|

市场调查报告书

商品编码

1913431

诊断超音波市场机会、成长要素、产业趋势分析及预测(2026-2035年)Diagnostic Ultrasound Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

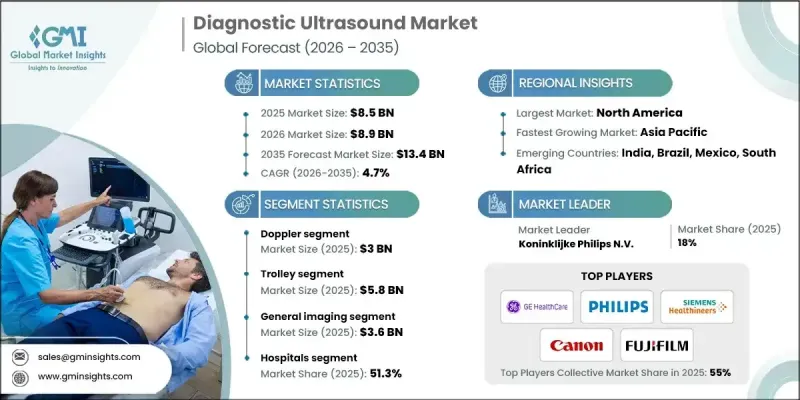

全球诊断超音波市场预计到 2025 年将达到 85 亿美元,到 2035 年将达到 134 亿美元,年复合成长率为 4.7%。

市场成长受多种因素驱动,包括已开发经济体和新兴经济体人口老化加剧、慢性病盛行率上升、部分国家出生率提高以及超音波设备的不断创新。诊断性超音波是一种非侵入性成像技术,利用超高频声波产生内部器官的高解析度影像。它广泛用于检查腹部、心臟、肌肉骨骼系统和其他身体部位。尤其在引导微创手术方面,例如怀孕期间胎儿监护和切片检查,超音波技术备受重视。心血管疾病、癌症和其他慢性疾病的增加推动了对安全且经济高效的诊断影像解决方案的需求。携带式和照护现场超音波系统的发展提高了医院和门诊的普及率,实现了快速、即时的诊断,从而提高了效率并改善了患者的治疗效果。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 85亿美元 |

| 预测金额 | 134亿美元 |

| 复合年增长率 | 4.7% |

预计到2025年,多普勒超音波市场规模将达30亿美元。多普勒超音波是一种透过检测声波频率变化来测量血管内血流的专业技术。它有多种形式,例如彩色多普勒、能量多普勒和频谱多普勒,广泛应用于心血管、血管和产科领域,提供重要的即时血流动力学资讯。其在诊断心血管疾病、监测胎儿健康和评估血管状况方面的作用,巩固了其在诊断超音波市场的主导地位。

预计到2025年,推车式超音波设备市场规模将达58亿美元。推车式超音波系统是传统的推车式设备,旨在为医院和诊断中心提供全面的超音波诊断服务。它们配备多个换能器和先进的成像功能,例如多普勒、3D/4D和造影超音波,是需要深度成像和无缝工作流程整合的高强度环境的理想选择。

预计到2025年,北美诊断超音波市场占有率将达到33.8%。该地区的市场份额得益于先进的医疗基础设施、对创新成像技术的早期应用以及主要製造商的存在。完善的报销政策、对诊断成像设施的持续投资以及超音波在心臟病学、产科和急诊医学领域日益增长的应用,都为该地区强大的市场地位做出了贡献。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 产业影响因素

