|

市场调查报告书

商品编码

1928905

丁酮市场机会、成长要素、产业趋势分析及2026年至2035年预测Methyl Ethyl Ketone (MEK) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

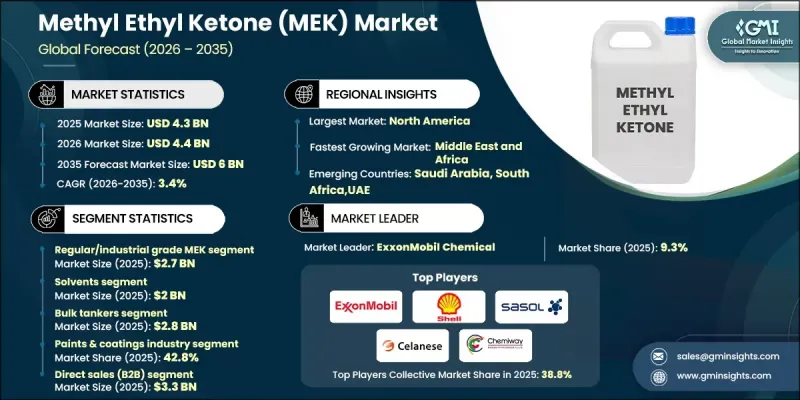

全球丁酮(MEK) 市场预计到 2025 年将达到 43 亿美元,到 2035 年将达到 60 亿美元,年复合成长率为 3.4%。

甲基乙基酮(MEK,俗称丁酮)是一种无色、易挥发的液体,具有刺鼻的甜味,且易燃。它因其优异的溶解性、快速的挥发速率以及溶解树脂、涂料、黏合剂和油墨的能力而广为人知。市场成长主要由涂料、黏合剂、印刷油墨、橡胶加工和化学品製造等行业的需求所驱动。建筑、汽车製造和包装等新兴产业的蓬勃发展也支撑着持续的消费,并推动着市场的稳定扩张。区域成长率因生产密度、环境法规和溶剂替代趋势而异。为了保持竞争力,供应商正致力于建立可靠的供应链、提高成本效益并遵守安全和环境标准。 MEK 仍然是各种製造领域中表面涂层、保护性涂料和特殊化学品应用的重要工业溶剂。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 43亿美元 |

| 预测金额 | 60亿美元 |

| 复合年增长率 | 3.4% |

预计到 2025 年,商用或工业级 MEK 市场将创造 27 亿美元的收入。工业级 MEK 因其多功能性和通用性能,被广泛应用于涂料、黏合剂和清洁工艺等领域;电子级 MEK 专为半导体製造和电路清洁等高纯度应用而设计;而医药级 MEK 则符合製药生产所需的严格纯度和安全标准。

根据包装类型,散装罐车运输市场预计到2025年将达到28亿美元。散装罐车为需要大量甲基乙基酮(MEK)的大型工业买家提供经济高效的运输和装卸方案。中型散货箱(IBC)兼具容量和便利性,被中型企业广泛用于简化储存和物流。

预计2025年北美丁酮(MEK)市场规模将达22亿美元,2035年将达31亿美元。该地区市场受到严格的环境法规的影响,这些法规推动了挥发性有机化合物(VOC)排放的减少和清洁溶剂的采用。成熟的工业基础使涂料、黏合剂和化学品製造业对MEK的需求保持稳定,但随着製造商寻求替代溶剂以应对监管压力,其成长速度正在放缓。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 油漆和涂料行业的需求不断增长

- 扩大製造业活动

- 汽车和航太领域的成长

- 产业潜在风险与挑战

- 原物料价格波动

- 极易燃且易挥发

- 市场机会

- 开发低排放、永续的MEK等级

- 扩展包装与展示应用

- 引入溶剂回收和循环系统

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按年级

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 各等级市场估算与预测,2022-2035年

- 通用/工业级甲基乙基酮

- 电子级甲基乙基酮

- 医药级MEK

- 胺甲酸乙酯级MEK

- ACS试剂级MEK

- 高效液相层析级甲乙酮

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 溶剂

- 油性漆和乳胶漆用防结皮剂

- 黏合剂和密封剂

- 印刷油墨

- 树脂

- 化学中间体

- 其他的

第七章 依包装类型分類的市场估计与预测,2022-2035年

- 散货(油轮)

- 中型散货箱(IBC)

