|

市场调查报告书

商品编码

1928882

可再生柴油市场机会、成长要素、产业趋势分析及预测(2026-2035)Renewable Diesel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

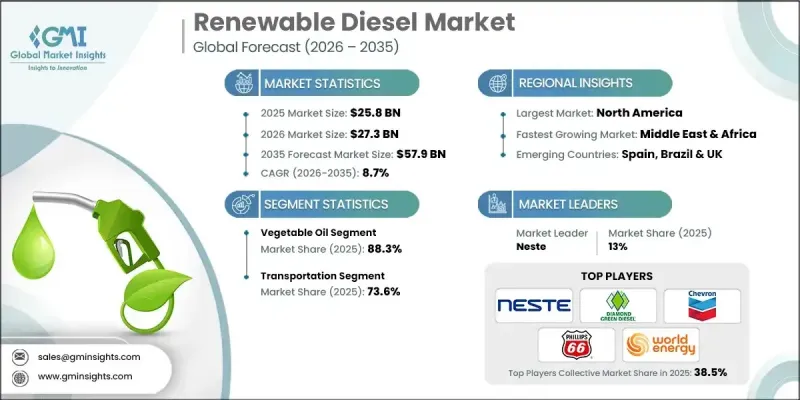

全球可再生柴油市场预计到 2025 年价值 258 亿美元,到 2035 年将达到 579 亿美元,年复合成长率为 8.7%。

全球对低生命週期温室气体排放燃料的需求不断增长,并持续加速此类燃料的普及。可再生柴油因其与现有柴油引擎和燃料分配系统的兼容性而备受关注,无需大量资本投资即可实现平稳过渡。各国政府、各产业和车队营运商日益重视兼顾排放和运作可靠性的能源解决方案。可再生柴油被视为增强燃料安全、应对气候变迁的策略选择。有利的法规结构,加上原油市场波动和地缘政治不确定性,进一步凸显了对多元化、国产替代燃料的需求。可再生柴油卓越的性能特性以及在不牺牲效率的前提下满足监管和企业永续性要求的能力,吸引了能源生产商的日益关注,进一步推动了市场发展。这些因素共同促成了可再生柴油在全球转型为低碳能源系统的核心地位。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 258亿美元 |

| 预测金额 | 579亿美元 |

| 复合年增长率 | 8.7% |

可再生柴油是一种利用生物质资源生产的低碳燃料,其化学性质与传统柴油相同。这使得现有基础设施能够立即投入使用,同时有助于实现排放和增强能源韧性的目标。政策支持和监管奖励持续推动再生柴油在多个终端用户领域的研发和应用,旨在减少对石油基燃料的依赖。

预计到2025年,植物油原料市占率将达到88.3%,到2035年将以9.9%的复合年增长率成长。对可再生和永续原料日益增长的需求将支撑该领域的持续主导地位,因为这些原料符合脱碳目标,并且当采用先进的炼油技术加工时,其性能特征可与传统柴油燃料相媲美。

2025年,交通运输领域占73.6%的市场份额,预计2026年至2035年将以8.5%的复合年增长率成长。车队营运商正越来越多地采用可再生柴油,以在满足排放目标的同时,保持可靠性和性能标准。监管合规和企业永续性措施持续推动该应用领域的需求成长。

预计到 2025 年,美国可再生柴油市场将占市场份额的 90.3%,到 2035 年将成长至 263 亿美元。强有力的政策支持和法规结构继续推动多个行业采用低碳燃料,从而加强了可再生柴油作为石油基燃料可行替代品的地位。

目录

第一章调查方法和范围

- 初步研究和检验

- 部分原始资讯(但不限于此)

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 调查过程和评估因素

- 研究轨迹的要素

- 评分组成部分

- 有关研究透明度的更多信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

- 市场定义

第二章执行摘要

第三章业界考察

- 产业生态系统

- 原物料供应及采购分析

- 製造能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 成本结构分析

- 波特分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

- 新的机会与趋势

- 数位化和物联网集成

- 拓展新兴市场

- 投资分析及未来展望

第四章 竞争情势

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 战略仪錶板

- 策略倡议

- 企业标竿管理

- 创新与科技趋势

第五章 市场规模及预测:依原料划分,2021-2034年

- 动物脂肪和油脂

- 植物油

- 其他的

第六章 依应用领域分類的市场规模及预测(2021-2034年)

- 运输

- 发电

- 其他的

第七章 2021-2034年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 西班牙

- 英国

- 义大利

- 亚太地区

- 中国

- 印度

- 印尼

- 澳洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第八章:公司简介

- BP

- Cargill

- Carolina Renewable Products

- Chevron

- Diamond Green Diesel

- Eni

- Gevo

- HollyFrontier

- Imperial Oil

- LanzaJet

- Marathon Petroleum

- Neste

- Petrobras

- Phillips 66

- Preem AB

- Repsol

- Shell

- TotalEnergies

- Valero

- World Energy

The Global Renewable Diesel Market was valued at USD 25.8 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 57.9 billion by 2035.

