|

市场调查报告书

商品编码

1913379

血流动力学监测设备市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)Hemodynamic Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

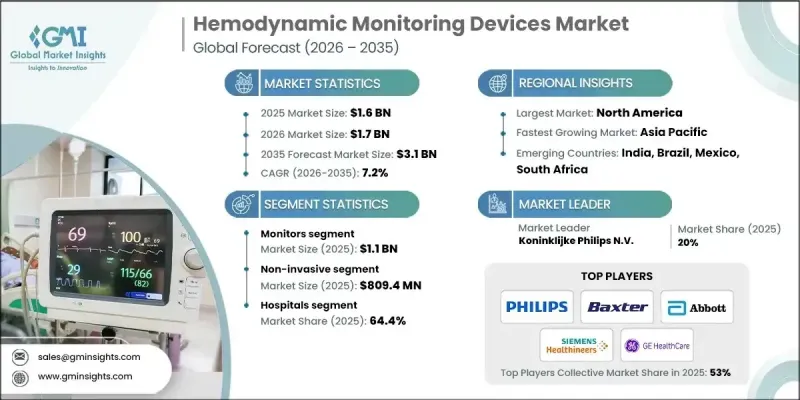

全球血液动力学监测设备市场预计到 2025 年将达到 16 亿美元,到 2035 年将达到 31 亿美元,年复合成长率为 7.2%。

全球慢性病盛行率上升、监测技术不断创新、远距医疗模式日益普及以及全球远端医疗手术数量不断增加,共同推动了血流动力学监测市场的成长。血流动力学监测设备是指透过即时追踪血压、血流和全身循环效率来评估心血管功能的系统。这些工具能够持续提供心抟出量、血管阻力及相关生理指标的讯息,进而辅助临床决策。它们在手术室、重症监护室和高依赖性医院环境中发挥着尤为重要的作用。慢性病盛行率的不断上升推动了对精准心血管评估工具的需求,尤其是在需要快速介入的情况下。与这些疾病相关的併发症促使医疗服务提供者采用先进的监测平台,以支持及时、准确的治疗决策。随着人工智慧 (AI) 和远端连接功能更深入地整合到监测解决方案中,血流动力学监测有望成为现代临床护理的核心组成部分,市场趋势预计将进一步加速发展。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 16亿美元 |

| 市场规模预测 | 31亿美元 |

| 复合年增长率 | 7.2% |

预计到2025年,监测领域的市场规模将达到11亿美元。该领域包括先进的床边系统、行动平台和整合监测解决方案,旨在提供连续的心血管数据,包括心抟出量、动脉压和中心静脉压。这些监测系统被认为是维持病患病情稳定和发展严重临床治疗策略的重要工具。加护病房(ICU)的使用率最高,因为在ICU中,不间断的心血管监测对于管理严重或病情不稳定的患者至关重要。

预计到2025年,非侵入性市场规模将达到8.094亿美元,到2035年将以7.3%的复合年增长率成长。非侵入性血流动力学监测解决方案是一种无需破皮或插入导管即可评估心血管参数的技术。这些系统利用先进的生理测量方法来评估心抟出量和液体反应性,并专注于病人安全和营运效率。由于非侵入性方法能够降低手术风险、缩短准备时间并提高成本效益,医疗机构正日益重视在手术全期和重症监护流程中采用这些方法。

预计到2025年,美国血流动力学监测设备市场规模将达到5.204亿美元。由于美国心血管疾病发病率高且医疗基础设施完善,预计美国将引领该市场。据悉,美国医院和先进的医疗中心高度依赖各种监测解决方案,以支持接受复杂外科手术、创伤治疗和高级心臟介入治疗的患者。

