|

市场调查报告书

商品编码

1913352

聚羟基烷酯市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Polyhydroxyalkanoate (PHA) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

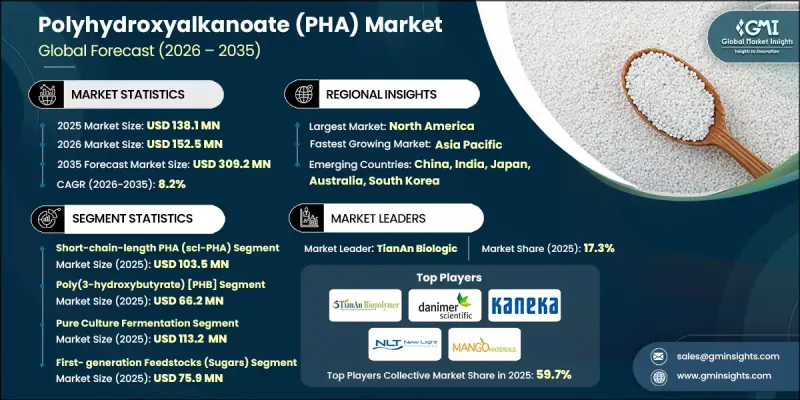

全球聚羟基烷酯(PHA)市场预计到 2025 年将达到 1.381 亿美元,到 2035 年将达到 3.092 亿美元,年复合成长率为 8.2%。

聚羟基脂肪酸酯(PHAs)是由微生物作为能量储存化合物产生的天然可生物降解聚合物。在碳过剩而营养匮乏的条件下,微生物合成的PHAs性质与传统塑胶非常相似。这些聚合物正逐渐成为石油基塑胶的环保且生物相容的替代品,在永续应用中发挥着至关重要的作用。发酵技术、基因工程的进步以及低成本原料的普及,使得PHAs的商业化生产在经济上成为可能,弥合了传统塑胶和可生物降解材料之间的差距。这项技术进步正在拓展PHAs的应用领域,包括包装、医疗保健、农业和消费品。 PHAs在土壤、淡水和海洋环境中的生物降解性有助于减少环境污染,而其可再生原料的使用则支持循环生物经济的发展。对永续材料日益增长的需求以及监管机构对减少塑胶废弃物的重视,正在推动市场接受度的提高,并鼓励进一步的创新。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 1.381亿美元 |

| 预测金额 | 3.092亿美元 |

| 复合年增长率 | 8.2% |

预计到2025年,短链聚羟基脂肪酸酯(scl-PHA)市场规模将达到1.035亿美元。 scl-PHA的高需求主要归功于其优异的机械强度、生物降解性和在包装、农业和兽医等领域的广泛应用。成熟的生产流程使其具有成本效益高、易于规模化生产的特点,使其成为希望减少塑胶废弃物的行业的首选解决方案。

预计到2025年,聚(3-羟基丁酸酯) [PHB] 市场规模将达到6,620万美元。 PHB及其共聚物,例如聚(3-羟基丁酸酯-共聚-3-羟基戊酸酯) (PHBV),因其优异的机械性能和生物降解性而备受关注。 PHB主要用于包装和农业薄膜,而PHBV的柔软性和韧性更佳,使其可应用于医疗设备和消费品领域。低廉的生产成本和稳定的需求预计将支撑这些聚合物的市场成长。

预计到2025年,北美聚羟基烷酯(PHAs)市场规模将达到3,860万美元。随着品牌越来越重视永续性,该地区对可再生和可生物降解材料的需求也不断增长。餐饮服务和消费品製造商日益增长的需求,以及强大的研发生态系统和发酵流程的中试优化,正在加速市场渗透。大型零售连锁店的兴趣也进一步推动了这一趋势。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对生物分解性塑胶的需求不断增长

- 微生物发酵技术的进步

- 终端用户产业的扩张

- 产业潜在风险与挑战

- 与化石基塑胶相比,生产成本高昂

- 与其他生质塑胶的竞争

- 市场机会

- 高性能PHA混合物

- 优质环保产品

- 融入循环经济

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依炼长分类

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估计与预测:依产业炼长度划分,2022-2035年

- 短链PHA(scl-PHA)

- 中链PHA(mcl-PHA)

- 长链PHA(lcl-PHA)

第六章 依共聚物类型分類的市场估计与预测,2022-2035年

- 聚(3-羟基丁酸酯) [PHB]

- 聚(3-羟基丁酸酯-共-3-羟基戊酸酯) [PHBV]

- 聚(3-羟基丁酸酯-共-4-羟基丁酸酯) [P3H4B]

- 聚(3-羟基丁酸酯-共-3-羟基己酸酯) [PHBH]

- 其他 PHA 共聚物 [P(3HB-co-3HP), P(3HB-co-LA)]

第七章 依生产方式分類的市场估算与预测,2022-2035年

- 纯培养发酵

- 混合微生物培养物(MMC)

