|

市场调查报告书

商品编码

1928864

生质柴油及生质燃料加工设备市场机会、成长要素、产业趋势分析及预测(2026-2035)Biodiesel and Biofuels Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球生质柴油和生质燃料加工设备市场预计到 2025 年将达到 18.2 亿美元,预计到 2035 年将达到 30.9 亿美元,年复合成长率为 5.5%。

在全球各地,人们正积极反思如何开发和部署能源系统,以应对日益增长的净零排放目标压力。各国政府、企业和投资者正将目光从石化燃料转向可再生和低碳能源来源。推动这项转变的因素包括:气候变迁相关风险日益加剧、各产业对环境、社会和管治(ESG)课责的日益重视,以及持续的技术进步使可再生燃料在成本和性能方面更具竞争力。生质燃料被视为国家和产业脱碳策略的关键组成部分,尤其是在缺乏即时替代方案的地区。对高能量、相容燃料的需求正在加速成长,促使企业加大对新建生产设施和先进加工设备的投资。製造商优先考虑扩充性、高效且可靠的系统,以确保长期燃料供应安全,同时满足监管规定的混合比例和永续性目标。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 18.2亿美元 |

| 预测金额 | 30.9亿美元 |

| 复合年增长率 | 5.5% |

市场持续受益于对先进生产设备的投资增加,这些设备能够实现高产量和稳定的运作性能。生产商越来越倾向于寻求能够提高效率、增加产量并实现连续运作的系统。这项变更反映了更广泛的趋势,即向现代化设备配置转型,以提高运作柔软性和成本控制,从而使製造商能够有效地满足日益增长的全球燃料需求。

预计到2025年,反应器市场规模将达到6.44亿美元。这些系统仍然是生物柴油和生质燃料生产的核心,因为它们是生产设施中的核心处理单位。市场需求倾向于能够提供稳定条件、高转换效率和更高产量的解决方案。设备供应商不断开发先进的设计,这些设计超越了传统系统,能够实现连续运作、更好的製程控制和扩充性,从而满足工业级生产需求。

年产量超过5000万公升的大型商业设施在2025年占了45.4%的市场。这些工厂在满足政府的掺混规定以及向工业用户供应可再生燃料方面发挥关键作用。实现全年不间断运作需要先进的工程技术、可靠的设备以及强大的原材料采购物流支援。大规模生产降低了单位成本,使生质燃料与传统燃料相比更具竞争力。

预计到2025年,北美生质柴油和生质燃料加工设备市场将占据77.2%的市场份额,市场规模达4.751亿美元。联邦和州政府的激励措施持续支持无污染燃料的推广应用,鼓励生产者扩大产能。随着商业营运商建设规模更大的生产设施,为满足可再生燃料标准和日益增长的替代燃料应用需求,相关设备的需求也不断上升。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 全球脱碳和能源转型

- 政府混合义务和政策奖励

- 扩大先进生质燃料(HVO、SAF)的引进

- 产业潜在风险与挑战

- 高昂的资本成本

- 基础设施和供应链中的脆弱性

- 机会

- 先进生质燃料工厂扩建

- 航空和航运业可再生燃料的成长

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过装置

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依设备类型分類的市场估算与预测(2022-2035 年)

- 热交换器

- 製程冷却和加热热交换器

- 甲醇回收热交换器

- 甘油加工热交换器

- 每套热交换器单元的管体积

- 蒸馏塔

- 甲醇精炼塔

- 甘油精炼塔

- 原料预处理塔

- 每塔管数

- 蒸发浓缩系统

- 甲醇闪蒸器

- 降膜蒸发器

- 反应炉

第六章 市场估算与预测:依材质(2022-2035 年)

- 304/304L不銹钢管

- 316/316L不銹钢管

- 双相和超双相不銹钢管

- 钛管

- 镍合金及其他材质

第七章 市场估计与预测:依应用领域划分(2022-2035 年)

- 甲醇回收提纯系统

- 甘油回收纯化系统

- 原料预处理和製备

- 酯交换反应的温度控管

- 生质柴油/FAMA冷却和表面处理工程

- 可再生柴油(HVO/HEFA)高压系统

第八章 依最终用途规模分類的市场估算与预测(2022-2035 年)

- 大型商业工厂(年产量超过5000万公升)

- 中型区域性工厂(年产1000万至5000万公升)

- 小规模分散式生产(年产量低于1000万公升)

- 农场和合作生物柴油系统

第九章 按分销管道分類的市场估计和预测(2022-2035 年)

