|

市场调查报告书

商品编码

1913378

氟硅酸市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)Fluorosilicic Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

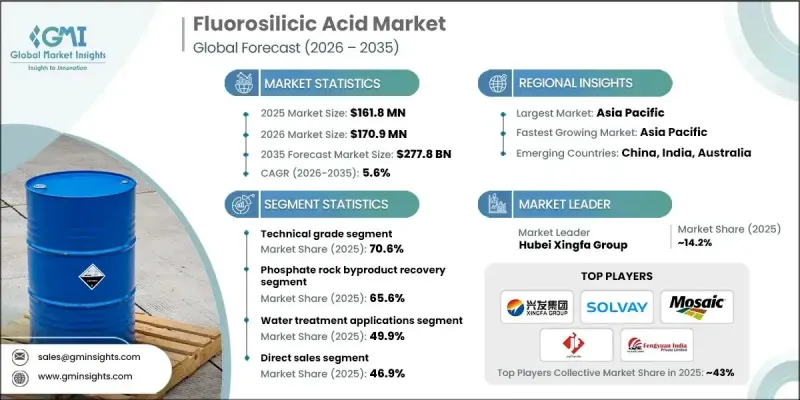

全球氟硅酸市场预计到 2025 年将达到 1.618 亿美元,到 2035 年将达到 2.778 亿美元,年复合成长率为 5.6%。

氟硅酸(化学式:H₂SiF₆)是一种无机化合物,以水溶液形式生产,市售纯度等级多样,从技术级到适用于受监管应用的高纯度级均有涵盖。在水处理系统、铝加工和精密製造等领域需求不断增长的推动下,市场持续发展。对回收效率、製程优化和品质保证的持续投入正在重塑供应结构,并支撑着长期需求的稳定性。生产商正积极提升生产标准,同时调整产量以满足更严格的应用要求。此外,市场也正在透过等级差异化进行发展,使供应商能够满足特定的性能和合规性需求。这种发展趋势正在推动更合理的定价结构、更深入的客户互动以及在工业和受监管终端应用领域的广泛应用,从而提升氟硅酸的全球重要性。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 1.618亿美元 |

| 市场规模预测 | 2.778亿美元 |

| 复合年增长率 | 5.6% |

电子级氟硅酸市场预计在2026年至2035年间将以6.8%的复合年增长率成长。该市场受益于先进製造环境中对符合严格成分和污染阈值要求的超纯化学原料日益增长的需求。纯化能力的不断提升使供应商能够提供高度稳定的产品质量,满足日益严格的技术规格。

2025年,磷矿石副产品回收领域占据了65.6%的市场份额,预计到2035年将以5.2%的复合年增长率成长。由于成本效益高、加工基础设施完善,以及有效利用可回收的氟化合物将产品流转化为具有商业性价值的材料,同时降低整体营运成本,该生产路线仍然占据主导地位。

预计2025年,美国氟硅酸市场规模将达3,190万美元。该国市场强劲成长主要得益于水处理项目的稳定需求、成熟的磷酸盐加工能力以及持续的工业消费。强有力的法律规范和规范化的品质要求也持续推动氟硅酸在多个应用领域的需求。

目录

第一章:分析方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按纯度等级

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计资料(HS编码)(註:贸易统计仅涵盖主要国家)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要企业的竞争分析

- 竞争定位矩阵

- 主要趋势

- 企业合併(M&A)

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依纯度等级分類的市场估算与预测(2022-2035 年)

- 技术级

- 试剂级

- 电子级

- 食品级及医药级

第六章 依生产方式分類的市场估算与预测(2022-2035 年)

- 磷矿石副产品回收

- 由硅化合物直接合成

- 氟硅酸盐分解法

- 其他的

7. 依最终用途产业分類的市场估计与预测(2022-2035 年)

- 水处理应用

- 水氟化

- 工业水处理

- 化学製造应用

- 氟化铝生产

- 氟化氢的生产

- 氟硅酸盐製造

- 电子和半导体应用

- 晶圆清洗

- 蚀刻

- 工业製程应用

- 金属表面处理

- 玻璃製造

- 油井酸处理

- 製造用途

- 纺织加工

- 建筑和砌体加固

- 木材防腐处理

- 特殊用途

- 食品和饮料灭菌

- pH值调节

- 其他的

第八章 按分销管道分類的市场估算和预测(2022-2035 年)

- 直销

- 化学品批发商和批发公司

- 化工公司

- 其他频道

第九章 各地区市场估算与预测(2022-2035 年)

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- American Elements

- Jayfluoride Private Limited

- Honeywell International

- Hubei Xingfa Group

- Hydrite Chemical

- ICL Group

- Simplot Company

- The Mosaic Company

- Sinograce Chemical

- Solvay

- Fengyuan Group

- IXOM

- Derivados Del Fluor

- Spectrum Chemical

- SoleChem SRL

The Global Fluorosilicic Acid Market was valued at USD 161.8 million in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 277.8 million by 2035.

