|

市场调查报告书

商品编码

1913340

物流领域机器学习市场机会、成长要素、产业趋势分析及2026年至2035年预测Machine Learning in Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球物流机器学习市场预计到 2025 年将达到 43 亿美元,到 2035 年将达到 445 亿美元,年复合成长率为 26.7%。

机器学习正在透过实现预测性决策、高级自动化和供应链网路的即时优化,变革物流业。数位商务的快速发展、对快速交付日益增长的期望,以及人工智慧和互联技术的不断进步,都在加速机器学习的普及应用。企业正在拓展机器学习的应用范围,以提高预测准确度、优化运输路线、提升仓储效率、调整存量基准、管理车队,并在设备故障发生前进行预测。随着物流生态系统的日益复杂,机器学习解决方案提供的扩充性、响应速度和营运视觉性是传统系统无法比拟的。这种变革有助于提高服务可靠性、降低成本并增强全球供应链的韧性,使机器学习成为未来物流的基础技术。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 43亿美元 |

| 预测金额 | 445亿美元 |

| 复合年增长率 | 26.7% |

先进的机器学习模型透过实现持续学习和营运自适应,显着提升了自动化物流系统的效能。企业越来越依赖智慧自动化来应对不断增长的订单量、严格的交货期限和频繁的运输週期。机器学习驱动的工作流程提高了准确性、效率和劳动生产力,同时满足了消费者对快速交付日益增长的期望。

预计到2025年,软体领域将占据64%的市场份额,并在2026年至2035年间以25.1%的复合年增长率成长。软体平台提供核心的机器学习功能,有助于预测、路线规划、资产利用率和维护计画。它们能够与现有的企业和仓库系统无缝集成,进一步增强了其优势。

到 2025 年,监督学习领域将占据 70% 的市场份额,到 2035 年将以 25.6% 的复合年增长率成长。这些模型利用历史资料来改善营运计划、需求预测和绩效预测,与传统方法相比,在准确性方面取得了可衡量的提升。

北美在物流机器学习市场中占据 32% 的份额,预计到 2035 年将以 22.4% 的复合年增长率成长。强大的数位基础设施、早期技术应用以及对物流创新的持续投资,巩固了该地区的领先地位。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 加强供应链营运优化

- 仓库自动化

- 电子商务领域的成长

- 改善客户体验的需求日益增长

- 物联网整合、即时追踪和先进的物流基础设施

- 产业潜在风险与挑战

- 数据品质和整合问题

- 与旧有系统的集成

- 市场机会

- 即时供应链可视性和动态优化

- 库存和供应链规划的预测分析和需求预测

- 仓库自动化、智慧仓库管理与机器人集成

- 运输资产的车队管理和预测性维护

- 成长潜力分析

- 监管环境

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利分析

- 用例和成功案例

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来前景与机会

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 按组件分類的市场估算与预测,2022-2035年

- 软体

- 服务

- 管理

- 面向专业人士

第六章 按技术分類的市场估计与预测,2022-2035年

- 监督式学习

- 无监督学习

第七章 依公司规模分類的市场估计与预测,2022-2035年

- 大公司

- 中小企业

第八章 按车型分類的市场估计与预测,2022-2035年

- 基于云端的

- 本地部署

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 库存管理

- 供应链规划

- 运输管理

- 仓库管理

- 车队管理

- 风险管理与安全

- 其他的

第十章 依最终用途分類的市场估计与预测,2022-2035年

- 零售与电子商务

- 製造业

- 卫生保健

- 车

- 食品/饮料

- 消费品

- 其他的

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 世界玩家

- Amazon Web Services

- DHL Supply Chain

- FedEx

- Google Cloud Platform(GCP)

- International Business Machines(IBM)