Rising global demand for fuels with lower lifecycle greenhouse gas emissions is continuing to accelerate their adoption. Renewable diesel gains strong momentum due to its compatibility with existing diesel engines and fuel distribution systems, which supports a smooth transition without requiring large capital investments. Governments, industries, and fleet operators increasingly prioritize energy solutions that balance emissions reduction with operational reliability. Renewable diesel is positioned as a strategic option for enhancing fuel security while addressing climate commitments. Supportive regulatory frameworks, combined with volatile crude oil markets and geopolitical uncertainty, reinforce the need for diversified and domestically sourced fuel alternatives. The market also benefits from growing interest among energy producers due to renewable diesel's strong performance characteristics and its ability to meet regulatory and corporate sustainability requirements without compromising efficiency. These combined factors establish renewable diesel as a central component of the global transition toward lower-carbon energy systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $25.8 Billion |

| Forecast Value | $57.9 Billion |

| CAGR | 8.7% |

Renewable diesel is described as a low-carbon fuel produced from biomass-based resources and offers chemical equivalence to conventional diesel. This allows immediate use across existing infrastructure while supporting emissions reduction and energy resilience goals. Policy support and regulatory incentives continue to strengthen development activity and encourage adoption across multiple end-use sectors seeking to reduce dependence on petroleum-based fuels.

The vegetable oil feedstock segment accounted for 88.3% share in 2025 and is projected to grow at a CAGR of 9.9% through 2035. Rising demand for renewable and sustainable inputs supports the continued dominance of this segment, as such feedstocks align with decarbonization objectives and deliver performance characteristics comparable to traditional diesel when processed through advanced refining technologies.

The transportation segment held 73.6% share in 2025 and is forecast to grow at a CAGR of 8.5% from 2026 to 2035. Fleet operators increasingly adopt renewable diesel to meet emissions targets while maintaining reliability and performance standards. Regulatory compliance and corporate sustainability commitments continue to strengthen demand within this application segment.

United States Renewable Diesel Market held 90.3% share in 2025 and is expected to generate USD 26.3 billion by 2035. Strong policy support and regulatory frameworks continue to incentivize low-carbon fuel adoption across multiple industries, reinforcing renewable diesel's role as a practical alternative to petroleum-based fuels.

Prominent companies active in the Global Renewable Diesel Market include Neste, Valero, Chevron, Shell, World Energy, TotalEnergies, BP, Phillips 66, Marathon Petroleum, Repsol, Diamond Green Diesel, Preem AB, Cargill, Eni, Gevo, Imperial Oil, Petrobras, LanzaJet, HollyFrontier, and Carolina Renewable Products. Companies operating in the Renewable Diesel Market strengthen their market position through capacity expansion, strategic partnerships, and investment in advanced refining technologies. Many players focus on securing long-term feedstock supply agreements to ensure production stability and cost control. Geographic expansion and integration across the value chain help improve market access and resilience. Firms also emphasize regulatory compliance and certification to align with evolving sustainability standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.1.1.1 Mathematical impact of growth parameters on forecast

- 1.3.1.1 Quantified market impact analysis

- 1.3.2 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Feedstock trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Porter';s analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Feedstock, 2021 - 2034 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Animal Fat

- 5.3 Vegetable Oil

- 5.4 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Transportation

- 6.3 Power Generation

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & MT)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Spain

- 7.3.4 UK

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Indonesia

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 BP

- 8.2 Cargill

- 8.3 Carolina Renewable Products

- 8.4 Chevron

- 8.5 Diamond Green Diesel

- 8.6 Eni

- 8.7 Gevo

- 8.8 HollyFrontier

- 8.9 Imperial Oil

- 8.10 LanzaJet

- 8.11 Marathon Petroleum

- 8.12 Neste

- 8.13 Petrobras

- 8.14 Phillips 66

- 8.15 Preem AB

- 8.16 Repsol

- 8.17 Shell

- 8.18 TotalEnergies

- 8.19 Valero

- 8.20 World Energy

生物柴油市场机会、成长要素、产业趋势分析及2026-2035年预测

生物柴油市场机会、成长要素、产业趋势分析及2026-2035年预测 2026-2034年全球生物柴油催化剂市场规模、份额、趋势和成长分析报告全球生物柴油市场规模、份额、趋势和成长分析报告(2026-2034年)

2026-2034年全球生物柴油催化剂市场规模、份额、趋势和成长分析报告全球生物柴油市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球绿色柴油市场报告2026年全球可再生柴油市场报告2026年全球生质柴油市场报告生质柴油市场-2026-2031年预测

2026年全球绿色柴油市场报告2026年全球可再生柴油市场报告2026年全球生质柴油市场报告生质柴油市场-2026-2031年预测 可再生柴油市场规模、份额和成长分析(按类型、原料、应用、最终用户和地区划分)-2026-2033年产业预测

可再生柴油市场规模、份额和成长分析(按类型、原料、应用、最终用户和地区划分)-2026-2033年产业预测 日本生质柴油市场报告:按原料、应用、类型、生产技术和地区划分(2026-2034 年)

日本生质柴油市场报告:按原料、应用、类型、生产技术和地区划分(2026-2034 年) 生质柴油:全球市场占有率和排名、总销售量和需求预测(2025-2031年)

生质柴油:全球市场占有率和排名、总销售量和需求预测(2025-2031年)