Fluosilicic acid, chemically identified as H2SiF6, is produced as an aqueous inorganic compound and is commercially supplied in multiple purity levels ranging from technical specifications to highly refined grades suitable for regulated applications. The market continues to advance as demand strengthens across water treatment systems, aluminum-related processing, and high-precision manufacturing industries. Ongoing investments in recovery efficiency, process optimization, and quality assurance are reshaping supply dynamics and supporting long-term demand stability. Producers are actively enhancing production standards while aligning output with stricter application requirements. The market is also evolving through grade differentiation, allowing suppliers to meet specialized performance and compliance needs. This evolution supports stronger pricing structures, deeper customer engagement, and broader adoption across industrial and regulated end-use environments, reinforcing the global relevance of fluorosilicic acid.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $161.8 million |

| Forecast Value | $277.8 million |

| CAGR | 5.6% |

The electronic grade fluorosilicic acid segment will grow at a CAGR of 6.8% from 2026 to 2035. This segment benefits from rising demand for ultra-pure chemical inputs that meet strict compositional and contamination thresholds required in advanced manufacturing environments. Continuous improvements in purification capabilities are enabling suppliers to deliver highly consistent product quality aligned with increasingly stringent technical specifications.

The phosphate rock byproduct recovery segment accounted for 65.6% share in 2025 and is forecast to grow at a CAGR of 5.2% through 2035. This production route maintains dominance due to cost efficiency, integrated processing infrastructure, and effective utilization of recoverable fluorine compounds, transforming byproduct streams into commercially valuable materials while lowering overall operational costs.

U.S. Fluorosilicic Acid Market reached USD 31.9 million in 2025. Market strength in the country is supported by steady demand from water treatment programs, established phosphate processing capacity, and consistent industrial consumption. Strong regulatory oversight and structured quality requirements continue to reinforce demand across multiple application areas.

Key companies active in the Global Fluorosilicic Acid Market include Solvay, American Elements, The Mosaic Company, ICL Group, Honeywell International, Jayfluoride Private Limited, Hydrite Chemical, Simplot Company, Hubei Xingfa Group, Sinograce Chemical, Fengyuan Group, IXOM, Spectrum Chemical, Derivados Del Flour, and SoleChem S.R.L. Companies operating in the Global Fluorosilicic Acid Market are strengthening their competitive position through capacity optimization, grade diversification, and long-term supply agreements. Manufacturers are prioritizing investments in purification technologies to support higher-value product offerings while ensuring regulatory compliance across applications. Strategic focus on consistent quality, process reliability, and customized specifications is helping suppliers secure stable customer relationships. Firms are also enhancing logistics efficiency and regional supply capabilities to reduce delivery risks and improve responsiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Purity grade

- 2.2.2 Production method

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By purity grade

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Purity Grade, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 technical grade

- 5.3 reagent grade

- 5.4 electronic grade

- 5.5 food/pharmaceutical grade

Chapter 6 Market Estimates and Forecast, By Production Method, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Phosphate Rock Byproduct Recovery

- 6.3 Direct Synthesis from Silicon Compounds

- 6.4 Fluorosilicate Salt Decomposition

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Water treatment applications

- 7.2.1 Municipal water fluoridation

- 7.2.2 Industrial water treatment

- 7.3 Chemical production applications

- 7.3.1 Aluminum fluoride production

- 7.3.2 Hydrogen fluoride production

- 7.3.3 Silicofluorides production

- 7.4 Electronics & semiconductor applications

- 7.4.1 Wafer cleaning

- 7.4.2 Etching

- 7.5 Industrial processing applications

- 7.5.1 Metal surface treatment

- 7.5.2 Glass manufacturing

- 7.5.3 Oil well acidizing

- 7.6 Manufacturing applications

- 7.6.1 Textile processing

- 7.6.2 Construction and masonry hardening

- 7.6.3 Wood preservation

- 7.7 Specialty applications

- 7.7.1 Food and beverage sterilization

- 7.7.2 Ph adjustment

- 7.7.3 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Chemical distributors & wholesalers

- 8.4 Chemical trading companies

- 8.5 Other channels

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 American Elements

- 10.2 Jayfluoride Private Limited

- 10.3 Honeywell International

- 10.4 Hubei Xingfa Group

- 10.5 Hydrite Chemical

- 10.6 ICL Group

- 10.7 Simplot Company

- 10.8 The Mosaic Company

- 10.9 Sinograce Chemical

- 10.10 Solvay

- 10.11 Fengyuan Group

- 10.12 IXOM

- 10.13 Derivados Del Fluor

- 10.14 Spectrum Chemical

- 10.15 SoleChem S.R.L.

氟硅酸盐市场:产业趋势与全球市场预测(至2035年)

氟硅酸盐市场:产业趋势与全球市场预测(至2035年) 氟硅酸市场分析及预测(至2035年):类型、产品类型、应用、最终用户、製程、形态、安装类型、组件

氟硅酸市场分析及预测(至2035年):类型、产品类型、应用、最终用户、製程、形态、安装类型、组件 氟硅酸市场规模、份额及成长分析(按应用、最终用户及地区划分)-2026-2033年产业预测

氟硅酸市场规模、份额及成长分析(按应用、最终用户及地区划分)-2026-2033年产业预测 全球氟硅酸市场

全球氟硅酸市场