- Microsoft

- Oracle

- SAP SE

- Uber Technologies

- United Parcel Service

- 区域玩家

- Blue Yonder Group

- CH Robinson Worldwide

- Convoy

- Coupa Software

- Flexport

- Infor

- Locus Robotics

- Manhattan Associates

- Trimble

- 新兴科技创新者

- ClearMetal

- FourKites

- Project44

- Shipwell

- Waymo LLC

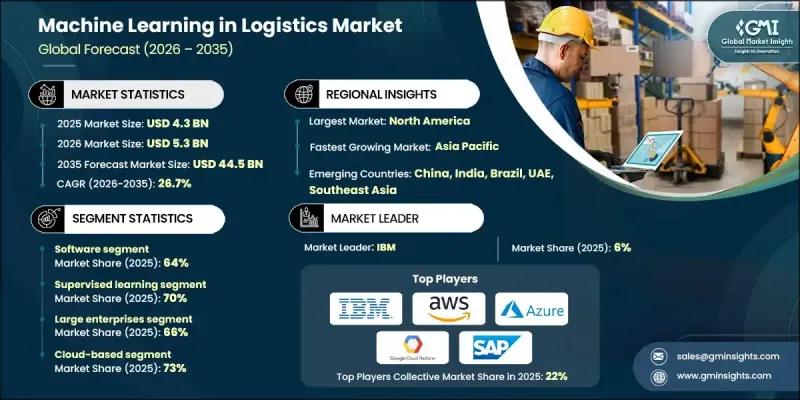

The Global Machine Learning in Logistics Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 26.7% to reach USD 44.5 billion by 2035.

Machine learning is transforming logistics by enabling predictive decision-making, advanced automation, and real-time optimization across supply chain networks. Rapid digital commerce expansion, rising expectations for faster deliveries, and continued progress in artificial intelligence and connected technologies are accelerating adoption. Organizations are increasingly applying machine learning to enhance forecasting accuracy, optimize transportation routes, improve warehouse efficiency, balance inventory levels, manage fleets, and anticipate equipment issues before disruptions occur. As logistics ecosystems become more complex, machine learning solutions provide scalability, responsiveness, and operational visibility that traditional systems cannot deliver. This evolution supports improved service reliability, reduced costs, and stronger resilience across global supply chains, positioning machine learning as a foundational technology for the future of logistics.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $44.5 Billion |

| CAGR | 26.7% |

Advanced machine learning models significantly improve the performance of automated logistics systems by enabling continuous learning and operational adaptation. Businesses increasingly rely on intelligent automation to handle higher order volumes, tighter delivery timelines, and frequent shipment cycles. Machine learning-driven workflows enhance accuracy, efficiency, and workforce productivity while supporting growing consumer expectations for rapid fulfillment.

The software segment held a 64% share in 2025 and is expected to grow at a CAGR of 25.1% from 2026 to 2035. Software platforms deliver core machine learning capabilities that support forecasting, routing, asset utilization, and maintenance planning. Their ability to integrate seamlessly with existing enterprise and warehouse systems reinforces their dominance.

The supervised learning segment held a 70% share in 2025 and is growing at a CAGR of 25.6% through 2035. These models leverage historical data to improve operational planning, demand estimation, and performance prediction, delivering measurable gains in accuracy compared to traditional approaches.

North America Machine Learning in Logistics Market held a 32% share and is forecast to grow at a CAGR of 22.4% through 2035. Strong digital infrastructure, early technology adoption, and sustained investment in logistics innovation support regional leadership.

Major companies operating in the Global Machine Learning in Logistics Market include SAP SE, Oracle, IBM, Microsoft Azure, Google Cloud Platform, Amazon Web Services, Blue Yonder, Manhattan Associates, DHL Supply Chain, and FedEx Corporation. Companies in the Global Machine Learning in Logistics Market strengthen their position through continuous innovation, platform integration, and strategic partnerships. Firms invest heavily in scalable cloud-based solutions that support real-time analytics and automation across supply chains. Focus on interoperability with existing enterprise systems to enhance adoption and customer retention. Many players prioritize advanced data security, predictive capabilities, and customizable solutions to meet diverse logistics requirements. Expansion into emerging markets, along with industry-specific applications, supports revenue growth.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technique

