|

市场调查报告书

商品编码

1913468

甜菜碱市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Betaine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

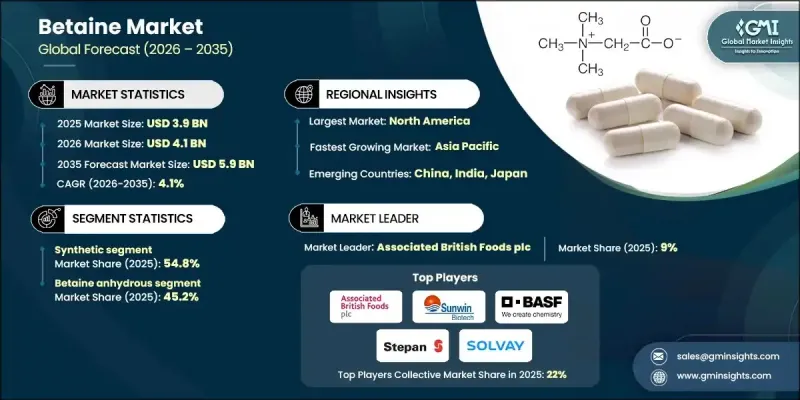

全球甜菜碱市场预计到 2025 年将达到 39 亿美元,到 2035 年将达到 59 亿美元,年复合成长率为 4.1%。

甜菜碱在营养、消费品和工业等多个终端应用产业的广泛应用推动了市场发展。人们对甜菜碱多功能性的认识不断提高,巩固了其作为关键成分的地位,使其在营养、性能提升和配方优化方面具有显着优势。全球人口成长、畜牧业扩张带来的蛋白质消费量增加以及消费者对天然环保成分的需求转变等结构性趋势,进一步促进了甜菜碱的长期成长。甜菜碱功能价值的科学检验不断增强其在商业应用上的信誉。市场前景也反映了持续的创新努力,这些努力致力于改进配方、提高生产效率和改进纯化方法。这些进展使供应商能够提高产品一致性、扩展应用范围并满足不断变化的法规和消费者期望,从而支持现有和新兴应用领域的持续需求。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 39亿美元 |

| 预测金额 | 59亿美元 |

| 复合年增长率 | 4.1% |

消费者对天然甜菜碱的偏好日益增长,这是影响市场动态的关键因素,其中甜菜衍生的甜菜碱越来越受欢迎,尤其是在永续性倡议和成分透明度影响购买决策和定价结构的地区。

到 2025 年,合成甜菜碱市占率将达到 54.8%。该领域继续受益于成本效益和扩充性的生产能力,从而支持其在价格竞争力和大量需求仍然至关重要的应用领域中得到广泛应用。

2025年,无水甜菜碱市占率达45.2%。这种无水结晶形式因其高浓度、优异的稳定性和与干粉製剂系统的相容性而备受青睐。其卓越的性能使其在营养补充剂、药品和饲料相关产品等众多应用领域拥有广泛的需求,在这些领域中,水分控制至关重要。

预计到2025年,北美甜菜碱市占率将达到28.8%。得益于完善的监管政策和多个应用领域稳定的需求,该地区拥有庞大的消费群体。消费者对洁净标示和天然成分日益增长的兴趣,并持续推动高级产品的普及。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 合成

- 自然的

- 光合成细菌

- 植物来源

- 动物源性

- 半合成

第六章 按类型分類的市场估算与预测,2022-2035年

- 无水甜菜碱

- 粉末

- 颗粒

- 盐酸甜菜碱

- 一水甜菜碱

- 结晶质

- 基于解决方案

7. 按纯度分類的市场估计与预测,2022-2035 年

- 高纯度

- 标准纯度

- 低纯度

- 客製化纯度

第八章 按应用领域分類的市场估算与预测,2022-2035年

- 动物饲料

- 家禽

- 猪

- 水产养殖

- 反刍动物

- 其他的

- 食品/饮料

- 麵包和糖果

- 运动营养与能量饮料

- 机能性食品

- 个人护理及化妆品

- 护肤

- 护髮

- 口腔清洁用品

- 製药

- 工业用途

- 化学中间体

- 清洁剂和界面活性剂

- 农业配方

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- AMINO GmbH

- BASF

- Kao Corporation

- Stepan Company

- Solvay

- Associated British Foods plc

- Nutreco

- The Lubrizol Corporation

- INOLEX, Inc.

- Sunwin Biotech Shandong Co., Ltd.

- Merck KGaA

- Evonik Industries AG

- Fengchen Group Co., Ltd.

- Orison Chemicals Limited

- Prasol Chemicals Limited

The Global Betaine Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 5.9 billion by 2035.

Market development is supported by the broadening use of betaine across multiple end-use industries, including nutrition-focused, consumer-oriented, and industrial sectors. Increasing recognition of betaine's functional versatility has strengthened its role as a key ingredient with nutritional, performance-enhancing, and formulation-related benefits. Long-term growth is reinforced by structural trends such as global population expansion, higher protein consumption linked to intensified animal production, and a growing shift toward ingredients perceived as natural and environmentally responsible. Scientific validation of betaine's functional value continues to strengthen confidence across commercial applications. The market outlook also reflects steady innovation efforts focused on refining formulations, improving production efficiency, and advancing purification methods. These developments are enabling suppliers to enhance product consistency, expand usage potential, and address evolving regulatory and consumer expectations, thereby supporting sustained demand across established and emerging application areas.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 4.1% |

Growing preference for naturally sourced betaine has become a major factor shaping market dynamics. Betaine derived from sugar beet sources is gaining increased traction, particularly in regions where sustainability credentials and ingredient transparency influence purchasing decisions and pricing structures.