- 司机

- 已开发国家和发展中国家老龄人口不断增长的趋势

- 慢性病发生率增加

- 开发中国家出生率不断上升

- 诊断超音波设备的创新与进展

- 产业潜在风险与挑战

- 熟练专业人员短缺,尤其是在发展中和欠发达地区。

- 发展中经济体普及诊断性超音波的障碍

- 市场机会

- 人工智慧(AI)与先进成像技术的融合

- 在预防和初级保健领域拓展应用

- 司机

- 成长潜力分析

- 监管环境

- 技术进步

- 当前技术趋势

- 新兴技术

- 供应链分析

- 救赎方案

- 2025年定价分析

- 未来市场趋势

- 差距分析

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 合作伙伴关係和合资企业

- 新产品发布

- 扩张计划

第五章 按技术分類的市场估算与预测,2022-2035年

- 2D

- 3D和4D

- 多普勒

第六章 市场估算与预测:2022-2035年手机性别分布

- 手推车

- 紧凑型/手持式

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 普通诊断影像

- 心臟病学

- 妇产科

- 其他应用

第八章 依最终用途分類的市场估算与预测,2022-2035年

- 医院

- 妇产科中心

- 其他用途

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第十章:公司简介

- Alpinion Medical Systems

- Butterfly Network

- Canon Medical Systems Corporation

- CHISON Medical Technologies

- Clarius Mobile Health

- Esaote SpA

- FujiFilm Holdings Corporation

- General Electric Company(GE Healthcare)

- Hologic, Inc.

- Konica Minolta Inc.

- Koninklijke Philips NV(BioTelemetry, Inc.)

- Samsung Electronics Co. Ltd.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Siemens Healthineers AG

- SonoScape

The Global Diagnostic Ultrasound Market was valued at USD 8.5 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 13.4 billion by 2035.

Market growth is driven by multiple factors, including a rising geriatric population in both developed and emerging regions, the growing prevalence of chronic illnesses, increasing birth rates in certain countries, and continuous technological innovations in ultrasound devices. Diagnostic ultrasound is a non-invasive imaging technology that generates high-resolution images of internal organs using ultra-high-frequency sound waves. It is widely used to examine the abdomen, heart, musculoskeletal system, and other body parts. Technology is particularly valued for fetal monitoring during pregnancy and for guiding minimally invasive procedures such as biopsies. Increasing rates of cardiovascular diseases, cancer, and other chronic conditions are driving demand for safe, cost-effective imaging solutions. The development of portable and point-of-care ultrasound systems is improving accessibility and enabling faster real-time diagnostics in hospitals and outpatient settings, enhancing both efficiency and patient outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.5 Billion |

| Forecast Value | $13.4 Billion |

| CAGR | 4.7% |

The Doppler segment reached USD 3 billion in 2025. Doppler ultrasound is a specialized modality that measures blood flow within vessels by detecting changes in sound wave frequency. Available in formats such as color, power, and spectral Doppler, it is widely used for cardiovascular, vascular, and obstetric applications, providing critical real-time hemodynamic information. Its role in diagnosing cardiovascular disorders, monitoring fetal health, and assessing vascular conditions drives its dominance in the diagnostic ultrasound market.

The trolley segment reached USD 5.8 billion in 2025. Trolley-based ultrasound systems are traditional cart-mounted devices designed for comprehensive hospital and diagnostic center use. Equipped with multiple transducers and advanced imaging features, including Doppler, 3D/4D, and contrast-enhanced ultrasound, these systems are ideal for high-volume settings that require detailed imaging and seamless workflow integration.

North America Diagnostic Ultrasound Market accounted for 33.8% share in 2025. The region's share is supported by advanced healthcare infrastructure, early adoption of innovative imaging technologies, and the presence of leading manufacturers. Established reimbursement policies, consistent investment in imaging facilities, and the growing use of ultrasound in cardiology, obstetrics, and emergency care contribute to its strong market position.