目录

第一章:分析方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 产业影响因素

- 司机

- 全球慢性病发生率不断上升

- 血流动力学监测设备的技术进步

- 人们对远端医疗服务的偏好日益增强

- 手术数量增加

- 产业潜在风险与挑战

- 病患监测设备高成本

- 严格的法规结构

- 市场机会

- 扩大门诊和居家医疗服务范围

- 整合人工智慧和数据分析

- 司机

- 成长潜力分析

- 监管环境

- 技术进步

- 当前技术趋势

- 新兴技术

- 供应链分析

- 救赎方案

- 价格分析(2024)

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 企业矩阵分析

- 主要企业的竞争分析

- 竞争定位矩阵

- 主要趋势

- 企业合併(M&A)

- 商业伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 按产品分類的市场估算与预测(2022-2035 年)

- 一次性产品

- 监视器

第六章 依系统类型分類的市场估算与预测(2022-2035 年)

- 非侵入性

- 侵入性

- 微创

7. 依最终用途分類的市场估计与预测(2022-2035 年)

- 医院

- 门诊手术中心

- 居家医疗

- 其他用途

第八章 各地区市场估算与预测(2022-2035 年)

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- Abbott Laboratories

- Baxter International

- Becton, Dickinson and Company(BD)

- Canon Medical Systems Corporation

- Deltex Medical Group

- Edwards Lifesciences Corporation

- GE HealthCare Technologies

- Getinge

- ICU Medical

- Koninklijke Philips NV

- Masimo Corporation

- Mindray

- Nihon Kohden Corporation

- OSYPKA MEDICAL

- Siemens Healthineers.

The Global Hemodynamic Monitoring Devices Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 3.1 billion by 2035.

The growth is explained by the rising global burden of long-term medical conditions, continuous innovation in monitoring technologies, wider acceptance of telehealth-based care models, and an increasing volume of surgical procedures worldwide. Hemodynamic monitoring devices are described as systems that assess cardiovascular performance by tracking blood pressure, blood flow, and overall circulatory efficiency in real time. These tools support clinical decision-making by delivering continuous insights into cardiac output, vascular resistance, and related physiological indicators. Their role is emphasized across surgical suites, intensive care environments, and high-dependency hospital settings. The expanding prevalence of chronic illnesses is said to be increasing demand for precise cardiovascular assessment tools, particularly where rapid intervention is required. Complications linked to these conditions are driving healthcare providers to adopt advanced monitoring platforms that support timely and accurate treatment decisions. Market momentum is expected to intensify as artificial intelligence and remote connectivity features become more deeply embedded in monitoring solutions, positioning hemodynamic monitoring as a core element of modern clinical care delivery.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 7.2% |

The monitors segment generated USD 1.1 billion in 2025. This category includes advanced bedside systems, mobile platforms, and integrated monitoring solutions designed to deliver continuous cardiovascular data, including cardiac output, arterial pressure, and central venous pressure. These monitoring systems are regarded as critical tools for maintaining patient stability and guiding therapeutic actions in high-acuity clinical settings. Utilization levels are highest in intensive care units, where uninterrupted cardiovascular monitoring is essential for managing patients with severe or unstable conditions.

The non-invasive segment reached USD 809.4 million in 2025 and is projected to grow at a CAGR of 7.3% throughout 2035. Non-invasive hemodynamic monitoring solutions are positioned as technologies that evaluate cardiovascular parameters without breaching the skin or requiring catheter placement. These systems rely on advanced physiological measurement methods to assess cardiac output and fluid responsiveness with a focus on patient safety and operational efficiency. Healthcare facilities are increasingly favoring non-invasive approaches due to reduced procedural risks, faster setup times, and improved cost efficiency across perioperative and critical care workflows.

U.S. Hemodynamic Monitoring Devices Market captured USD 520.4 million in 2025. The United States is described as leading the market due to a high incidence of cardiovascular disorders and a well-established healthcare infrastructure. Hospitals and advanced care centers across the country are said to rely heavily on a broad range of monitoring solutions to support patients undergoing complex surgical procedures, trauma management, and advanced cardiac interventions.

