|

市场调查报告书

商品编码

1913459

安全物流市场机会、成长要素、产业趋势分析及预测(2026-2035年)Secure Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

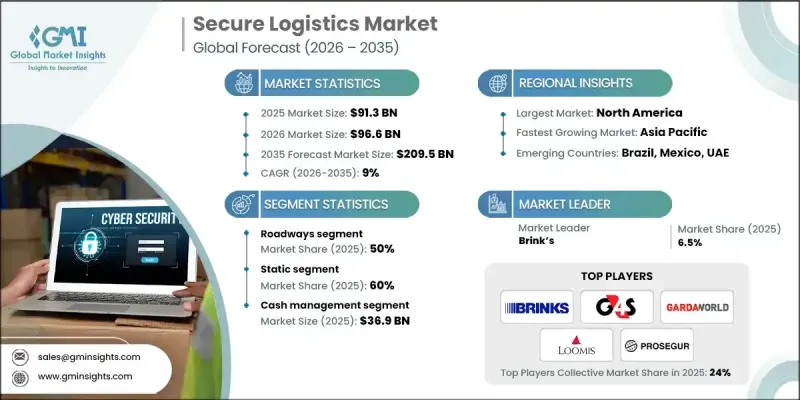

全球安全物流市场预计到 2025 年将达到 913 亿美元,到 2035 年将达到 2,095 亿美元,年复合成长率为 9%。

这一增长主要得益于国际贸易的稳步增长、对高价值货物保护日益增长的关注,以及对可靠合规的价值链运营的日益依赖。各行各业的组织越来越重视保护货币资产、敏感材料、受管制货物和关键业务文件,从而推动了对专业物流服务的需求。物流营运的持续数位转型正在改变传统的运输和仓储模式,提升了整个运输生命週期的可视性、可追溯性和风险管理水准。对货物从收集、运输到交付的整个过程进行端到端监控,正成为企业减少损失、提高营运效率和满足监管要求的标准要求。此外,电子商务的成长、国际货运量的成长、支付生态系统的不断发展,以及对高价值货物风险缓解和保险调整的日益重视,都进一步推动了市场扩张。安全可靠的物流服务已成为业务永续营运和营运韧性的基础要素。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 913亿美元 |

| 预测金额 | 2095亿美元 |

| 复合年增长率 | 9% |

2025年,道路运输市占率占比达到50%,预计2026年至2035年将以8.4%的复合年增长率成长。该领域之所以能保持主导地位,是因为它能够柔软性、可靠且经济高效地运输高价值和敏感货物。数位化车队管理和监控能力的广泛应用,提高了交付的可靠性,降低了风险,并确保了国内和区域供应链的合规性。道路运输的营运范围和扩充性使其成为各行各业的首选。

预计到2025年,静态储存市场份额将达到60%,并在2035年之前以8%的复合年增长率成长。该细分市场主导地位,是因为它能够提供安全的储存环境、集中式管理功能以及对资产的持续监控。先进的资料驱动型管理工具和整合监控框架能够提高工作流程效率、增强安全标准,并确保分散式营运的一致性。静态储存服务构成了全面安全物流网路的基础架构,并支援与行动营运的无缝整合。

预计2025年,美国安全物流市场规模将达到2,42亿美元,占76%的市占率。市场领先地位的支撑因素包括:大型企业高度集中于高价值资产的管理、先进的数位化应用以及完善的监管体系。整合物流平台、即时视觉化工具和预测性风险管理解决方案的广泛应用,持续推动美国市场的扩张。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 现金运输和高价值货物保护的需求日益增长

- 技术进步

- 监理合规要求

- 电子商务和跨境贸易的成长

- 产业潜在风险与挑战

- 高昂的营运成本

- 安全风险和窃盗

- 市场机会

- 在新兴市场拓展业务

- 整合数位化解决方案

- 3. 为高价值和机密货物提供专业的安全解决方案

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国运输部(DOT) 和联邦汽车运输安全管理局 (FMCSA) 的指导方针

- OSHA标准

- 加拿大贵重货物运输法规与劳动法

- 欧洲

- 德国联邦劳动和社会事务部(BMAS)和联邦警察(Bundespolizei)的规定

- 法国国家资讯与自由委员会 (CNIL) 和内政部指南

- 英国警察总长协会 (ACPO) 和健康与安全执行局 (HSE) 指南

- 义大利内政部和劳动部合规

- 亚太地区

- 中国国土交通运输部和公共安全的指导意见

- 日本国土交通省(MLIT)合规性

- 韩国僱佣劳动部规章

- 印度公路运输部和公路部指南

- 拉丁美洲

- 巴西运输部和MTE指南

- 墨西哥联邦通讯部 (SCT) 和劳动部 (STPS) 的指导方针

- 中东和非洲

- 阿联酋人力资源与酋长国化部指南

- 沙乌地阿拉伯王国人力资源和社会发展部和运输部规章

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 使用案例场景

- 风险、威胁与损失概况分析

- 盗窃、劫持和武装抢劫风险分析

- 内部威胁和共谋风险

- 网路和实体安全威胁(GPS欺骗、资料外洩)

