|

市场调查报告书

商品编码

1913435

车上Wi-Fi市场机会、成长要素、产业趋势分析及2026年至2035年预测In-car Wi-Fi Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

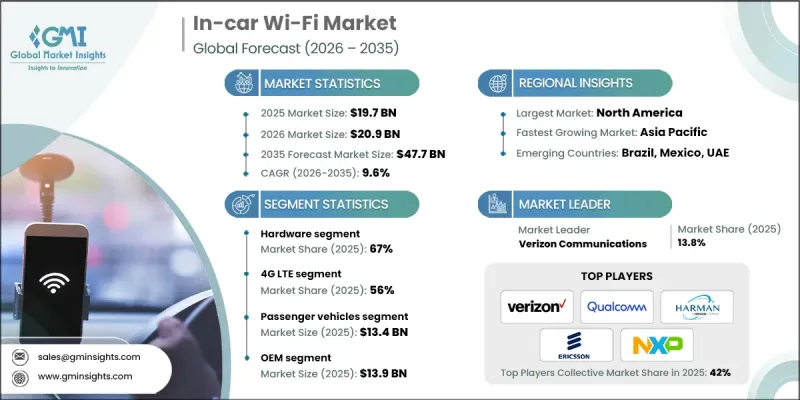

全球车载 Wi-Fi 市场预计到 2025 年将达到 197 亿美元,到 2035 年将达到 477 亿美元,年复合成长率为 9.6%。

这一成长主要得益于联网汽车的日益普及以及消费者对出行过程中不间断数位存取的日益增长的需求。汽车製造商和旅游服务供应商正越来越多地将无线连接作为标准配置,以提升用户舒适度、系统智慧和营运效能。行动网路基础设施和车载电子设备的持续进步,已将车载连线转变为支援多用户同时使用的高速、低延迟服务。先进的资料处理、云端整合和智慧网路管理提高了可靠性并加强了资料保护。随着车辆越来越主导软体,车载Wi-Fi已发展成为支援通讯、系统监控和远端更新的核心平台,巩固了其作为现代汽车设计基本要素的地位。不断扩展的互联出行生态系统和先进车辆技术的日益整合也进一步推动了市场成长。共用出行模式和下一代汽车的日益普及,推动了对持续连接的需求。车载Wi-Fi能够实现即时数据交换,进而提高导航精度、车辆监控、乘客服务和紧急应变能力,为个人和车队出行提供安全性和效率保障。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 197亿美元 |

| 预测金额 | 477亿美元 |

| 复合年增长率 | 9.6% |

预计到2025年,硬体部分将占据67%的市场份额,并在2026年至2035年间以9.9%的复合年增长率成长。这一主导地位反映了市场对车辆生产时整合的内建连接组件的强劲需求。随着先进通讯模组和网路设备的日益普及,硬体已成为车载Wi-Fi系统的基础,能够实现稳定的连接、高速数据传输以及支援多用户同时连接。

预计到2025年,4G LTE市占率将达到56%,并在2035年之前以9.2%的复合年增长率成长。其主导地位得益于广泛的网路覆盖范围、久经考验的性能和成本效益。基础设施的普及以及与现有车辆系统的兼容性,使得这项技术成为众多车型的首选。

预计到 2025 年,美国车载 Wi-Fi 市场将占据 87% 的市场份额,市场规模将达到 63 亿美元。成熟的汽车生态系统、先进的数位基础设施以及智慧连接解决方案的早期应用,巩固了北美地区的市场优势,帮助北美在全球市场中确立了强大的地位。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对联网汽车的需求不断增长

- 4G/5G网路扩展

- 电动车和自动驾驶汽车的发展

- 车队和旅游服务日益普及

- 产业潜在风险与挑战

- 高昂的实施成本和订阅成本

- 网路安全和资料隐私问题

- 市场机会

- 与5G、V2X和智慧运输系统的集成

- 数位服务和订阅变现

- 联网汽车自动驾驶汽车的普及

- 物联网和智慧运输应用

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- NAIC车辆Wi-Fi法规(美国)