- 直销

- 间接销售

第十章 各地区市场估计与预测(2022-2035 年)

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章 公司简介

- Advance Biofuel

- Alfa Laval

- American Crane &Equipment

- ANDRITZ

- CPM Crown

- Desmet

- Ecolab

- Florida Biodiesel

- JBT

- Myande

- N&T Engitech

- S. Howes

- Springboard Biodiesel

- SRS International

- Sulzer

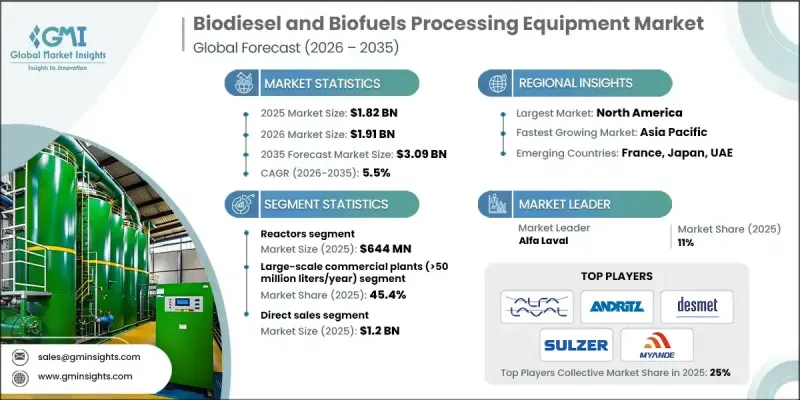

The Global Biodiesel and Biofuels Processing Equipment Market was valued at USD 1.82 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 3.09 billion by 2035.

Communities worldwide are actively reassessing how energy systems are developed and deployed as pressure increases to achieve net-zero targets. Governments, corporations, and investors are shifting their focus away from fossil fuel dependency and toward renewable and low-carbon energy sources. This transition is driven by increasing climate-related risks, stronger ESG accountability across industries, and continuous technological improvements that allow renewable fuels to compete on cost and performance. Biofuels are positioned as essential components in national and sector-specific decarbonization strategies, especially where immediate alternatives remain limited. Demand is accelerating in industries that require high-energy, compatible fuels, which is leading to greater investment in new production facilities and advanced processing equipment. Manufacturers are prioritizing scalable, efficient, and reliable systems that can support long-term fuel supply stability while meeting regulatory blending mandates and sustainability objectives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.82 Billion |

| Forecast Value | $3.09 Billion |

| CAGR | 5.5% |

The market continues to benefit from rising investment in advanced production equipment designed to support higher throughput and consistent operational performance. Producers increasingly demand systems that improve efficiency, enhance output, and support continuous operation. This shift reflects a broader move toward modernized equipment configurations that deliver operational flexibility and improved cost control, allowing manufacturers to respond more effectively to growing global fuel demand.

The reactors segment generated USD 644 million in 2025. These systems remain central to biodiesel and biofuel manufacturing, as they serve as the core processing units within production facilities. Market demand favors solutions that deliver stable conditions, higher conversion efficiency, and increased output volumes. Equipment suppliers continue to develop advanced designs that outperform traditional systems by enabling continuous operation, better process control, and greater scalability to meet industrial-level production requirements.

The large-scale commercial facilities with annual output exceeding 50 million liters accounted for 45.4% share in 2025. These plants play a vital role in meeting government blending mandates while supplying renewable fuels to industrial consumers. Their ability to operate continuously throughout the year requires sophisticated engineering, dependable equipment, and strong logistics support for feedstock sourcing. High-volume production allows these facilities to achieve lower per-unit costs, making biofuels increasingly competitive with conventional fuels.

North America Biodiesel and Biofuels Processing Equipment Market held 77.2% share and generated USD 475.1 million in 2025. Federal and state-level incentives continue to support the adoption of cleaner fuels, encouraging producers to expand capacity. Equipment demand is rising as commercial operators develop large production facilities to comply with renewable fuel standards and respond to increasing interest in alternative fuel applications.

