthalene

- 5.4 Naphthalene solid

- 5.5 Other

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Coal tar derived naphthalene

- 6.3 Petroleum derived naphthalene

- 6.4 Recycled and secondary sources

Chapter 7 Market Estimates and Forecast, By Product Grade, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Crude naphthalene (90-95% purity)

- 7.3 Refined naphthalene (96-98% purity)

- 7.4 Pure naphthalene (99%+ purity)

- 7.5 Specialty grades and custom products

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Phthalic anhydride production

- 8.3 Surfactants & dispersants

- 8.4 Water reducing agents (construction chemicals)

- 8.5 Dyes & pigments (chemical intermediates)

- 8.6 Traditional applications (mothballs, tanning agents)

- 8.7 Emerging and other applications

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Atom Scientific

- 10.2 CDH Fine Chemical

- 10.3 China Steel Chemical

- 10.4 Deza

- 10.5 Dong-Suh Chemical Ind. Co., Ltd.

- 10.6 ExxonMobil Chemical

- 10.7 Himadri Specialty Chemical Ltd.

- 10.8 JFE Chemical Corporation

- 10.9 King Industries

- 10.10 Koppers

- 10.11 PCC Group

- 10.12 Rain Carbon

- 10.13 Tulstar Products

环烷酸市场 - 全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年)

环烷酸市场 - 全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年) 溶剂石脑油(重芳烃)市场按类型、纯度等级、通路、终端用户行业和应用划分 - 全球预测 2026-2032

溶剂石脑油(重芳烃)市场按类型、纯度等级、通路、终端用户行业和应用划分 - 全球预测 2026-2032 环烷酸市场-2026-2031年预测

环烷酸市场-2026-2031年预测 萘市场规模、份额和趋势分析报告:按原材料、应用、地区和细分市场预测(2026-2033 年)

萘市场规模、份额和趋势分析报告:按原材料、应用、地区和细分市场预测(2026-2033 年) 萘市场规模、份额及成长分析(按来源、应用、最终用户和地区划分)-产业预测(2026-2033 年)

萘市场规模、份额及成长分析(按来源、应用、最终用户和地区划分)-产业预测(2026-2033 年) 2,6-二甲基萘:全球市占率及排名、总营收及需求预测(2025-2031年)全球甲醇烷基化萘市场规模:依等级、黏度指数、应用、地区和预测萘市场-全球产业规模、份额、趋势、机会及预测(按销售管道、最终用途、地区和竞争细分,2020-2030 年)

2,6-二甲基萘:全球市占率及排名、总营收及需求预测(2025-2031年)全球甲醇烷基化萘市场规模:依等级、黏度指数、应用、地区和预测萘市场-全球产业规模、份额、趋势、机会及预测(按销售管道、最终用途、地区和竞争细分,2020-2030 年) 2025-2033年环烷酸市场类型、应用、销售管道和地区报告

2025-2033年环烷酸市场类型、应用、销售管道和地区报告 萘:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

萘:市场占有率分析、产业趋势与统计、成长预测(2025-2030)