- 鼓

- 水桶和小容器

- 特殊包装

8. 2022-2035年按最终用途产业分類的市场估算与预测

- 油漆和涂料行业

- 车

- 建造

- 包装

- 电子和半导体

- 药品和医疗保健

- 航太

- 纺织皮革业

- 橡胶工业

- 其他的

9. 2022-2035年按分销管道分類的市场估算与预测

- 直销(B2B)

- 线上平台/电子商务

- 其他的

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十一章:公司简介

- Arkema SA

- Genomatica

- LanzaTech(Carbon Capture to Chemicals)

- Vertec Biosolvents

- Celanese Corporation

- Cetex Petrochemicals

- Eastman Chemical Company

- ExxonMobil Corporation

- INEOS Group

- Idemitsu Kosan Co., Ltd.

- LG Chem Ltd.

- Maruzen Petrochemical Co., Ltd.

- Nouryon

- PTT Global Chemical Public Company Limited

- Sasol Limited

- Shell Chemicals(Shell Plc)

- Solvay SA

- SK Energy

- PetroChina Company Limited

- Mitsubishi Chemical Corporation

The Global Methyl Ethyl Ketone (MEK) Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 3.4% to reach USD 6 billion by 2035.

MEK, commonly known as butanone, is a colorless, highly volatile liquid with a sharp, sweet odor and flammable properties. It is widely recognized for its excellent solvency, rapid evaporation, and capacity to dissolve resins, coatings, adhesives, and inks. The market growth is primarily fueled by demand from industries such as paints and coatings, adhesives, printing inks, rubber processing, and chemical manufacturing. Expanding sectors, including construction, automotive production, and packaging, are supporting sustained consumption, driving steady market expansion. Regional growth varies due to manufacturing density, environmental regulations, and trends toward solvent substitution. To stay competitive, suppliers focus on reliable supply chains, cost efficiency, and compliance with safety and environmental standards. MEK remains an essential industrial solvent for surface coatings, protective finishes, and specialized chemical applications across diverse manufacturing sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $6 Billion |

| CAGR | 3.4% |

The regular or industrial-grade MEK segment generated USD 2.7 billion in 2025. Industrial-grade MEK is preferred for broad applications, including coatings, adhesives, and cleaning processes, due to its versatile, general-purpose performance. In contrast, electronic-grade MEK is tailored for high-purity applications in semiconductor production and circuit cleaning, while pharmaceutical-grade MEK meets the stringent purity and safety standards required for drug manufacturing.

In terms of packaging, the bulk tankers segment reached USD 2.8 billion in 2025. Bulk tankers serve large industrial buyers needing high volumes of MEK, offering cost-effective transportation and handling. Intermediate Bulk Containers (IBCs) provide a balance between volume and convenience, widely used in medium-scale operations for easier storage and logistics.

North America Methyl Ethyl Ketone (MEK) Market accounted for USD 2.2 billion in 2025 and is projected to reach USD 3.1 billion by 2035. The market in this region is influenced by stringent environmental regulations, driving lower VOC emissions and cleaner solvent adoption. A mature industrial base ensures stable demand for MEK in coatings, adhesives, and chemical manufacturing, though growth is moderated as manufacturers explore alternative solvents in response to regulatory pressures.

Key players in the Global Methyl Ethyl Ketone (MEK) Market include Celanese Corporation, Solvay S.A., Arkema S.A., Eastman Chemical Company, ExxonMobil Corporation, Genomatica, LanzaTech (Carbon Capture to Chemicals), SK Energy, PTT Global Chemical Public Company Limited, Vertec Biosolvents, Idemitsu Kosan Co., Ltd., LG Chem Ltd., Maruzen Petrochemical Co., Ltd., Sasol Limited, Shell Chemicals (Shell Plc), PetroChina Company Limited, Nouryon, Cetex Petrochemicals, and Mitsubishi Chemical Corporation. Companies in the Global Methyl Ethyl Ketone (MEK) Market strengthen their presence through strategic investments in production efficiency, sustainability, and technological innovation. Manufacturers focus on expanding production capacity while optimizing cost structures to remain competitive. Research and development initiatives target cleaner solvent alternatives, improved solvent performance, and regulatory compliance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Purity Grade

- 2.2.2 Application

- 2.2.3 Packaging Type

- 2.2.4 End Use Industry

- 2.2.5 Distribution Channel

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from paints and coatings industry

