|

市场调查报告书

商品编码

1928907

数位造船厂市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Digital Shipyard Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

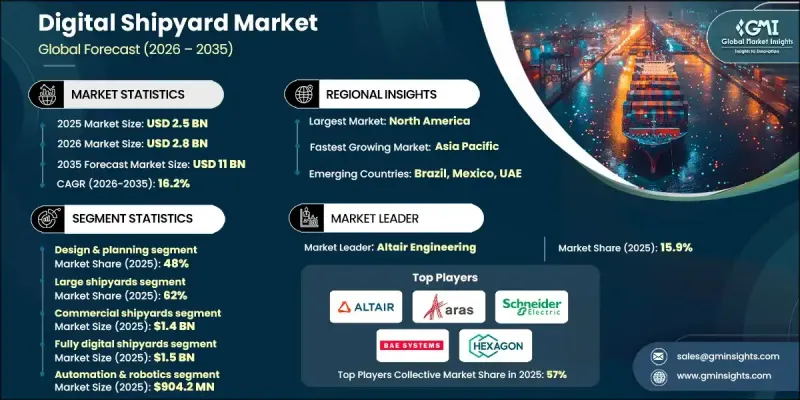

全球数位造船厂市场预计到 2025 年将达到 25 亿美元,到 2035 年将达到 110 亿美元,年复合成长率为 16.2%。

市场成长的驱动力来自对高效造船和维护流程日益增长的需求、对互联智慧系统的依赖性不断增强,以及日益严格的监管和环境合规要求。造船企业、海军机构和商业营运商致力于降低成本、提高建造精度并缩短计划週期,这加速了数位化船厂平台的普及应用。数据驱动的决策正成为船厂营运的核心,有助于提高生产效率、提升安全标准并优化资产生命週期管理。随着产业的现代化进程,数位化船厂解决方案正成为一项关键的基础技术,为整个造船和维修生态系统提供即时视觉性、预测能力和协作工作流程。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 25亿美元 |

| 预测金额 | 110亿美元 |

| 复合年增长率 | 16.2% |

人工智慧、机器学习、互联感测器和虚拟建模技术的进步正在重塑造船厂的营运模式,以智慧自动化系统取代人工操作。整合式数位平台能够对设计、建造和维护活动进行持续监控、效能分析和基于模拟的规划。这些功能可以减少返工、提高合规性并支援预防性维护策略。随着分析、自动化和互联基础设施融入日常运营,数位化造船环境不断成熟,从而支援扩充性和长期生产计画。

预计到2025年,设计和规划领域将占据48%的市场份额,并在2035年之前以16.8%的复合年增长率成长。该领域的主导地位归功于精确建模、协调的工作流程和预测性进度安排的重要性。数位化规划工具支援复杂造船专案间的协作,从而减少设计错误并缩短交付时间。

预计到2025年,大型造船厂将占据62%的市场份额,并在2026年至2035年间以16.7%的复合年增长率增长。其主导地位得益于更雄厚的财力、先进的基础设施以及在大规模营运中部署全面数位化解决方案的能力。高度的自动化和系统整合使大型造船厂成为端到端数位化造船技术的关键采用者。

预计到 2025 年,美国数位化造船厂市场将占据 78% 的市场份额,价值 7.547 亿美元。这一区域主导地位得益于先进的工业能力、强大的技术应用以及对互联智慧造船厂平台的早期采用,这些平台提高了营运效率和安全性。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 扩大先进数位技术的应用

- 提高营运效率和降低成本的需求

- 来自国防和民用领域的需求不断增长

- 监理合规和环境标准

- 产业潜在风险与挑战

- 安装和维修成本高昂

- 与旧有系统的复杂集成

- 市场机会

- 预测性维护和生命週期优化

- 中小型造船厂的引进状况

- 实施基于云端的整合平台

- 扩展数位双胞胎和预测性维护解决方案

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国:职业安全与美国海岸警卫队指南

- 加拿大:运输部和职业安全与健康指南

- 欧洲

- 德国:联邦交通数位化部 (BMVI) 和德国工人赔偿保险局 (DGUV) 的规定

- 法国:DGME 和 CNES 指南

- 英国:海事和海洋事务部 (MCA) 和健康与安全执行局 (HSE) 的相关规定

- 义大利:ENAC 和 INAIL 指南

- 亚太地区

- 中国:中国船级社(CCS)和海事安全法规

- 日本:JCAB 和国土交通省指南

- 韩国:国土交通部 (MOLIT) 和安全指南

- 印度:航运总局和码头安全规则

- 拉丁美洲

- 巴西:ANTAQ(国家海事局)和基础设施部指南

- 墨西哥:SEMAR 和 DGPM 法规

- 中东和非洲

- 阿联酋:能源和基础设施部法规

- 沙乌地阿拉伯:沙乌地阿拉伯港务局指南

- 北美洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 使用案例场景

- 数位造船厂架构框架

- 端到端数位化造船厂参考架构

- IT-OT融合层

- 数据互通性和整合标准

- 造船业中的网实整合系统

- 数位成熟度和准备度指数

- 造船厂数位化成熟度等级

- 能力标竿分析:传统船厂与智慧船厂

- 区域成熟度比较

- 按造船厂规模分類的战备差距

- 买方和相关人员分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 按类型分類的市场估算与预测,2022-2035年