- 区域风险强度图(高风险走廊)

- 保险、责任与风险转移机制

- 高价值货物的保险承保模式

- 托运人、物流公司和保险公司之间的责任划分

- 损失历史如何影响保费

- 区域责任限额规定

- 服务等级架构和合约模型

- 端对端和模组化安全物流服务的比较

- 服务等级协定配置(回应时间、丢包阈值、违约金)

- 合约期限和定价结构

- 供应商锁定和退出风险

- 安全基础设施和资产配置分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 按服务分類的市场估算与预测,2022-2035年

- 静止的

- 移动的

第六章 依运输方式分類的市场估计与预测,2022-2035年

- 道路运输

- 空运

- 铁路

- 水道

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 现金管理

- 贵金属

- 机密文件

- 高灵敏度电子设备

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

第九章:公司简介

- Global Player

- Brink's

- DHL Secure Logistics

- G4S

- GardaWorld

- Loomis

- Loomis International

- Malca-Amit

- Prosegur

- Securitas

- Transguard

- Regional Player

- Brink's UK

- CMS Info Systems

- G4S South Africa

- GardaWorld Canada

- Loomis France

- Maltacourt Global Logistics

- Prosegur Cash Mexico

- 欧洲安全现金

- Transnational Secure Logistics

- Tristar Secure Logistics

- 新兴企业

- Apex Cash Transport

- Elite Armored Transport

- Quantum Secure Logistics

- Sentinel Cash Solutions

- Swift Secure Logistics

The Global Secure Logistics Market was valued at USD 91.3 billion in 2025 and is estimated to grow at a CAGR of 9% to reach USD 209.5 billion by 2035.

Growth is being driven by the steady rise in international trade, heightened concern around the protection of high-value shipments and increasing reliance on dependable and compliant supply chain operations. Organizations across multiple sectors are placing greater emphasis on safeguarding monetary assets, sensitive materials, regulated goods, and critical business documents, which is elevating demand for specialized logistics services. Ongoing digital transformation within logistics operations is reshaping traditional transport and storage models by improving visibility, traceability, and risk control throughout the movement lifecycle. End-to-end oversight of assets during collection, transit, and delivery is becoming a standard requirement as businesses seek to minimize loss, enhance operational efficiency, and meet regulatory expectations. Market expansion is further supported by the growth of online commerce, rising international shipment volumes, evolving payment ecosystems, and increased focus on risk mitigation and insurance alignment for valuable cargo. Secure logistics services have become a foundational component of business continuity and operational resilience.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $91.3 Billion |

| Forecast Value | $209.5 Billion |

| CAGR | 9% |

The roadways segment accounted for 50% share in 2025 and is projected to grow at a CAGR of 8.4% from 2026 to 2035. This segment maintains its lead due to its ability to provide adaptable, dependable, and cost-efficient movement of high-value and sensitive consignments. Broad deployment of digitally enabled fleet management and monitoring capabilities supports reliable delivery performance, risk reduction, and compliance across domestic and regional supply chains. The operational reach and scalability of road-based transport continue to make it the preferred option across industries.

The static segment held 60% share in 2025 and is expected to register a CAGR of 8% through 2035. This segment leads due to its role in providing secure storage environments, centralized control functions, and continuous oversight of assets. Advanced data-driven management tools and integrated monitoring frameworks enable improved workflow efficiency, enhanced protection standards, and consistent compliance across distributed operations. Static services form the structural backbone of comprehensive secure logistics networks and support seamless coordination with mobile operations.

United States Secure Logistics Market accounted for 76% share and generated USD 24.2 billion in 2025. Market leadership is supported by a strong concentration of large enterprises handling high-value assets, advanced digital adoption, and well-established regulatory systems. Widespread use of integrated logistics platforms, real-time visibility tools, and predictive risk management solutions continues to drive market expansion across the country.

Key companies operating in the Global Secure Logistics Market include Prosegur, Brink's, Loomis, GardaWorld, G4S, Transguard, Securitas, DHL Secure Logistics, CMS Info Systems, and Maltacourt Global Logistics. Companies in the Global Secure Logistics Market are strengthening their market position through technology-driven service enhancement and geographic expansion. Many providers are investing in advanced digital platforms to improve visibility, control, and risk assessment across logistics operations. Strategic partnerships with financial institutions, retailers, and technology firms are helping expand service portfolios and client reach. Firms are also focusing on fleet modernization, infrastructure upgrades, and workforce training to improve service reliability and compliance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Mode of Transportation

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for cash-in-transit and high-value goods protection

- 3.2.1.2 Technological advancements

- 3.2.1.3 Regulatory compliance requirements

- 3.2.1.4 Growth in e-commerce and cross-border trade

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operational costs

- 3.2.2.2 Security risks and theft

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Integration of digital solutions

