|

市场调查报告书

商品编码

1928884

电子陶瓷市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Electronic Ceramics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

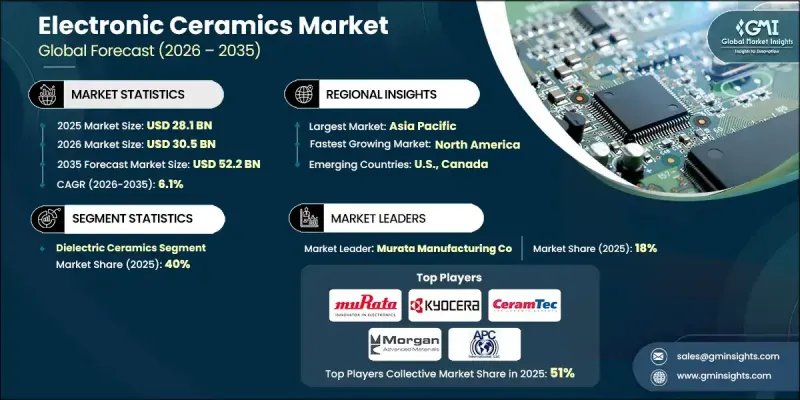

全球电子陶瓷市场预计到 2025 年将达到 281 亿美元,到 2035 年将达到 522 亿美元,年复合成长率为 6.1%。

市场成长主要受先进电子产品、高速连接、电动化交通以及电力基础设施升级的持续推动。互联设备的大规模生产持续驱动着对具有讯号完整性、高能效和热稳定性的陶瓷基元件的需求。无线通讯和下一代网路的进步提高了高频和微波应用对陶瓷材料的性能要求。汽车产业的长期需求也不断增强,因为电动驱动系统、电力电子和充电系统需要能够在高压高温环境下工作的陶瓷基板和绝缘体。工业电力系统、电网现代化和自动化解决方案也透过在绝缘、储能和控制系统中采用陶瓷材料来推动市场成长。亚太地区约占全球市场价值的60%,主要得益于其电子製造业的集中度。同时,北美和欧洲则专注于高可靠性、专业应用的高价值产品。持续的微型化、不断发展的储存技术、汽车电气化以及法规主导的材料创新不断拓展应用领域。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 281亿美元 |

| 预测金额 | 522亿美元 |

| 复合年增长率 | 6.1% |

按产品类型,到2025年,介电陶瓷将占据40%的市场份额,这主要得益于对积层陶瓷电容、共振器和高频元件的强劲需求。磁性陶瓷材料将占约15%的市场份额,这主要得益于其在电感元件、电磁干扰对抗措施和先进通讯系统中的应用。

家用电子电器和家用电器是主要的终端应用领域,消耗大量陶瓷元件,这些元件广泛应用于连网设备、智慧系统和数位家电。智慧互联和高效能消费品的日益普及,持续推动对紧凑可靠陶瓷材料的需求,这些材料能够支援讯号处理、能量储存和温度控管。

受製造业回流计画、半导体和先进製造业激励措施以及电动车产量成长的推动,美国电子陶瓷市场预计到2025年将达到61亿美元,到2035年将接近120亿美元。该地区对航太、医疗技术、国防和先进电力电子等高可靠性应用的重视,也促使平均售价上涨,并增加了对供应链安全的投资。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

5. 2022-2035年按产品类型分類的电子陶瓷市场

- 铁电陶瓷

- 压电陶瓷

- 热电陶瓷

- 介电陶瓷

- 磁性陶瓷

- 绝缘和基板陶瓷

- 用于电极的导电陶瓷

- 其他的

6. 2022-2035年电子陶瓷市场(按类型划分)

- 块状陶瓷

- 薄膜

- 粉末

- 奈米颗粒

- 复合材料

7. 2022-2035年按终端应用产业分類的电子陶瓷市场

- 家用电器/家用电子电器

- 卫生保健

- 汽车和运输设备

- 电讯和电力传输

- 航太/国防

- 工业自动化和电力电子

- 能源与发电

- 物联网和穿戴式装置

- 其他的

第八章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- APC International

- CeramTec Holding

- Central Electronics

- Kyocera Corporation

- Maruwa

- Morgan Advanced Materials

- Murata Manufacturing

- PI Ceramics

- Sensor Technology

- Sparkler Ceramics

The Global Electronic Ceramics Market was valued at USD 28.1 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 52.2 billion by 2035.

Market growth is supported by the continued expansion of advanced electronics, high-speed connectivity, electrified mobility, and power infrastructure upgrades. Large-scale production of connected devices drives sustained demand for ceramic-based components that enable signal integrity, energy efficiency, and thermal stability. Advancements in wireless communication and next-generation networks are increasing performance requirements for ceramic materials used in high-frequency and microwave applications. The automotive sector is reinforcing long-term demand as electric drivetrains, power electronics, and charging systems rely on ceramic substrates and insulators capable of operating at higher voltages and temperatures. Industrial power systems, grid modernization, and automation solutions further contribute to market expansion using ceramic materials for insulation, energy storage, and control systems. Asia Pacific represents nearly 60% of global market value due to its concentration of electronics manufacturing, while North America and Europe remain focused on high-reliability and specialty applications with premium pricing. Ongoing miniaturization, evolving memory technologies, automotive electrification, and regulatory-driven material innovation continue to widen application opportunities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $28.1 Billion |

| Forecast Value | $52.2 Billion |

| CAGR | 6.1% |

By product category, the dielectric ceramics accounted for 40% share in 2025, supported by strong demand for multilayer ceramic capacitors, resonators, and radio-frequency components. Magnetic ceramic materials held close to 15% of the market, driven by their use in inductive components, electromagnetic interference control, and advanced communication systems.