- 2.2.4 Organization Size

- 2.2.5 Deployment Model

- 2.2.6 Application

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Increased optimization of supply chain operations

- 3.2.1.3 Automation of warehousing operations

- 3.2.1.4 Growth of e-commerce sector

- 3.2.1.5 Rising need for enhanced customer experience

- 3.2.1.6 Integration with IoT, real-time tracking, and advanced logistic infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data quality and integration concern

- 3.2.2.2 Integration with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Real-time supply-chain visibility & dynamic optimization

- 3.2.3.2 Predictive analytics & demand forecasting for inventory and supply-chain planning

- 3.2.3.3 Warehouse automation, smart warehousing & robotics integration

- 3.2.3.4 Fleet management & predictive maintenance for transport assets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Use cases & success stories

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.3.1 Managed

- 5.3.2 Professional

Chapter 6 Market Estimates & Forecast, By Technique, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Supervised learning

- 6.3 Unsupervised learning

Chapter 7 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 Small and medium-sized enterprises (SMEs)

Chapter 8 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Cloud-based

- 8.3 On-premises

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Inventory management

- 9.3 Supply chain planning

- 9.4 Transportation management

- 9.5 Warehouse management

- 9.6 Fleet management

- 9.7 Risk management and security

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Retail and e-commerce

- 10.3 Manufacturing

- 10.4 Healthcare

- 10.5 Automotive

- 10.6 Food & beverage

- 10.7 Consumer goods

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Amazon Web Services

- 12.1.2 DHL Supply Chain

- 12.1.3 FedEx

- 12.1.4 Google Cloud Platform (GCP)

- 12.1.5 International Business Machines (IBM)

- 12.1.6 Microsoft

- 12.1.7 Oracle

- 12.1.8 SAP SE

- 12.1.9 Uber Technologies

- 12.1.10 United Parcel Service

- 12.2 Regional Players

- 12.2.1 Blue Yonder Group

- 12.2.2 C.H. Robinson Worldwide

- 12.2.3 Convoy

- 12.2.4 Coupa Software

- 12.2.5 Flexport

- 12.2.6 Infor

- 12.2.7 Locus Robotics

- 12.2.8 Manhattan Associates

- 12.2.9 Trimble

- 12.3 Emerging Technology Innovators

- 12.3.1 ClearMetal

- 12.3.2 FourKites

- 12.3.3 Project44

- 12.3.4 Shipwell

- 12.3.5 Waymo LLC

2025-2029年全球云端机器学习市场

2025-2029年全球云端机器学习市场 2025-2029年全球人工智慧与机器学习营运软体市场

2025-2029年全球人工智慧与机器学习营运软体市场 2025-2029年全球机器学习课程市场

2025-2029年全球机器学习课程市场 2025-2029年全球机器学习软体市场

2025-2029年全球机器学习软体市场 2025-2029年全球製药业机器学习展望

2025-2029年全球製药业机器学习展望 2025-2029年全球零售业机器学习趋势

2025-2029年全球零售业机器学习趋势 机器学习市场-全球产业规模、份额、趋势、机会及预测(按组件、公司规模、部署方式、最终用户、地区和竞争格局划分,2021-2031年)自动化机器学习解决方案市场-全球产业规模、份额、趋势、机会和预测:按产品、部署、自动化类型、公司规模、最终用户、地区和竞争格局划分,2021-2031年

机器学习市场-全球产业规模、份额、趋势、机会及预测(按组件、公司规模、部署方式、最终用户、地区和竞争格局划分,2021-2031年)自动化机器学习解决方案市场-全球产业规模、份额、趋势、机会和预测:按产品、部署、自动化类型、公司规模、最终用户、地区和竞争格局划分,2021-2031年 2026-2030年全球医疗、法律与监管(MLR)审查软体市场

2026-2030年全球医疗、法律与监管(MLR)审查软体市场 GPU加速器市场:2026-2032年全球预测(依产品类型、最终用户、记忆体容量和应用划分)

GPU加速器市场:2026-2032年全球预测(依产品类型、最终用户、记忆体容量和应用划分)