- 3.2.3. 3 Specialized secure solutions for high-value and sensitive goods

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. DOT & FMCSA Guidelines

- 3.4.1.2 OSHA Standards

- 3.4.1.3 Canada Transport of Valuable Goods Regulations & Labour Code

- 3.4.2 Europe

- 3.4.2.1 Germany BMAS & Bundespolizei Regulations

- 3.4.2.2 France CNIL & Ministry of the Interior Guidelines

- 3.4.2.3 United Kingdom ACPO & HSE Guidelines

- 3.4.2.4 Italy Ministry of the Interior & Ministry of Labour Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China MOHURD & Public Security Bureau Guidelines

- 3.4.3.2 Japan MLIT Compliance

- 3.4.3.3 South Korea MOEL Regulations

- 3.4.3.4 India MoRTH Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil Ministry of Transport & MTE Guidelines

- 3.4.4.2 Mexico SCT & STPS Guidelines

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE Ministry of Human Resources & Emiratisation Guidelines

- 3.4.5.2 Saudi Arabia HRSD & Transport Ministry Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Risk, Threat & Loss Profile Analysis

- 3.13.1 Theft, hijacking & armed robbery risk profiling

- 3.13.2 Insider threat & collusion risks

- 3.13.3 Cyber-physical security threats (GPS spoofing, data breaches)

- 3.13.4 Regional risk intensity mapping (high-risk corridors)

- 3.14 Insurance, liability & risk transfer mechanisms

- 3.14.1 Insurance coverage models for high-value cargo

- 3.14.2 Liability allocation between shipper, logistics provider & insurer

- 3.14.3 Impact of loss history on premiums

- 3.14.4 Regulatory limits on liability by region

- 3.15 Service-Level Architecture & Contract Models

- 3.15.1 End-to-end vs modular secure logistics services

- 3.15.2 SLA structures (response time, loss thresholds, penalties)

- 3.15.3 Contract duration & pricing structures

- 3.15.4 Vendor lock-in and exit risks

- 3.16 Secure Infrastructure & Asset Deployment Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Static

- 5.3 Mobile

Chapter 6 Market Estimates & Forecast, By Mode of Transportation, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Roadways

- 6.3 Airways

- 6.4 Railways

- 6.5 Waterways

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Cash Management

- 7.3 Precious Metals

- 7.4 Confidential Documents

- 7.5 Sensitive Electronics

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Belgium

- 8.3.7 Netherlands

- 8.3.8 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 Singapore

- 8.4.6 South Korea

- 8.4.7 Vietnam

- 8.4.8 Indonesia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Global Player

- 9.1.1 Brink’s

- 9.1.2 DHL Secure Logistics

- 9.1.3 G4S

- 9.1.4 GardaWorld

- 9.1.5 Loomis

- 9.1.6 Loomis International

- 9.1.7 Malca-Amit

- 9.1.8 Prosegur

- 9.1.9 Securitas

- 9.1.10 Transguard

- 9.2 Regional Player

- 9.2.1 Brink’s UK

- 9.2.2 CMS Info Systems

- 9.2.3 G4S South Africa

- 9.2.4 GardaWorld Canada

- 9.2.5 Loomis France

- 9.2.6 Maltacourt Global Logistics

- 9.2.7 Prosegur Cash Mexico

- 9.2.8 SecurCash Europe

- 9.2.9 Transnational Secure Logistics

- 9.2.10 Tristar Secure Logistics

- 9.3 Emerging Players

- 9.3.1 Apex Cash Transport

- 9.3.2 Elite Armored Transport

- 9.3.3 Quantum Secure Logistics

- 9.3.4 Sentinel Cash Solutions

- 9.3.5 Swift Secure Logistics

安全物流市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

安全物流市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 安全物流市场规模、份额和成长分析(按类型、运输方式、应用、最终用户和地区划分)—产业预测(2026-2033 年)

安全物流市场规模、份额和成长分析(按类型、运输方式、应用、最终用户和地区划分)—产业预测(2026-2033 年) 安全物流市场规模、份额和趋势分析报告:按类型、运输方式、应用、最终用途、地区和细分市场预测(2025-2030 年)

安全物流市场规模、份额和趋势分析报告:按类型、运输方式、应用、最终用途、地区和细分市场预测(2025-2030 年) 按服务类型、最终用户和地区分類的安全物流市场

按服务类型、最终用户和地区分類的安全物流市场 安全物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

安全物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 安全物流市场,按运输方式、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

安全物流市场,按运输方式、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 全球安全物流市场 2024-2031

全球安全物流市场 2024-2031 安全物流市场、占有率、规模、趋势、产业分析报告:依应用程式、运输方式、最终用户、类型、地区、细分市场进行预测,2024-2032 年

安全物流市场、占有率、规模、趋势、产业分析报告:依应用程式、运输方式、最终用户、类型、地区、细分市场进行预测,2024-2032 年