|

市场调查报告书

商品编码

1913451

汽车差速器市场成长机会、成长要素、产业趋势分析及2026年至2035年预测Automotive Differential Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

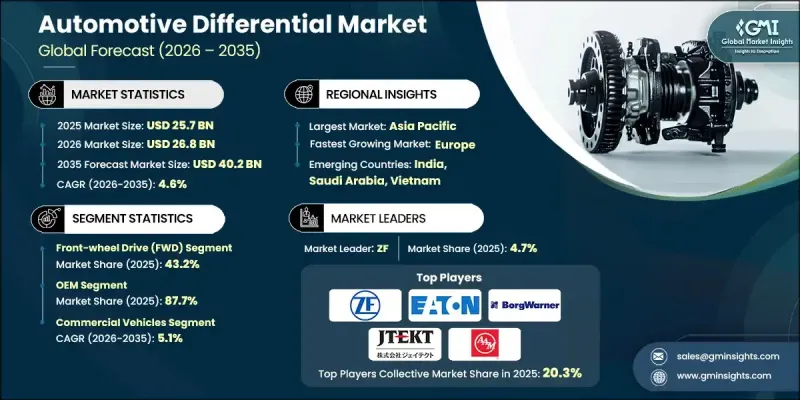

全球汽车差速器市场预计到 2025 年将达到 257 亿美元,到 2035 年将达到 402 亿美元,年复合成长率为 4.6%。

中产阶级消费者可支配收入的增加以及全球汽车产量的成长支撑了市场成长,而这又得益于交通运输和物流行业的持续扩张。个人出行和货运需求的成长推动了乘用车和商用车的持续生产,从而直接支撑了对汽车差速器的需求。公共交通系统和物流业务的成长进一步加速了巴士、厢型车和卡车的生产,进一步增强了市场成长势头。差速器製造商正在加紧开发针对特定车型的解决方案,以适应不断变化的动力传动系统总成架构。电动和混合动力汽车的日益普及促使供应商重新设计和整合差速器系统,以满足新的动力传动系统要求。技术进步推动了对电子控制和智慧差速器的日益关注,这些系统能够改善扭矩分配、牵引力管理和车辆稳定性。随着车辆系统向软体主导和感测器整合方向发展,电子控制的先进差速器在各类车辆中的重要性日益凸显。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 257亿美元 |

| 预测金额 | 402亿美元 |

| 复合年增长率 | 4.6% |

截至2025年,前轮驱动车型市占率达43.2%,营收达111亿美元。前轮驱动配置因其成本效益高、结构紧凑(将动力传动系统零件整合于单一总成中)而广泛应用。这种结构降低了製造复杂性和整车成本,从而帮助其在全球市场广受欢迎。

2025年,OEM细分市场占市场份额的87.7%,预计到2035年将达到359亿美元。由于OEM能够提供符合整合车辆生产策略和不断变化的性能要求的高品质、特定应用的零件,因此它们仍然是差速器供应的主要来源。

美国汽车差速器市场预计到2025年将达到38.3亿美元。汽车製造业活动的增加以及汽车製造商与零件供应商之间合作的加强推动了市场成长。由于内部生产成本高昂,汽车製造商纷纷与专业的差速器製造商合作,以满足其客製化的传动系统需求。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 全球汽车产量增加

- 对SUV和四轮传动车的需求不断增长

- 越野和休閒车市场成长

- 商用车越来越受欢迎

- 产业潜在风险与挑战

- 车辆重量和包装限制

- 设计和维护的复杂性

- 市场机会

- 电动车中电动差速器的普及率越来越高

- 高性能差速器的售后市场需求不断成长

- 新兴汽车市场的成长

- 开发轻巧小巧的差速器解决方案

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国汽车工程师协会 (SAE)

- FMVSS(联邦机动车辆安全标准 - NHTSA)

- ASTM International

- CSA集团

- 欧洲

- 联合国欧洲经济委员会(UNECE)条例(ECE)

- ISO(国际标准化组织)

- EN标准(CEN)

- TUV标准与认证

- 亚太地区

- JIS(日本工业标准)

- GB/T标准(中国)

- AIS(印度汽车工业标准)

- 拉丁美洲

- ABNT 标准(巴西)

- NOM标准(墨西哥)

- IRAM 标准(阿根廷)

- 中东和非洲

- 波湾合作理事会(GSO)标准

- SASO标准(沙乌地阿拉伯)

