|

市场调查报告书

商品编码

1913447

二丁基羟基甲苯市场机会、成长要素、产业趋势分析及2026年至2035年预测Butylated Hydroxytoluene (BHT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

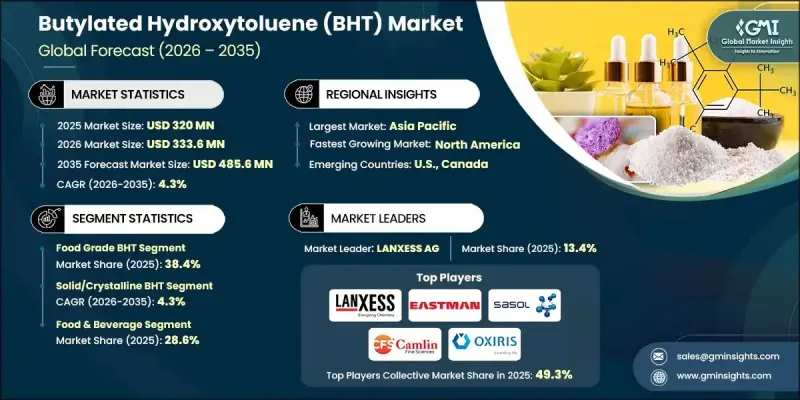

全球二丁基羟基甲苯(BHT) 市场预计到 2025 年将达到 3.2 亿美元,到 2035 年将达到 4.856 亿美元,年复合成长率为 4.3%。

二丁基羟基甲苯)作为一种高效能抗氧化剂在多个工业领域的广泛应用,推动了市场的发展。 BHT在延缓油脂氧化方面发挥关键作用,直接有助于提高产品稳定性并延长保质期。其清除自由基的能力可防止产品劣化和腐败,使其成为食品保鲜、个人保健产品和药品的重要成分。包装和保质期产品需求的不断增长,进一步提升了BHT在工业生产中的重要性。 BHT因其成本效益高、抗氧化性能强且对产品特性影响小而持续受到青睐。开发中国家食品加工和化妆品生产的扩张也进一步推动了市场成长。然而,某些地区不断变化的法规结构和健康相关问题正在影响市场动态,要求製造商专注于合规性、品质保证和产品纯度,以维持需求并确保市场的长期稳定。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 3.2亿美元 |

| 预测金额 | 4.856亿美元 |

| 复合年增长率 | 4.3% |

预计到2025年,食品级BHT的市占率将达到38.4%,并在2035年之前以4.4%的复合年增长率成长。该细分市场受益于加工食品、谷物、饮料和动物营养产品中对抗氧化剂解决方案的强劲需求。维持产品新鲜度和完整性的需求持续推动消费,而法律规范和不断变化的消费者偏好正在影响配方策略。

2025年,固体或结晶质BHT市占率达到73.4%,预计2026年至2035年将以4.3%的复合年增长率成长。这种形态的产品因其稳定性好、易于操作、可精确计量以及与多种配方相容性强而被广泛采用。其性能稳定和储存优势持续推动其在食品、医药和化妆品等应用领域的需求。

预计到2025年,北美二丁基羟基甲苯(BHT)市占率将达到29.9%。食品、製药和化妆品製造商的稳定需求,以及严格的品质和安全标准,正在支撑该地区的成长。对高纯度配方的重视和对合规性的承诺,正在影响采购决策并维持市场成长动能。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 2022-2035年各等级市场估算与预测

- 食品级BHT

- 医药级

- 工业技术级BHT

第六章 按类型分類的市场估算与预测,2022-2035年

- 固体/结晶质BHT

- 液态BHT

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 食品/饮料

- 化妆品和个人护理

- 药物製剂

- 聚合物/塑胶稳定剂

- 润滑油/石油产品

- 饲料添加剂

- 包装材料和食品接触物质

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- AB Enterprises

- Akrochem Corporation

- Anmol Chemicals

- Camlin Fine Sciences Ltd.