Key players operating in the Global Diagnostic Ultrasound Market include Siemens Healthineers AG, Canon Medical Systems Corporation, Alpinion Medical Systems, Butterfly Network, Konica Minolta Inc., General Electric Company (GE Healthcare), Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Samsung Electronics Co., Ltd., Clarius Mobile Health, Hologic, Inc., CHISON Medical Technologies, Koninklijke Philips N.V., SonoScape, Esaote SpA, and FujiFilm Holdings Corporation. Companies in the Global Diagnostic Ultrasound Market strengthen their position through continuous product innovation, expanding their portfolio of advanced imaging modalities such as Doppler, 3D/4D, and point-of-care devices. Strategic partnerships with hospitals, clinics, and research institutions help expand adoption and enhance brand visibility. R&D investment drives miniaturization, portability, and software-enabled diagnostic capabilities. Firms also focus on improving workflow integration, user-friendly interfaces, and AI-based imaging analytics to deliver more accurate and faster diagnostics.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Portability trends

- 2.2.4 Application trends

- 2.2.5 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population base in developed as well as developing regions

- 3.2.1.2 Increasing incidence of chronic diseases

- 3.2.1.3 Increasing birth rates in developing countries

- 3.2.1.4 Technological innovations and advancements in diagnostic ultrasound devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled professionals especially in developing and underdeveloped regions

- 3.2.2.2 Barriers impeding use of diagnostic ultrasound in developing economies

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and advanced imaging technologies

- 3.2.3.2 Increasing applications in preventive and primary care

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2025

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 2D

- 5.3 3D and 4D

- 5.4 Doppler

Chapter 6 Market Estimates and Forecast, By Portability, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Trolley

- 6.3 Compact/handheld

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 General imaging

- 7.3 Cardiology

- 7.4 OB/GYN

- 7.5 Other application

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Maternity centers

- 8.4 Other End Use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alpinion Medical Systems

- 10.2 Butterfly Network

- 10.3 Canon Medical Systems Corporation

- 10.4 CHISON Medical Technologies

- 10.5 Clarius Mobile Health

- 10.6 Esaote SpA

- 10.7 FujiFilm Holdings Corporation

- 10.8 General Electric Company (GE Healthcare)

- 10.9 Hologic, Inc.

- 10.10 Konica Minolta Inc.

- 10.11 Koninklijke Philips N.V. (BioTelemetry, Inc.)

- 10.12 Samsung Electronics Co. Ltd.

- 10.13 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 10.14 Siemens Healthineers AG

- 10.15 SonoScape

2026年全球携带式全数位彩色超音波诊断系统市场报告2026年全球携带式床边超音波诊断系统市场报告

2026年全球携带式全数位彩色超音波诊断系统市场报告2026年全球携带式床边超音波诊断系统市场报告 下一代超音波系统市场:按系统类型、技术、应用和最终用户划分-2026-2032年全球市场预测超音波市场:按产品、组件、便携性、显示类型、应用和最终用户划分-全球预测,2026-2032年宠物超导性核磁共振造影系统市场:按动物种类、磁场强度、系统类型、应用和最终用户划分-全球预测,2026-2032年

下一代超音波系统市场:按系统类型、技术、应用和最终用户划分-2026-2032年全球市场预测超音波市场:按产品、组件、便携性、显示类型、应用和最终用户划分-全球预测,2026-2032年宠物超导性核磁共振造影系统市场:按动物种类、磁场强度、系统类型、应用和最终用户划分-全球预测,2026-2032年 超音波清洗槽市场规模、份额和成长分析:按产品类型、技术、应用、最终用户、分销管道、地区和产业预测,2026-2033年

超音波清洗槽市场规模、份额和成长分析:按产品类型、技术、应用、最终用户、分销管道、地区和产业预测,2026-2033年 全球血管内超音波设备市场规模、份额、趋势和成长分析报告(2026-2034年)

全球血管内超音波设备市场规模、份额、趋势和成长分析报告(2026-2034年) 2026-2030年全球超音波设备市场2026年全球3D和4D超音波设备市场报告2026年全球医用超音波设备市场报告

2026-2030年全球超音波设备市场2026年全球3D和4D超音波设备市场报告2026年全球医用超音波设备市场报告