- 美国州保险部门

- OSFI车上Wi-Fi指南(加拿大)

- 欧洲

- 德国金融监理局(BaFin)车载Wi-Fi法规

- 法国ACPR车载Wi-Fi法规

- 英国金融行为监理局 (PRA) 和金融行为监理局 (FCA) 的车载 Wi-Fi 指南

- 义大利IVASS车载Wi-Fi标准

- 亚太地区

- 中国银保监会关于车载Wi-Fi的规定

- 日本金融厅车用Wi-Fi管理条例

- 韩国金融服务委员会(FSC)和金融监督院(FSS)车载Wi-Fi指南

- 印度的IRDAI车载Wi-Fi标准

- 拉丁美洲

- 巴西的SUSEP车载Wi-Fi法规

- 墨西哥 CNSF 车载 Wi-Fi 指南

- 中东和非洲

- 阿联酋中央银行车载Wi-Fi指南

- 沙乌地阿拉伯中央银行(SAMA)车载Wi-Fi法规

- 北美洲

- 波特五力分析

- PESTEL 分析

- 技术与创新展望

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 使用案例场景

- 商用车辆车队管理与远端资讯处理

- 空中下载 (OTA) 更新和车辆诊断

- 高级车载资讯娱乐系统及乘客体验

- 自动驾驶汽车和ADAS支持

- 保险和风险管理

- 网路安全、资料隐私和合规框架

- 网路安全架构

- 资料隐私合规性

- 威胁情势

- 安全设计原则

- 资料管治

- 第三方风险管理

- 安全事件管理

- 合规成熟度模型

- 客户信任与品牌影响力

- 空中下载 (OTA) 更新:基础设施、部署和机队管理

- OTA 更新架构

- 零接触配置

- 软体部署策略

- 舰队特有的挑战

- 对连结性的依赖

- 更新频率和速度

- 成本结构

- 实现互联服务

- 预测性维护集成

- OTA监管合规性

- 车队管理平台集成

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 按组件分類的市场估算与预测,2022-2035年

- 硬体

- 无线路由器

- 内建模组

- OBD-II设备

- 天线和接收器

- 软体和服务

- 连线管理

- 基于云端的解决方案

- 资讯娱乐应用

第六章 按技术分類的市场估计与预测,2022-2035年

- 4G LTE

- 5G NR

- Wi-Fi 6

第七章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第八章 按分销管道分類的市场估算与预测,2022-2035年

- OEM

- 售后市场

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Global Player

- AT&T

- Berkshire Hathaway

- Broadcom

- Ericsson

- Harman International

- Munich Re

- NXP Semiconductors

- Qualcomm

- Swiss Re

- Verizon Communications

- Regional Player

- China Re

- Hannover Re

- Lloyd's

- MTN

- PartnerRe

- Reliance Jio

- SCOR

- SoftBank

- Telefonica

- Telstra

- 新兴企业

- Autotalks

- CalAmp

- Cohda Wireless

- Icomera

- Veniam

The Global In-car Wi-Fi Market was valued at USD 19.7 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 47.7 billion by 2035.

Growth is supported by the rising penetration of connected vehicles and increasing consumer expectations for uninterrupted digital access while traveling. Vehicle manufacturers and mobility providers are increasingly embedding wireless connectivity as a standard vehicle capability to improve user comfort, system intelligence, and operational performance. Continuous progress in mobile network infrastructure and vehicle electronics has transformed in-car connectivity into a high-speed, low-latency service that supports multiple users simultaneously. Advanced data processing, cloud integration, and intelligent network management have improved reliability and strengthened data protection. As vehicles become more software-driven, in-car Wi-Fi has evolved into a central platform that supports communication, system monitoring, and remote updates, reinforcing its role as a core element of modern automotive design. Market growth is further supported by the expanding connected mobility ecosystem and the rising integration of advanced vehicle technologies. Increased adoption of shared mobility models and next-generation vehicles has intensified the need for constant connectivity. In-car Wi-Fi enables real-time data exchange that improves navigation accuracy, vehicle oversight, passenger services, and emergency response capabilities, supporting both safety and efficiency across personal and fleet-based transportation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.7 Billion |

| Forecast Value | $47.7 Billion |

| CAGR | 9.6% |

The hardware segment held 67% share in 2025 and is projected to grow at a CAGR of 9.9% from 2026 to 2035. This dominance reflects strong demand for built-in connectivity components integrated during vehicle production. High adoption of advanced communication modules and network equipment has made hardware the foundation of in-car Wi-Fi systems, delivering stable connectivity, fast data transfer, and support for multiple connected users.