- Eastman Chemical Company

- Kemin Industries

- KH Chemicals BV

- Lanxess AG

- Oxiris Chemicals SA

- Ratnagiri Chemicals Pvt Ltd

- Sasol Limited

- SI Group

The Global Butylated Hydroxytoluene (BHT) Market was valued at USD 320 million in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 485.6 million by 2035.

Market development is supported by the widespread use of butylated hydroxytoluene as an effective antioxidant across multiple industries. BHT plays a critical role in slowing oxidation in fats and oils, which directly supports longer product stability and extended shelf life. Its ability to neutralize free radicals helps prevent degradation and quality loss, making it an essential ingredient in food preservation, personal care formulations, and pharmaceutical products. Rising demand for packaged and long-shelf-life products is reinforcing its importance in industrial processing. BHT continues to be favored due to its cost efficiency, strong antioxidant performance, and minimal impact on product characteristics. Expanding food processing and cosmetics production in developing economies is further supporting market growth. However, evolving regulatory frameworks and health-related concerns in certain regions are shaping market dynamics, encouraging manufacturers to focus on compliance, quality assurance, and product purity to maintain demand and ensure long-term market stability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $320 Million |

| Forecast Value | $485.6 Million |

| CAGR | 4.3% |

The food grade BHT accounted for 38.4% share in 2025 and is expected to grow at a CAGR of 4.4% through 2035. This segment benefits from strong demand for antioxidant solutions in processed foods, cereals, beverages, and animal nutrition products. The need to maintain freshness and product integrity continues to support consumption, although regulatory oversight and shifting consumer preferences are influencing formulation strategies.

The solid or crystalline BHT segment held 73.4% share in 2025 and is forecast to grow at a CAGR of 4.3% from 2026 to 2035. This form is widely adopted due to its stability, ease of handling, precise dosing capability, and compatibility with various formulations. Its consistent performance and storage advantages continue to drive demand across food, pharmaceutical, and cosmetic applications.

North America Butylated Hydroxytoluene (BHT) Market held 29.9% share in 2025. Regional growth is supported by stable demand from food, pharmaceutical, and cosmetic manufacturers, along with strict quality and safety standards. Emphasis on high-purity formulations and regulatory compliance continues to shape purchasing decisions and sustain market momentum.

Key companies operating in the Global Butylated Hydroxytoluene (BHT) Market include Lanxess AG, Eastman Chemical Company, SI Group, Sasol Limited, Kemin Industries, Camlin Fine Sciences Ltd., Akrochem Corporation, KH Chemicals BV, Oxiris Chemicals S.A., Ratnagiri Chemicals Pvt Ltd, AB Enterprises, and Anmol Chemicals. Companies active in the Global Butylated Hydroxytoluene (BHT) Market are strengthening their competitive position through a combination of quality enhancement, regulatory alignment, and portfolio optimization. Manufacturers are focusing on producing high-purity grades to meet increasingly strict safety standards across food, cosmetic, and pharmaceutical applications. Strategic investments in process efficiency and quality control systems are helping improve consistency and reliability. Firms are also expanding their presence in emerging markets where food processing and personal care industries are growing steadily. Long-term supply agreements with end users, competitive pricing strategies, and improved distribution networks are supporting market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Grade

- 2.2.3 Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Food grade BHT

- 5.3 Pharmaceutical grade

- 5.4 Technical/industrial grade BHT

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid/crystalline BHT

- 6.3 Liquid BHT

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Cosmetics & personal care

- 7.4 Pharmaceutical formulations

- 7.5 Polymer & plastic stabilization

- 7.6 Lubricants & petroleum products

- 7.7 Animal feed additives

- 7.8 Packaging materials & food contact substances

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AB Enterprises

- 9.2 Akrochem Corporation

- 9.3 Anmol Chemicals

- 9.4 Camlin Fine Sciences Ltd.

- 9.5 Eastman Chemical Company

- 9.6 Kemin Industries

- 9.7 KH Chemicals BV

- 9.8 Lanxess AG

- 9.9 Oxiris Chemicals S.A.

- 9.10 Ratnagiri Chemicals Pvt Ltd

- 9.11 Sasol Limited

- 9.12 SI Group