The synthetic betaine segment held 54.8% share in 2025. This segment continues to benefit from cost efficiency and scalable production capabilities, which support its widespread use in applications where pricing competitiveness and volume requirements remain critical.

The betaine anhydrous segment held 45.2% share in 2025. This water-free crystalline form is valued for its high concentration, strong stability profile, and suitability for dry formulation systems. Its performance characteristics support demand across nutrition-focused, pharmaceutical, and feed-related product formats where moisture control is essential.

North America Betaine Market held 28.8% share in 2025. The region maintains a strong consumption base, supported by established regulatory clarity and consistent demand across multiple application segments. Consumer interest in clean-label and naturally positioned ingredients continues to support the adoption of premium products.

Key companies active in the Global Betaine Market include BASF, Associated British Foods plc, Evonik Industries AG, Stepan Company, AMINO GmbH, Nutreco, Solvay, INOLEX, Inc., Merck KGaA, The Lubrizol Corporation, Fengchen Group Co., Ltd., Kao Corporation, Sunwin Biotech Shandong Co., Ltd., Orison Chemicals Limited, and Prasol Chemicals Limited. Companies operating in the Global Betaine Market are strengthening their market position through a combination of product innovation, supply chain optimization, and strategic expansion. Many players are investing in advanced processing technologies to improve yield, purity, and formulation flexibility. Portfolio diversification is being used to address both cost-sensitive and premium demand segments. Firms are also focusing on sustainability initiatives, including responsible sourcing and reduced environmental impact, to align with evolving regulatory and consumer expectations. Geographic expansion and long-term partnerships with end-use industries are improving market reach and demand stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Synthetic

- 5.3 Natural

- 5.3.1 Photosynthetic Bacteria

- 5.3.2 Plant Sourced

- 5.3.3 Animal Sourced

- 5.4 Semi-synthetic

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 Betaine anhydrous

- 6.2.1 Powder

- 6.2.2 Granules

- 6.3 Betaine hydrochloride

- 6.4 Betaine monohydrate

- 6.4.1 Crystalline

- 6.4.2 Solution-based

Chapter 7 Market Estimates and Forecast, By Purity, 2022-2035 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 High purity

- 7.3 Standard purity

- 7.4 Low purity

- 7.5 Customized purity

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 Animal feed

- 8.2.1 Poultry

- 8.2.2 Swine

- 8.2.3 Aquaculture

- 8.2.4 Ruminants

- 8.2.5 Others

- 8.3 Food & beverages

- 8.3.1 Bakery & confectionery

- 8.3.2 Sports nutrition & energy drinks

- 8.3.3 Functional foods

- 8.4 Personal care & cosmetics

- 8.4.1 Skin care

- 8.4.2 Hair care

- 8.4.3 Oral care

- 8.5 Pharmaceuticals

- 8.6 Industrial applications

- 8.6.1 Chemical intermediates

- 8.6.2 Detergents & surfactants

- 8.6.3 Agricultural formulations

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion & Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AMINO GmbH

- 10.2 BASF

- 10.3 Kao Corporation

- 10.4 Stepan Company

- 10.5 Solvay

- 10.6 Associated British Foods plc

- 10.7 Nutreco

- 10.8 The Lubrizol Corporation

- 10.9 INOLEX, Inc.

- 10.10 Sunwin Biotech Shandong Co., Ltd.

- 10.11 Merck KGaA

- 10.12 Evonik Industries AG

- 10.13 Fengchen Group Co., Ltd.

- 10.14 Orison Chemicals Limited

- 10.15 Prasol Chemicals Limited

合成甜菜碱市场:依形态、产品等级、製程、应用及通路划分-全球预测,2026-2032年天然甜菜碱市场:2026-2032年全球市场预测(依原料、类型、形态、纯度等级、应用及通路划分)

合成甜菜碱市场:依形态、产品等级、製程、应用及通路划分-全球预测,2026-2032年天然甜菜碱市场:2026-2032年全球市场预测(依原料、类型、形态、纯度等级、应用及通路划分) 2026年全球甜菜碱市场报告

2026年全球甜菜碱市场报告 甜菜碱市场-全球产业规模、份额、趋势、机会、预测:按形状、类型、应用、地区和竞争格局划分,2021-2031年

甜菜碱市场-全球产业规模、份额、趋势、机会、预测:按形状、类型、应用、地区和竞争格局划分,2021-2031年 2025-2033年甜菜碱市场报告(依来源、产品类型、最终用途产业和地区)

2025-2033年甜菜碱市场报告(依来源、产品类型、最终用途产业和地区) 甜菜碱 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)

甜菜碱 -市场占有率分析、产业趋势/统计、成长预测(2025-2030) 甜菜碱市场:现况分析与预测(2024-2032)

甜菜碱市场:现况分析与预测(2024-2032) 天然甜菜碱的全球市场

天然甜菜碱的全球市场