- 南非标准局 (SABS)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产基地

- 消费基础

- 出口和进口

- 成本細項分析

- 永续性和环境影响

- 环境影响评估

- 社会影响力和社区服务

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 电气化影响评估

- 电动车差速器的设计差异

- 电子桥接器整合趋势

- 电动车中的扭力向量控制

- 传统製造商转型面临的挑战

- 性能和效率基准

- 按类型分類的差异化效率等级

- 耐久性和寿命分析

- 噪音、振动和声振粗糙度 (NVH) 性能

- 温度控管能力

- 案例研究

- 未来前景与机会

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依车辆类型分類的市场估计与预测,2022-2035年

- 开放式差速器

- 限滑差速器(LSD)

- 电子控制限滑差速器(ELSD)

- 差速锁

- 手动锁(驾驶员操作)

- 自动锁定机构(侦测车轮打滑)

- 扭力差速器

第六章 按组件分類的市场估算与预测,2022-2035年

- 差速器

- 差速器壳体

- 轴承和密封件

- 电子控制零件

第七章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- MCV

- 重型商用车(HCV)

第八章 按驱动类型分類的市场估算与预测,2022-2035年

- 前轮驱动(FWD)

- 后轮驱动(RWD)

- 全轮驱动(AWD)/四轮驱动(4WD)

9. 2022-2035年按推进方式分類的市场估计与预测

- 内燃机(ICE)

- 电动车(EV)

- 杂交种

第十章 依销售管道分類的市场估计与预测,2022-2035年

- OEM

- 售后市场

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 新加坡

- 马来西亚

- 印尼

- 越南

- 泰国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 世界公司

- ZF

- American Axle &Manufacturing(AAM)

- Dana

- BorgWarner

- GKN Automotive

- Eaton

- JTEKT

- Linamar

- Schaeffler

- Magna

- Hyundai Mobis

- Meritor(Cummins)

- Continental

- NSK

- 本地公司

- Bharat Gears

- Neapco

- Huayu Automotive Systems

- Tata Motors

- Sona Comstar

- AmTech

- Univance

- 新兴企业

- Auburn Gear

- Drexler Automotive

- RT Quaife

- Xtrac

The Global Automotive Differential Market was valued at USD 25.7 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 40.2 billion by 2035.

Market growth is supported by rising global vehicle production, driven by higher disposable income levels among middle-class consumers and continued expansion within the transportation and logistics sectors. Increasing demand for personal mobility and freight movement is contributing to sustained production of both passenger and commercial vehicles, which directly supports demand for automotive differentials. Growth in public transportation systems and logistics operations has further accelerated manufacturing of buses, vans, and trucks, strengthening market momentum. Differential manufacturers are increasingly developing vehicle-specific solutions to align with changing powertrain architectures. The growing presence of electric and hybrid vehicles is encouraging suppliers to redesign and integrate differential systems suited to new drivetrain requirements. Technology advancement is shifting focus toward electronically controlled and smart differential systems that enhance torque distribution, traction management, and vehicle stability. As vehicle systems become more software-driven and sensor-integrated, electronically advanced differentials are gaining greater relevance across multiple vehicle categories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $25.7 Billion |

| Forecast Value | $40.2 Billion |

| CAGR | 4.6% |

The front-wheel drive segment held 43.2% share and generated USD 11.1 billion in 2025. Front-wheel drive configurations are widely adopted due to their cost efficiency and compact design, where power delivery components are integrated into a single assembly. This structure reduces manufacturing complexity and overall vehicle cost, supporting widespread use across global markets.

The original equipment manufacturer segment accounted for 87.7% share in 2025 and is expected to reach USD 35.9 billion by 2035. OEMs remain the primary channel for differential supply due to their ability to deliver high-quality, application-specific components that align with integrated vehicle production strategies and evolving performance requirements.

U.S. Automotive Differential Market reached USD 3.83 billion in 2025. Market growth is supported by rising vehicle production activity and increasing collaboration between automakers and component suppliers. High manufacturing costs associated with in-house production are encouraging OEMs to partner with specialized differential manufacturers to meet customized drivetrain needs.

Key companies operating in the Global Automotive Differential Market include Dana, ZF, Magna, Eaton, BorgWarner, GKN Automotive, Schaeffler, American Axle & Manufacturing, Linamar, and JTEKT. Companies active in the Global Automotive Differential Market are strengthening their market position through technology innovation, strategic partnerships, and platform-specific product development. Many manufacturers are investing in advanced differential technologies that improve efficiency, durability, and electronic control compatibility. Collaboration with vehicle OEMs is being prioritized to co-develop integrated drivetrain solutions tailored to evolving powertrain architectures. Firms are expanding their global manufacturing footprint to serve regional markets more efficiently and reduce supply chain risks. Emphasis on lightweight materials and precision engineering is helping improve performance and fuel efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Differential

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Drive

- 2.2.6 Propulsion

- 2.2.7 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Growing demand for SUVs and all-wheel drive vehicles

- 3.2.1.3 Growth in off-road and recreational vehicle segment

- 3.2.1.4 Increasing penetration of commercial vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Weight and packaging constraints in vehicles