The 4G LTE segment accounted for 56% share in 2025 and is anticipated to grow at a CAGR of 9.2% through 2035. Its leadership is driven by broad network availability, proven performance, and cost efficiency. Widespread infrastructure and compatibility with existing vehicle systems have made this technology the preferred choice across a wide range of vehicle categories.

United States In-car Wi-Fi Market held 87% share and generated USD 6.3 billion in 2025. Regional leadership is supported by a well-established automotive ecosystem, advanced digital infrastructure, and early adoption of intelligent connectivity solutions, reinforcing North America's strong position in the global market.

Key companies operating in the Global In-car Wi-Fi Market include Qualcomm, Verizon Communications, Harman International, Ericsson, AT&T, NXP Semiconductors, Broadcom, Berkshire Hathaway, Swiss Re, and Munich Re. Companies in the Global In-car Wi-Fi Market strengthen their competitive position through continuous technology development, strategic collaborations, and long-term agreements with vehicle manufacturers. Firms invest in advanced connectivity solutions that deliver higher speeds, improved reliability, and stronger security. Expanding product portfolios to support both passenger and commercial vehicles helps address the diverse needs of the market. Partnerships with network providers enable broader coverage and service consistency. Companies also focus on scalable platforms that support future upgrades without major hardware changes.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Vehicle

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for connected vehicles

- 3.2.1.2 Expansion of 4G/5G networks

- 3.2.1.3 Growth of electric and autonomous vehicles

- 3.2.1.4 Increasing adoption of fleet and mobility services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and subscription costs

- 3.2.2.2 Cybersecurity and data privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with 5G, V2X, and smart mobility ecosystems

- 3.2.3.2 Monetization through digital services and subscriptions

- 3.2.3.3 Connected and autonomous vehicle adoption

- 3.2.3.4 IoT and smart mobility applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 NAIC In-car Wi-Fi Regulations (U.S.)

- 3.4.1.2 U.S. State Insurance Departments

- 3.4.1.3 OSFI In-car Wi-Fi Guidelines (Canada)

- 3.4.2 Europe

- 3.4.2.1 Germany BaFin In-car Wi-Fi Rules

- 3.4.2.2 France ACPR In-car Wi-Fi Regulations

- 3.4.2.3 UK PRA & FCA In-car Wi-Fi Guidelines

- 3.4.2.4 Italy IVASS In-car Wi-Fi Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China CBIRC In-car Wi-Fi Rules

- 3.4.3.2 Japan FSA In-car Wi-Fi Regulations

- 3.4.3.3 South Korea FSC & FSS In-car Wi-Fi Guidelines

- 3.4.3.4 India IRDAI In-car Wi-Fi Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazil SUSEP In-car Wi-Fi Rules

- 3.4.4.2 Mexico CNSF In-car Wi-Fi Guidelines

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE Central Bank In-car Wi-Fi Guidelines

- 3.4.5.2 Saudi Arabia SAMA In-car Wi-Fi Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.12.1 Fleet Management & Telematics for Commercial Vehicles