Key participants active in the Global Hemodynamic Monitoring Devices Market include Siemens Healthineers, Koninklijke Philips N.V., Edwards Lifesciences Corporation, GE HealthCare Technologies, Abbott Laboratories, Masimo Corporation, Mindray, Baxter International, Getinge, Nihon Kohden Corporation, Canon Medical Systems Corporation, Becton, Dickinson and Company, ICU Medical, Deltex Medical Group, and OSYPKA MEDICAL. Companies operating in the Global Hemodynamic Monitoring Devices Market are described as strengthening their market position through a combination of innovation, strategic partnerships, and geographic expansion. Product development efforts are focused on improving accuracy, usability, and data integration to support real-time clinical decision-making. Many players are investing in digital health capabilities, including remote monitoring and intelligent analytics, to align with evolving care models. Strategic collaborations with hospitals and research institutions help companies validate technologies and accelerate adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 System type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic diseases across the globe

- 3.2.1.2 Technological advancements in hemodynamic monitoring devices

- 3.2.1.3 Increasing preference for telehealth services

- 3.2.1.4 Growing number of surgeries

- 3.2.2 Industry Pitfalls and Challenges

- 3.2.2.1 High cost of patient monitoring devices

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market Opportunities

- 3.2.3.1 Expansion in ambulatory and homecare settings

- 3.2.3.2 Integration of AI and data analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Disposables

- 5.3 Monitors

Chapter 6 Market Estimates and Forecast, By System Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Non-invasive

- 6.3 Invasive

- 6.4 Minimally invasive

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Baxter International

- 9.3 Becton, Dickinson and Company (BD)

- 9.4 Canon Medical Systems Corporation

- 9.5 Deltex Medical Group

- 9.6 Edwards Lifesciences Corporation

- 9.7 GE HealthCare Technologies

- 9.8 Getinge

- 9.9 ICU Medical

- 9.10 Koninklijke Philips N.V.

- 9.11 Masimo Corporation

- 9.12 Mindray

- 9.13 Nihon Kohden Corporation

- 9.14 OSYPKA MEDICAL

- 9.15 Siemens Healthineers.

2026年全球血流动力学调节装置市场报告

2026年全球血流动力学调节装置市场报告 血流动力学监测系统市场:按产品类型、应用、最终用户和地区划分

血流动力学监测系统市场:按产品类型、应用、最终用户和地区划分 全球血流动力学监测系统市场规模、份额、趋势和成长分析报告(2026-2034年)

全球血流动力学监测系统市场规模、份额、趋势和成长分析报告(2026-2034年) 血流动力学监测市场规模、份额及成长分析(按类型、设备、配置、模式、最终用户和地区划分)-2026-2033年产业预测

血流动力学监测市场规模、份额及成长分析(按类型、设备、配置、模式、最终用户和地区划分)-2026-2033年产业预测 血流动力学监测系统市场规模、份额及成长分析(按类型、产品类型、模式及地区划分)-2026-2033年产业预测血流动力学监测系统市场:全球市场规模,2025-2030年

血流动力学监测系统市场规模、份额及成长分析(按类型、产品类型、模式及地区划分)-2026-2033年产业预测血流动力学监测系统市场:全球市场规模,2025-2030年 血流动力学监测设备市场规模、份额和趋势分析报告:按系统类型、产品、最终用途、地区和细分市场预测(2025-2033 年)2025年全球血流动力学监测系统市场报告

血流动力学监测设备市场规模、份额和趋势分析报告:按系统类型、产品、最终用途、地区和细分市场预测(2025-2033 年)2025年全球血流动力学监测系统市场报告 全球血流动力学监测设备市场

全球血流动力学监测设备市场 2025 年至 2033 年血流动力学监测市场规模、份额、趋势及预测(按产品、监测、最终用户和地区)

2025 年至 2033 年血流动力学监测市场规模、份额、趋势及预测(按产品、监测、最终用户和地区)