- 3.2.2.2 Complexity in design and maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of electric differentials in EVs

- 3.2.3.2 Increasing aftermarket demand for performance differentials

- 3.2.3.3 Growth in emerging automotive markets

- 3.2.3.4 Development of lightweight and compact differential solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 SAE (Society of Automotive Engineers)

- 3.4.1.2 FMVSS (Federal Motor Vehicle Safety Standards - NHTSA)

- 3.4.1.3 ASTM International

- 3.4.1.4 CSA Group

- 3.4.2 Europe

- 3.4.2.1 UNECE Regulations (ECE)

- 3.4.2.2 ISO (International Organization for Standardization)

- 3.4.2.3 EN Standards (CEN)

- 3.4.2.4 TUV Standards/Certifications

- 3.4.3 Asia Pacific

- 3.4.3.1 JIS (Japanese Industrial Standards)

- 3.4.3.2 GB/T Standards (China)

- 3.4.3.3 AIS (Automotive Industry Standards - India)

- 3.4.4 Latin America

- 3.4.4.1 ABNT Standards (Brazil)

- 3.4.4.2 NOM Standards (Mexico)

- 3.4.4.3 IRAM Standards (Argentina)

- 3.4.5 Middle East & Africa

- 3.4.5.1 GSO Standards (Gulf Cooperation Council)

- 3.4.5.2 SASO Standards (Saudi Arabia)

- 3.4.5.3 SABS Standards (South Africa)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Electrification impact assessment

- 3.12.1 EV differential design differences

- 3.12.2 E-axle integration trends

- 3.12.3 Torque vectoring in EVs

- 3.12.4 Transition challenges for traditional manufacturers

- 3.13 Performance & efficiency benchmarking

- 3.13.1 Differential efficiency ratings by type

- 3.13.2 Durability and lifespan analysis

- 3.13.3 Noise, vibration, and harshness (NVH) performance

- 3.13.4 Thermal management capabilities

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Differential, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Open differential

- 5.3 Limited-slip differential (LSD)

- 5.4 Electronic limited-slip differential (ELSD)

- 5.5 Locking differential

- 5.5.1 Manual Locking (Driver-activated)

- 5.5.2 Automatic Locking (Sensing wheel slip)

- 5.6 Torque differential

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Differential Gears

- 6.3 Differential Case/Housing

- 6.4 Bearings & Seals

- 6.5 Electronic Control Components

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Drive, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Front-wheel drive (FWD)

- 8.3 Rear-wheel drive (RWD)

- 8.4 All-wheel drive (AWD)/Four-wheel drive (4WD)

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 EV

- 9.4 Hybrid

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 ZF

- 12.1.2 American Axle & Manufacturing (AAM)

- 12.1.3 Dana

- 12.1.4 BorgWarner

- 12.1.5 GKN Automotive

- 12.1.6 Eaton

- 12.1.7 JTEKT

- 12.1.8 Linamar

- 12.1.9 Schaeffler

- 12.1.10 Magna

- 12.1.11 Hyundai Mobis

- 12.1.12 Meritor (Cummins)

- 12.1.13 Continental

- 12.1.14 NSK

- 12.2 Regional companies

- 12.2.1 Bharat Gears

- 12.2.2 Neapco

- 12.2.3 Huayu Automotive Systems

- 12.2.4 Tata Motors

- 12.2.5 Sona Comstar

- 12.2.6 AmTech

- 12.2.7 Univance

- 12.3 Emerging companies

- 12.3.1 Auburn Gear

- 12.3.2 Drexler Automotive

- 12.3.3 RT Quaife

- 12.3.4 Xtrac

商用车差速器市场:依车辆类型、差速器类型、传动系统、材质、替换零件和销售管道划分-2026-2032年全球市场预测

商用车差速器市场:依车辆类型、差速器类型、传动系统、材质、替换零件和销售管道划分-2026-2032年全球市场预测 汽车差速器市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测

汽车差速器市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测 汽车差速器市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、产品类型、驱动类型、地区和竞争格局划分,2021-2031年)

汽车差速器市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、产品类型、驱动类型、地区和竞争格局划分,2021-2031年) 汽车差速器市场:按类型、驱动系统和地区划分

汽车差速器市场:按类型、驱动系统和地区划分 全球汽车差速器系统市场:市场规模、份额和趋势分析(按类型、传动系统、车辆类型、零件、推进系统和地区划分),细分市场预测(2025-2033 年)

全球汽车差速器系统市场:市场规模、份额和趋势分析(按类型、传动系统、车辆类型、零件、推进系统和地区划分),细分市场预测(2025-2033 年) 汽车差异化:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

汽车差异化:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)