- 3.12.2 Over-the-Air (OTA) Updates & Vehicle Diagnostics

- 3.12.3 Premium In-Vehicle Infotainment & Passenger Experience

- 3.12.4 Autonomous Vehicle & ADAS Support

- 3.12.5 Insurance & Risk Management

- 3.13 Cybersecurity, Data Privacy & Compliance Framework

- 3.13.1 Cybersecurity Architecture

- 3.13.2 Data Privacy Compliance

- 3.13.3 Threat Landscape

- 3.13.4 Security-by-Design Principles

- 3.13.5 Data Governance

- 3.13.6 Third-Party Risk Management

- 3.13.7 Security Incident Management

- 3.13.8 Compliance Maturity Models

- 3.13.9 Customer Trust & Brand Impact

- 3.14 Over-the-Air (OTA) Updates: Infrastructure, Deployment & Fleet Management

- 3.14.1 OTA Update Architecture

- 3.14.2 Zero-Touch Provisioning

- 3.14.3 Software Deployment Strategies

- 3.14.4 Fleet-Specific Challenges

- 3.14.5 Connectivity Dependency

- 3.14.6 Update Frequency & Cadence

- 3.14.7 Cost Structure

- 3.14.8 Connected Services Enablement

- 3.14.9 Predictive Maintenance Integration

- 3.14.10 Regulatory Compliance via OTA

- 3.14.11 Fleet Management Platform Integration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Wi-Fi routers

- 5.2.2 Embedded modules

- 5.2.3 OBD-II devices

- 5.2.4 Antennas & receivers

- 5.3 Software & services

- 5.3.1 Connectivity management

- 5.3.2 Cloud-based solutions

- 5.3.3 Infotainment applications

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 4G LTE

- 6.3 5G NR

- 6.4 Wi-Fi 6

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicle (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 AT&T

- 10.1.2 Berkshire Hathaway

- 10.1.3 Broadcom

- 10.1.4 Ericsson

- 10.1.5 Harman International

- 10.1.6 Munich Re

- 10.1.7 NXP Semiconductors

- 10.1.8 Qualcomm

- 10.1.9 Swiss Re

- 10.1.10 Verizon Communications

- 10.2 Regional Player

- 10.2.1 China Re

- 10.2.2 Hannover Re

- 10.2.3 Lloyd’s

- 10.2.4 MTN

- 10.2.5 PartnerRe

- 10.2.6 Reliance Jio

- 10.2.7 SCOR

- 10.2.8 SoftBank

- 10.2.9 Telefonica

- 10.2.10 Telstra

- 10.3 Emerging Players

- 10.3.1 Autotalks

- 10.3.2 CalAmp

- 10.3.3 Cohda Wireless

- 10.3.4 Icomera

- 10.3.5 Veniam

2026年全球反辐射飞弹市场报告

2026年全球反辐射飞弹市场报告 行动端购买者行为指南(2025)美国行动装置以旧换新和保护市场的成长机会2026年全球超行动装置市场报告

行动端购买者行为指南(2025)美国行动装置以旧换新和保护市场的成长机会2026年全球超行动装置市场报告 超移动设备市场-全球产业规模、份额、趋势、机会及预测(按类型、设备类型、应用、地区及竞争格局划分,2021-2031年)

超移动设备市场-全球产业规模、份额、趋势、机会及预测(按类型、设备类型、应用、地区及竞争格局划分,2021-2031年) 智慧家庭电子产品市场按产品类型、连接技术、安装类型、分销管道和最终用户划分-2026年至2032年全球预测行动数据采集软体市场按组件、设备类型、部署模式、组织规模、应用和最终用户行业划分 - 全球预测 2026-2032

智慧家庭电子产品市场按产品类型、连接技术、安装类型、分销管道和最终用户划分-2026年至2032年全球预测行动数据采集软体市场按组件、设备类型、部署模式、组织规模、应用和最终用户行业划分 - 全球预测 2026-2032 5G 大规模 MIMO追踪新兴行动装置技术:市场数据概览(2026 年第一季)

5G 大规模 MIMO追踪新兴行动装置技术:市场数据概览(2026 年第一季) 智慧型手机电视市场规模、份额和成长分析(按内容类型、技术、萤幕大小、分销管道、服务类型、用途、应用、最终用户和地区划分)—产业预测(2026-2033 年)

智慧型手机电视市场规模、份额和成长分析(按内容类型、技术、萤幕大小、分销管道、服务类型、用途、应用、最终用户和地区划分)—产业预测(2026-2033 年)