Key companies operating in the Global Biodiesel and Biofuels Processing Equipment Market include Alfa Laval, ANDRITZ, Desmet, Sulzer, Myande, CPM Crown, JBT, SRS International, N&T Engitech, Advance Biofuel, Florida Biodiesel, Springboard Biodiesel, American Crane & Equipment, S. Howes, and Ecolab. Companies in the Global Biodiesel and Biofuels Processing Equipment Market focus on capacity expansion, technology upgrades, and strategic partnerships to strengthen their market position. Many manufacturers invest heavily in research and development to improve the efficiency, durability, and scalability of equipment. Firms also emphasize customization to meet regional regulatory requirements and diverse feedstock conditions. Strategic collaborations with fuel producers help suppliers secure long-term contracts and improve product validation. Expansion into emerging markets allows companies to capture new demand driven by sustainability mandates.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment Type

- 2.2.3 Material Type

- 2.2.4 Application

- 2.2.5 End use scale

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global decarbonization & energy transition

- 3.2.1.2 Government blend mandates & policy incentives

- 3.2.1.3 Rising adoption of advanced biofuels (HVO, SAF)

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital costs

- 3.2.2.2 Infrastructure & supply chain weaknesses

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of advanced biofuel plants

- 3.2.3.2 Growth in aviation & marine renewable fuels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter';s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Heat exchangers

- 5.2.1 Process cooling/heating heat exchangers

- 5.2.2 Methanol recovery heat exchangers

- 5.2.3 Glycerin processing heat exchangers

- 5.2.4 Tube content per heat exchanger unit

- 5.3 Distillation columns

- 5.3.1 Methanol rectification columns

- 5.3.2 Glycerin purification columns

- 5.3.3 Feedstock pre-treatment columns

- 5.3.4 Tube content per column

- 5.4 Evaporation & concentration systems

- 5.4.1 Methanol flash evaporators

- 5.4.2 Falling film evaporators

- 5.5 Reactors

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Stainless steel 304/304l tubes

- 6.3 Stainless steel 316/316L tubes

- 6.4 Duplex and super duplex stainless-steel tubes

- 6.5 Titanium tubes

- 6.6 Nickel alloys and other materials

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Methanol recovery and purification systems

- 7.3 Glycerin recovery and purification systems

- 7.4 Feedstock pre-treatment and preparation

- 7.5 Transesterification reaction thermal management

- 7.6 Biodiesel/FAMA cooling and finishing

- 7.7 Renewable diesel (HVO/HEFA) high-pressure systems

Chapter 8 Market Estimates and Forecast, By End Use Scale, 2022 - 2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Large-scale commercial plants (>50 million liters/year)

- 8.3 Mid-scale regional plants (10-50 million liters/year)

- 8.4 Small-scale and distributed production (<10 million liters/year)

- 8.5 On-farm and cooperative biodiesel systems

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Advance Biofuel

- 11.2 Alfa Laval

- 11.3 American Crane & Equipment

- 11.4 ANDRITZ

- 11.5 CPM Crown

- 11.6 Desmet

- 11.7 Ecolab

- 11.8 Florida Biodiesel

- 11.9 JBT

- 11.10 Myande

- 11.11 N&T Engitech

- 11.12 S. Howes

- 11.13 Springboard Biodiesel

- 11.14 SRS International

- 11.15 Sulzer

2026年全球生质燃料市场报告2026年全球生质燃料检测服务市场报告

2026年全球生质燃料市场报告2026年全球生质燃料检测服务市场报告 沼气检测服务市场(按原始类型、检测类型、服务模式、最终用途产业和应用划分)—2026-2032年全球预测生物甲烷检测服务市场(依光谱法、层析法、服务组合和应用领域划分)-全球预测,2026-2032年

沼气检测服务市场(按原始类型、检测类型、服务模式、最终用途产业和应用划分)—2026-2032年全球预测生物甲烷检测服务市场(依光谱法、层析法、服务组合和应用领域划分)-全球预测,2026-2032年 生质燃料:全球市场份额和排名、总收入和需求预测(2025-2031 年)

生质燃料:全球市场份额和排名、总收入和需求预测(2025-2031 年) 铁路生质燃料市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测

铁路生质燃料市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测 B5燃料市场规模、份额和成长分析(按原料、应用和地区划分)-产业预测(2026-2033年)

B5燃料市场规模、份额和成长分析(按原料、应用和地区划分)-产业预测(2026-2033年) 生质燃料:全球市场

生质燃料:全球市场 生质燃料能源·原料设备的全球市场(2025年),终端用户,类型,竞争企业:分析与预测

生质燃料能源·原料设备的全球市场(2025年),终端用户,类型,竞争企业:分析与预测 生物热能燃料市场:依混合比例、配销通路、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

生物热能燃料市场:依混合比例、配销通路、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测