- 嗜盐/极端微生物的生产

- 基因工程系统

第八章 依原料类型分類的市场估算与预测,2022-2035年

- 第一代原料(醣类)

- 第二代原料(植物油)

- 第三代原料(废物流)

- 下一代原料(CO2、CO、CH4、C1化合物)

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 包装应用

- 硬包装

- 柔性薄膜

- 其他的

- 生物医学应用

- 医疗设备

- 手术缝合线

- 其他的

- 农业用途

- 多卷胶片

- 种子披衣

- 其他的

- 光纤应用

- 纤维和线

- 不织布

- 其他的

- 消费品

- 化妆品包装

- 玩具和娱乐产品

- 其他的

- 其他工业应用

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十一章 公司简介

- Biomer

- Bluepha

- CJ BIO(CJ CheilJedang)

- Danimer Scientific

- Full Cycle Bioplastics

- Kaneka Corporation

- Mango Materials

- Newlight Technologies

- Paques Biomaterials

- PhaBuilder

- Phangel Biotechnology

- Tepha Inc.

- TianAn Biologic

- Tianjin Green-Bio

- Weining Biotechnology

- Yield10 Bioscience

The Global Polyhydroxyalkanoate (PHA) Market was valued at USD 138.1 million in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 309.2 million by 2035.

PHAs are naturally occurring biodegradable polymers produced by microorganisms as energy-storage compounds. Under conditions of excess carbon and limited nutrients, microorganisms synthesize PHAs with properties closely resembling conventional plastics. These polymers have emerged as eco-friendly and biocompatible alternatives to petroleum-based plastics, making them highly relevant for sustainable applications. Advances in fermentation, genetic engineering, and the use of low-cost feedstocks have made commercial-scale PHA production economically feasible, bridging the gap between traditional plastics and biodegradable options. This technological progress has expanded PHA applications across packaging, medical, agricultural, and consumer products. The ability of PHAs to biodegrade in soil, freshwater, and marine environments reduces environmental pollution, while renewable feedstock utilization supports a circular bioeconomy. Growing demand for sustainable materials and regulatory emphasis on reducing plastic waste are driving market adoption and encouraging further innovation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $138.1 Million |

| Forecast Value | $309.2 Million |

| CAGR | 8.2% |

The short-chain-length PHAs (scl-PHA) segment accounted for USD 103.5 million in 2025. The high demand for scl-PHAs stems from their mechanical strength, biodegradability, and versatility across sectors such as packaging, agriculture, and veterinary applications. Their established production methods make them cost-efficient and readily scalable, positioning them as a preferred solution for industries aiming to reduce plastic waste.

The poly(3-hydroxybutyrate) [PHB] segment reached USD 66.2 million in 2025. PHB and its copolymers, such as Poly(3-hydroxybutyrate-co-3-hydroxyvalerate) (PHBV), are gaining traction due to favorable mechanical properties and biodegradability. PHB is primarily used in packaging and agricultural films, while PHBV's enhanced flexibility and toughness enable applications in medical and consumer goods. The combination of low production costs and steady demand ensures sustained market growth for these polymers.

North America Polyhydroxyalkanoate (PHA) Market generated USD 38.6 million in 2025. The region is witnessing increased adoption of renewable and biodegradable materials as brands focus on sustainability. Rising demand from food-service and consumer goods manufacturers, coupled with robust R&D ecosystems and pilot-scale optimization of fermentation processes, is accelerating market penetration. Interest from major retail chains is further reinforcing adoption trends.

Key players in the Global Polyhydroxyalkanoate (PHA) Market include Biomer, Bluepha, CJ BIO (CJ CheilJedang), Danimer Scientific, Full Cycle Bioplastics, Kaneka Corporation, Mango Materials, Newlight Technologies, Paques Biomaterials, PhaBuilder, Phangel Biotechnology, Tepha Inc., TianAn Biologic, Tianjin Green-Bio, Weining Biotechnology, and Yield10 Bioscience. Companies in the Global Polyhydroxyalkanoate (PHA) Market are strengthening their presence by investing heavily in R&D to improve fermentation efficiency, reduce production costs, and enhance polymer properties. Strategic partnerships with research institutions and industrial stakeholders enable the co-development of application-specific products. Expanding production capacities, adopting low-cost and renewable feedstocks, and developing scalable commercial processes help increase market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Chain Length Classification

- 2.2.2 Copolymer Type

- 2.2.3 Production Method

- 2.2.4 Feedstock Type

- 2.2.5 Application

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for biodegradable plastics

- 3.2.1.2 Technological advancements in microbial fermentation

- 3.2.1.3 Expansion of end-use industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production cost compared to fossil-based plastics

- 3.2.2.2 Competition from other bioplastics

- 3.2.3 Market opportunities

- 3.2.3.1 High-performance PHA blends

- 3.2.3.2 Premium eco-friendly products

- 3.2.3.3 Circular economy integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By chain length classification

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Chain Length Classification, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Short-Chain-Length PHA (scl-PHA)