- 3.2.1.2 Expansion of manufacturing activities

- 3.2.1.3 Automotive and aerospace sector growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 High flammability and volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Development of low-emission and sustainable MEK grades

- 3.2.3.2 Expansion in packaging and labeling applications

- 3.2.3.3 Adoption of solvent recovery and recycling systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By grade

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Regular/Industrial Grade MEK

- 5.3 Electronic grade MEK

- 5.4 Pharmaceutical grade MEK

- 5.5 Urethane grade MEK

- 5.6 ACS reagent grade MEK

- 5.7 HPLC grade MEK

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvents

- 6.3 Anti-skinning agent in oil/latex paints

- 6.4 Adhesives & sealants

- 6.5 Printing inks

- 6.6 Resins

- 6.7 Chemical intermediates

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bulk (tankers)

- 7.3 Intermediate bulk container (IBC)

- 7.4 Drums

- 7.5 Pails & small containers

- 7.6 Specialty packaging

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Paints & coatings industry

- 8.3 Automotive

- 8.4 Construction

- 8.5 Packaging

- 8.6 Electronics & semiconductors

- 8.7 Pharmaceuticals & healthcare

- 8.8 Aerospace

- 8.9 Textiles & leather

- 8.10 Rubber industry

- 8.11 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Direct sales (B2B)

- 9.3 Online platforms/E-commerce

- 9.4 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Arkema S.A.

- 11.2 Genomatica

- 11.3 LanzaTech (Carbon Capture to Chemicals)

- 11.4 Vertec Biosolvents

- 11.5 Celanese Corporation

- 11.6 Cetex Petrochemicals

- 11.7 Eastman Chemical Company

- 11.8 ExxonMobil Corporation

- 11.9 INEOS Group

- 11.10 Idemitsu Kosan Co., Ltd.

- 11.11 LG Chem Ltd.

- 11.12 Maruzen Petrochemical Co., Ltd.

- 11.13 Nouryon

- 11.14 PTT Global Chemical Public Company Limited

- 11.15 Sasol Limited

- 11.16 Shell Chemicals (Shell Plc)

- 11.17 Solvay S.A.

- 11.18 SK Energy

- 11.19 PetroChina Company Limited

- 11.20 Mitsubishi Chemical Corporation

甲基异戊基酮市场按等级、生产流程、应用、终端用户产业和分销管道划分-全球预测(2026-2032)电子级丁酮市场按形态、包装规格、应用、终端用户产业和分销管道划分-2026-2032年全球预测丁酮市场(按形态、纯度等级、分销管道、应用和最终用户产业)—2025-2032 年全球预测

甲基异戊基酮市场按等级、生产流程、应用、终端用户产业和分销管道划分-全球预测(2026-2032)电子级丁酮市场按形态、包装规格、应用、终端用户产业和分销管道划分-2026-2032年全球预测丁酮市场(按形态、纯度等级、分销管道、应用和最终用户产业)—2025-2032 年全球预测 全球碳酸乙甲酯市场

全球碳酸乙甲酯市场 丁酮市场规模、份额和趋势分析报告:按应用、地区和细分市场预测,2025-2033 年

丁酮市场规模、份额和趋势分析报告:按应用、地区和细分市场预测,2025-2033 年 2025 年至 2033 年甲基乙基酮 (MEK) 市场报告,按应用(油漆和涂料、粘合剂和稀释剂、印刷油墨、药品等)、形态(液态、固态)、等级(普通级、聚氨酯级等)和地区划分全球氯乙酸甲酯和乙酯市场

2025 年至 2033 年甲基乙基酮 (MEK) 市场报告,按应用(油漆和涂料、粘合剂和稀释剂、印刷油墨、药品等)、形态(液态、固态)、等级(普通级、聚氨酯级等)和地区划分全球氯乙酸甲酯和乙酯市场 丁酮的全球市场:各等级,各终端用户业界,各地区,机会,预测,2018年~2032年

丁酮的全球市场:各等级,各终端用户业界,各地区,机会,预测,2018年~2032年 丁酮市场报告:趋势、预测和竞争分析(至2031年)

丁酮市场报告:趋势、预测和竞争分析(至2031年) 丁酮市场规模、份额和成长分析(按形式、等级、应用、最终用户产业和地区)- 产业预测 2025-2032

丁酮市场规模、份额和成长分析(按形式、等级、应用、最终用户产业和地区)- 产业预测 2025-2032