|

市场调查报告书

商品编码

1913449

爆炸物及烟火市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)Explosives and Pyrotechnics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

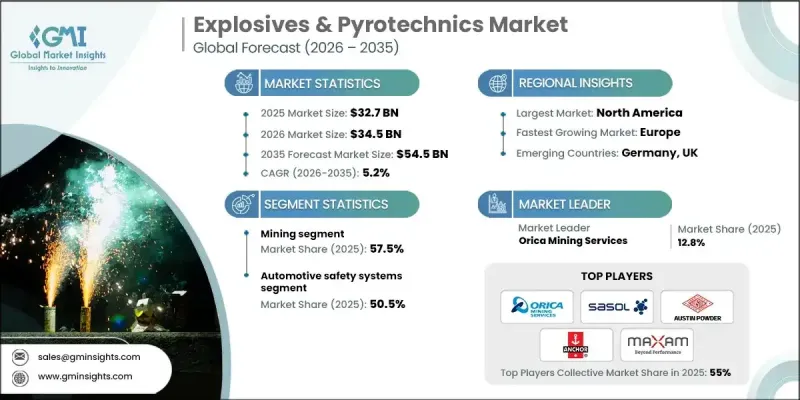

全球炸药和烟火市场预计到 2025 年将达到 327 亿美元,到 2035 年将达到 545 亿美元,年复合成长率为 5.2%。

该市场涵盖用于采矿和基础设施建设的商业爆破剂、应用于国防和航太项目的高能化合物,以及整合到汽车安全系统和受控视觉显示器中的烟火组件。硝酸铵基组合药物占据主导地位,由于持续的采矿和采石活动,年需求量达到约2000万吨。用于车辆安全机制的烟火组件被列为联合国编号3268(第9类物质),并依照规定的热驱动和电力驱动要求进行製造,以确保性能可预测。国防和航太应用仍然是稳定的成长要素,这得益于公共部门对依赖高能量材料的弹药和推进系统的持续投资。汽车烟火组件也因高产量和强制性安全标准而产生稳定的需求。同时,环境问题正在推动材料创新。传统的硝酸盐基炸药面临排放和残留物的挑战,促使供应商优化配方并提高生产效率。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 327亿美元 |

| 预测金额 | 545亿美元 |

| 复合年增长率 | 5.2% |

采矿业的成长主要得益于铜、镍、锂和其他关键矿物产量的增加,预计到 2025 年将占 57.5% 的市场份额。清洁能源供应链的扩张和长期资源需求直接导致爆破材料消耗量的增加,露天矿场倾向于使用散装乳化炸药,而地下计划则越来越多地采用包装产品和电子爆破系统。

到 2025 年,汽车安全应用领域将占 50.5% 的市场份额,这反映出市场对按照既定的运输和认证标准製造的安全气囊和约束启动系统有着强劲的需求。

美国炸药和烟火市场预计到 2025 年将达到 79 亿美元,到 2035 年将达到 127 亿美元。持续的国防费用、成熟的国内製造能力和先进的数位爆破技术的应用支撑了市场成长,而加拿大透过金属和钾肥开采贡献了稳定的需求。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 价格趋势

- 按地区

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 依应用领域分類的炸药市场(2022-2035 年)

- 矿业

- 采煤

- 金属矿业

- 其他的

- 建筑和基础设施

- 隧道及地下工程

- 道路和高速公路建设

- 水坝、水库和发电工程

- 其他的

- 军事/国防

- 军事训练与模拟

- 军事技术/建筑

- 海军和海上作战

- 其他的

- 其他的

- 石油和天然气产业

- 雪崩预防和雪灾预防

- 农业和土地开发

- 岩土工程与科学应用

- 应急服务与灾害应对

- 林业和伐木

第六章 烟火市场:依应用领域划分(2022-2035 年)

- 消费品及零售

- 一般消费者

- 零售通路

- 其他的

- 汽车业:安全系统

- 航太太空产业

- 军事/国防

- 海洋/海事应用

- 其他的

第七章 市场规模及预测:依地区划分(2022-2035 年)

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第八章 公司简介

- Orica Mining Services

- Incitec Pivot Limited

- Sasol Limited

- Austin Powder Company

- ENAEX

- MAXAM Corp

- AECI Group

- EPC Group

- Chemring Group

- Titanobel SAS

- Hanwha Corporation

- LSB Industries Inc

- Solar Industries India

- Zambelli Fireworks

- Howard &Sons

- Angelfire Pyrotechnics

- Pyro Company Fireworks

- Melrose Pyrotechnics

- Skyburst The Firework

- Entertainment Fireworks

- Supreme Fireworks UK

- Celebration Fireworks

- Impact Pyro

The Global Explosives & Pyrotechnics Market was valued at USD 32.7 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 54.5 billion by 2035.

This market encompasses commercial blasting materials used in mining and infrastructure development, energetic compounds applied in defense and aerospace programs, and pyrotechnic components integrated into automotive safety systems and controlled visual displays. Bulk ammonium nitrate-based formulations continue to account for the largest consumption volumes, with annual demand reaching nearly 20 million tons due to sustained mining and quarrying activity. Pyrotechnic components used in vehicle safety mechanisms are regulated as UN 3268 Class 9 materials and are manufactured to meet defined thermal and electrical activation requirements ensure predictable performance. Defense and aerospace applications remain stable growth contributors, supported by ongoing public-sector investment in munitions and propulsion systems that rely on energetic materials. Automotive-related pyrotechnics also generate consistent demand due to high production volumes and mandatory safety standards. At the same time, environmental considerations are influencing material innovation, as traditional nitrate-based explosives carry emissions and residue challenges that are encouraging suppliers to optimize formulations and manufacturing efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $32.7 Billion |

| Forecast Value | $54.5 Billion |

| CAGR | 5.2% |

The mining segment held 57.5% share in 2025, driven by the rising production of copper, nickel, lithium, and other critical minerals. Expanding clean energy supply chains and long-term resource requirements translate directly into higher blasting material consumption, with surface operations favoring bulk emulsions and underground projects relying more on packaged products and electronic blasting systems.