- 5.3 Medium-Chain-Length PHA (mcl-PHA)

- 5.4 Long-Chain-Length PHA (lcl-PHA)

Chapter 6 Market Estimates and Forecast, By Copolymer Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Poly(3-hydroxybutyrate) [PHB]

- 6.3 Poly(3-hydroxybutyrate-co-3-hydroxyvalerate) [PHBV]

- 6.4 Poly(3-hydroxybutyrate-co-4-hydroxybutyrate) [P3H4B]

- 6.5 Poly(3-hydroxybutyrate-co-3-hydroxyhexanoate) [PHBH]

- 6.6 Other PHA Copolymers [P(3HB-co-3HP), P(3HB-co-LA)]

Chapter 7 Market Estimates and Forecast, By Production Method, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Pure Culture Fermentation

- 7.3 Mixed Microbial Culture (MMC)

- 7.4 Halophilic/Extremophilic Production

- 7.5 Genetically Engineered Systems

Chapter 8 Market Estimates and Forecast, By Feedstock Type, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 First-Generation Feedstocks (Sugars)

- 8.3 Second-Generation Feedstocks (Vegetable Oils)

- 8.4 Third-Generation Feedstocks (Waste Streams)

- 8.5 Next-Generation Feedstocks (CO2, CO, CH4, C1 Compounds)

Chapter 9 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Packaging Applications

- 9.2.1 Rigid Packaging

- 9.2.2 Flexible Films

- 9.2.3 Others

- 9.3 Biomedical Applications

- 9.3.1 Medical Devices

- 9.3.2 Surgical Sutures

- 9.3.3 Others

- 9.4 Agricultural Applications

- 9.4.1 Mulch Films

- 9.4.2 Seed Coatings

- 9.4.3 Others

- 9.5 Textile Applications

- 9.5.1 Fibers & Yarns

- 9.5.2 Non-Wovens

- 9.5.3 Others

- 9.6 Consumer Goods

- 9.6.1 Cosmetic Packaging

- 9.6.2 Toys & Recreational Product

- 9.6.3 Others

- 9.7 Other Industrial Applications

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Biomer

- 11.2 Bluepha

- 11.3 CJ BIO (CJ CheilJedang)

- 11.4 Danimer Scientific

- 11.5 Full Cycle Bioplastics

- 11.6 Kaneka Corporation

- 11.7 Mango Materials

- 11.8 Newlight Technologies

- 11.9 Paques Biomaterials

- 11.10 PhaBuilder

- 11.11 Phangel Biotechnology

- 11.12 Tepha Inc.

- 11.13 TianAn Biologic

- 11.14 Tianjin Green-Bio

- 11.15 Weining Biotechnology

- 11.16 Yield10 Bioscience

聚羟基烷酯市场:全球市场按产品类型、製造流程、原料和应用进行预测-2026-2032年

聚羟基烷酯市场:全球市场按产品类型、製造流程、原料和应用进行预测-2026-2032年 聚羟基烷酯市场分析与预测(至2035年):类型、产品、应用、技术、材料类型、最终用户、製程、设备、解决方案、模式

聚羟基烷酯市场分析与预测(至2035年):类型、产品、应用、技术、材料类型、最终用户、製程、设备、解决方案、模式 全球聚羟基烷酯市场规模、份额、趋势和成长分析报告(2026-2034年)

全球聚羟基烷酯市场规模、份额、趋势和成长分析报告(2026-2034年) 聚羟基烷酯(PHA):市场占有率分析、产业趋势与统计、成长预测(2026-2031)

聚羟基烷酯(PHA):市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球聚羟基烷酯(PHA)市场(至2030年)按类型(短链/中链)、生产方法(糖发酵/植物油发酵)、应用(包装和食品服务/生物医学)和地区划分

全球聚羟基烷酯(PHA)市场(至2030年)按类型(短链/中链)、生产方法(糖发酵/植物油发酵)、应用(包装和食品服务/生物医学)和地区划分 聚羟基脂肪酸酯市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年)

聚羟基脂肪酸酯市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年) 聚羟基烷酸酯市场(类型:短炼和中链,最终用途:包装、油漆涂料、医疗、农业、纺织等)-全球产业分析、规模、份额、成长、趋势及预测,2024-2034

聚羟基烷酸酯市场(类型:短炼和中链,最终用途:包装、油漆涂料、医疗、农业、纺织等)-全球产业分析、规模、份额、成长、趋势及预测,2024-2034 聚羟基烷酯市场规模、份额和趋势分析报告:按类型、最终用途、按地区、细分市场预测,2024-2030 年聚羟基烷酯(PHA) 市场 - 2024 年至 2029 年预测

聚羟基烷酯市场规模、份额和趋势分析报告:按类型、最终用途、按地区、细分市场预测,2024-2030 年聚羟基烷酯(PHA) 市场 - 2024 年至 2029 年预测 聚羟基链烷酸(PHA)的全球市场(2016-2036)

聚羟基链烷酸(PHA)的全球市场(2016-2036)