The consumer electronics and home appliances represented the leading end-use segment, consuming high volumes of ceramic components used across connected devices, smart systems, and digital appliances. Growing adoption of intelligent, connected, and high-performance consumer products continues to stimulate demand for compact, reliable ceramic materials that support signal processing, energy storage, and heat management.

U.S. Electronic Ceramics Market reached USD 6.1 billion in 2025 and is expected to approach USD 12 billion by 2035, supported by reshoring initiatives, incentives for semiconductor and advanced manufacturing, and growth in electric vehicle production. The region emphasizes high-reliability applications across aerospace, medical technology, defense, and advanced power electronics, contributing to higher average selling prices and increased investment in supply chain security.

Key companies active in the Global Electronic Ceramics Market include Murata Manufacturing, Kyocera Corporation, CeramTec Holding, Morgan Advanced Materials, Maruwa, APC International, PI Ceramics, Sparkler Ceramics, Central Electronics, and Sensor Technology. Companies in the Global Electronic Ceramics Market are strengthening their market position by investing in advanced material research to improve dielectric performance, thermal conductivity, and reliability. Many players are expanding production capacity and regional manufacturing footprints to support supply chain resilience and meet local sourcing requirements. Strategic collaborations with electronics, automotive, and energy system manufacturers enable early integration into next-generation designs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Form factor

- 2.2.3 End use industry

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Electronic Ceramics Market, By Product Type, 2022-2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Ferroelectric ceramics

- 5.3 Piezoelectric ceramics

- 5.4 Pyroelectric ceramics

- 5.5 Dielectric ceramics

- 5.6 Magnetic ceramics

- 5.7 Insulating & substrate ceramics

- 5.8 Conductive & electrode ceramics

- 5.9 Others

Chapter 6 Electronic Ceramics Market, By Form Factor, 2022-2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Bulk ceramics

- 6.3 Thin films

- 6.4 Powders

- 6.5 Nanoparticles

- 6.6 Composite materials

Chapter 7 Electronic Ceramics Market, By End Use Industry, 2022-2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Home appliances & consumer electronics

- 7.3 Healthcare

- 7.4 Automotive & transportation

- 7.5 Telecommunication & power transmission

- 7.6 Aerospace & defense

- 7.7 Industrial automation & power electronics

- 7.8 Energy & power generation

- 7.9 IoT & wearables

- 7.10 Others

Chapter 8 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 APC International

- 9.2 CeramTec Holding

- 9.3 Central Electronics

- 9.4 Kyocera Corporation

- 9.5 Maruwa

- 9.6 Morgan Advanced Materials

- 9.7 Murata Manufacturing

- 9.8 PI Ceramics

- 9.9 Sensor Technology

- 9.10 Sparkler Ceramics

电陶瓷市场:按产品类型、功能和最终用途产业划分-2026-2032年全球市场预测

电陶瓷市场:按产品类型、功能和最终用途产业划分-2026-2032年全球市场预测 电子陶瓷市场分析及预测(至2035年):依类型、产品、应用、材料类型、技术、组件、最终用户、功能及设备划分

电子陶瓷市场分析及预测(至2035年):依类型、产品、应用、材料类型、技术、组件、最终用户、功能及设备划分 2026年全球电子陶瓷市场报告2026年全球电气和电子陶瓷市场报告

2026年全球电子陶瓷市场报告2026年全球电气和电子陶瓷市场报告 电子电气陶瓷市场规模、份额及成长分析(依陶瓷类型、应用、形状及地区划分)-2026-2033年产业预测

电子电气陶瓷市场规模、份额及成长分析(依陶瓷类型、应用、形状及地区划分)-2026-2033年产业预测 电子陶瓷市场规模、份额和成长分析(按陶瓷类型、应用、形状、最终用户和地区划分)-2026-2033年产业预测电子电气陶瓷市场按产品类型、原料、应用和製造流程划分-2025-2032年全球预测

电子陶瓷市场规模、份额和成长分析(按陶瓷类型、应用、形状、最终用户和地区划分)-2026-2033年产业预测电子电气陶瓷市场按产品类型、原料、应用和製造流程划分-2025-2032年全球预测 全球电子陶瓷市场

全球电子陶瓷市场 2025 年至 2033 年电子陶瓷市场规模、份额、趋势及预测(按材料、应用、最终用户和地区)

2025 年至 2033 年电子陶瓷市场规模、份额、趋势及预测(按材料、应用、最终用户和地区)