The automotive safety applications segment accounted for 50.5% share in 2025, reflecting strong demand for airbag and restraint activation systems manufactured under established transport and qualification standards.

U.S. Explosives & Pyrotechnics Market reached USD 7.9 billion in 2025 and is projected to reach USD 12.7 billion by 2035. Growth is supported by sustained defense spending, mature domestic production capacity, and advanced adoption of digital blasting technologies, while Canada contributes steady demand through metals and potash extraction.

Key companies active in the Global Explosives & Pyrotechnics Market include Orica Mining Services, MAXAM Corp, ENAEX, AECI Group, Incitec Pivot Limited, Austin Powder Company, Sasol Limited, EPC Group, Chemring Group, Titanobel SAS, Hanwha Corporation, LSB Industries Inc., Solar Industries India, Zambelli Fireworks, Celebration Fireworks, Supreme Fireworks UK, Entertainment Fireworks, Melrose Pyrotechnics, Impact Pyro, Skyburst The Firework, Angelfire Pyrotechnics, Pyro Company Fireworks, Howard & Sons, and Impact Pyro. Companies operating in the Global Explosives & Pyrotechnics Market are strengthening their market position by focusing on operational efficiency, digital blasting solutions, and product innovation that improves safety and performance consistency. Strategic investments in capacity expansion and localized manufacturing help ensure supply reliability near major mining and defense customers. Many players are also prioritizing environmentally optimized formulations to address regulatory pressure and sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Explosives Market, By End-user

- 2.2.2 Pyrotechnics Market, By End-user

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Explosives Market, By End Use, 2022-2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Mining

- 5.2.1 Coal mining

- 5.2.2 Metal mining

- 5.2.3 Others

- 5.3 Construction & infrastructure

- 5.3.1 Tunneling & underground construction

- 5.3.2 Road & highway construction

- 5.3.3 Dam, reservoir & hydroelectric projects

- 5.3.4 Others

- 5.4 Military & defense

- 5.4.1 Military training & simulation

- 5.4.2 Military engineering & construction

- 5.4.3 Naval & maritime operations

- 5.4.4 Others

- 5.5 Others

- 5.5.1 Oil & gas industry

- 5.5.2 Avalanche control & snow safety

- 5.5.3 Agriculture & land clearing

- 5.5.4 Geotechnical & scientific applications

- 5.5.5 Emergency services & disaster response

- 5.5.6 Forestry & logging

Chapter 6 Pyrotechnics Market, By End Use, 2022-2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Consumer & retail

- 6.2.1 Household consumers

- 6.2.2 Retail distribution channels

- 6.2.3 Others

- 6.3 Automotive industry - safety systems

- 6.4 Aerospace & space industry

- 6.5 Military & defense

- 6.6 Marine & maritime applications

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Orica Mining Services

- 8.2 Incitec Pivot Limited

- 8.3 Sasol Limited

- 8.4 Austin Powder Company

- 8.5 ENAEX

- 8.6 MAXAM Corp

- 8.7 AECI Group

- 8.8 EPC Group

- 8.9 Chemring Group

- 8.10 Titanobel SAS

- 8.11 Hanwha Corporation

- 8.12 LSB Industries Inc

- 8.13 Solar Industries India

- 8.14 Zambelli Fireworks

- 8.15 Howard & Sons

- 8.16 Angelfire Pyrotechnics

- 8.17 Pyro Company Fireworks

- 8.18 Melrose Pyrotechnics

- 8.19 Skyburst The Firework

- 8.20 Entertainment Fireworks

- 8.21 Supreme Fireworks UK

- 8.22 Celebration Fireworks

- 8.23 Impact Pyro

2026年全球爆炸物和烟火市场报告RDX、HMX 和 C-4 全球市场报告 2026RDX和HMX全球市场报告(2026年)

2026年全球爆炸物和烟火市场报告RDX、HMX 和 C-4 全球市场报告 2026RDX和HMX全球市场报告(2026年) 炸药市场:2026-2032年全球市场预测(依产品类型、配方、应用、分销管道及最终用户划分)

炸药市场:2026-2032年全球市场预测(依产品类型、配方、应用、分销管道及最终用户划分) 全球研究部:炸药市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球烟火化学品市场报告RDX(高爆炸药)全球市场报告(2026年)

全球研究部:炸药市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球烟火化学品市场报告RDX(高爆炸药)全球市场报告(2026年) 烟火市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、通路、地区及竞争格局划分,2021-2031年)矿用炸药市场-全球产业规模、份额、趋势、机会及预测(按应用、类型、地区和竞争格局划分,2021-2031年)

烟火市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、通路、地区及竞争格局划分,2021-2031年)矿用炸药市场-全球产业规模、份额、趋势、机会及预测(按应用、类型、地区和竞争格局划分,2021-2031年) 2026-2030年全球RDX和HMX市场

2026-2030年全球RDX和HMX市场