- 商业造船厂

- 军用造船厂

第六章 依製造流程分類的市场估算与预测,2022-2035年

- 设计与规划

- 建造

- 维护/修理

第七章 依产能分類的市场估计与预测,2022-2035年

- 大型造船厂

- 中型造船厂

- 小规模造船厂

第八章 依数位化程度分類的市场估算与预测,2022-2035年

- 全数数位化造船厂

- 半数数位化造船厂

第九章 依技术分類的市场估计与预测,2022-2035年

- 自动化和机器人技术

- 物联网 (IoT)

- 数据分析和巨量资料

- 数位双胞胎技术

- 其他的

第十章 依最终用途分類的市场估计与预测,2022-2035年

- 造船公司和船厂

- 国防/军事

- 船舶所有者和运营商

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

第十二章:公司简介

- Global Player

- ABB

- Altair Engineering

- Aras

- BAE Systems

- Dassault Systemes

- Hexagon

- iBase-t

- Mitsubishi Heavy Industries

- Schneider Electric(AVEVA)

- Siemens

- Regional Player

- Austal

- China State Shipbuilding Corporation(CSSC)

- Daewoo Shipbuilding &Marine Engineering

- Fincantieri

- Honeywell International

- Hyundai Heavy Industries

- Kongsberg Gruppen

- Larsen &Toubro(L&T)Shipbuilding

- Mitsui E&S

- Navantia

- 新兴企业

- DNV Digital Solutions

- Marine Technologies

- MarineCFO

- Navis Marine Solutions

- ShipConstructor

The Global Digital Shipyard Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 16.2% to reach USD 11 billion by 2035.

The market growth is driven by the rising need for efficient shipbuilding and maintenance processes, increased reliance on connected and intelligent systems, and stricter regulatory and environmental compliance requirements. Shipbuilders, naval organizations, and commercial operators are increasingly focused on reducing costs, improving build accuracy, and shortening project timelines, which is accelerating the adoption of digital shipyard platforms. Data-driven decision-making is becoming central to shipyard operations, enabling higher productivity, improved safety standards, and optimized asset lifecycle management. As the industry modernizes, digital shipyard solutions are emerging as critical enablers that support real-time visibility, predictive capabilities, and coordinated workflows across the entire shipbuilding and repair ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $11 Billion |

| CAGR | 16.2% |

Advancements in artificial intelligence, machine learning, connected sensors, and virtual modeling are reshaping shipyard operations by replacing manual processes with intelligent, automated systems. Integrated digital platforms allow continuous monitoring, performance analysis, and simulation-based planning across design, construction, and maintenance activities. These capabilities reduce rework, improve compliance, and enable proactive maintenance strategies. The digital shipyard environment continues to mature as analytics, automation, and connected infrastructure become embedded into daily operations, supporting scalable and long-term production planning.

The design and planning segment held a 48% share in 2025 and is projected to grow at a CAGR of 16.8% through 2035. This segment leads due to its importance in enabling accurate modeling, coordinated workflows, and predictive scheduling. Digital planning tools support collaboration, reduce design errors, and improve delivery timelines across complex shipbuilding programs.

The large shipyards segment held 62% share in 2025 and is expected to grow at a CAGR of 16.7% between 2026 and 2035. Their leadership is supported by greater financial capacity, advanced infrastructure, and the ability to deploy comprehensive digital solutions across large-scale operations. High levels of automation and system integration position large facilities as primary adopters of end-to-end digital shipyard technologies.

U.S. Digital Shipyard Market accounted for 78% share in 2025, generating USD 754.7 million. Regional leadership is supported by advanced industrial capabilities, strong technology adoption, and early implementation of connected and intelligent shipyard platforms that enhance operational efficiency and safety.

Key companies active in the Global Digital Shipyard Market include Siemens, ABB, Dassault Systemes, Schneider Electric (AVEVA), Honeywell International, Hexagon, BAE Systems, Altair Engineering, Aras, and iBase-t. Companies operating in the Global Digital Shipyard Market are strengthening their competitive positions through continuous technology innovation and strategic collaboration. Providers are investing heavily in AI-driven design tools, real-time analytics, and integrated digital platforms to deliver end-to-end visibility across shipyard operations. Partnerships with shipbuilders, defense organizations, and technology firms are being used to accelerate the deployment and customization of solutions. Many players are expanding cloud-based offerings to support scalability and remote collaboration. Emphasis is also being placed on cybersecurity, compliance support, and predictive maintenance capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Process

- 2.2.4 Capacity

- 2.2.5 Digitalization Level

- 2.2.6 Technology

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Adoption of Advanced Digital Technologies

- 3.2.1.2 Need for Operational Efficiency and Cost Reduction

- 3.2.1.3 Growing Demand from Defense and Commercial Sectors

- 3.2.1.4 Regulatory Compliance and Environmental Standards

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Implementation and Maintenance Costs

- 3.2.2.2 Complex Integration with Legacy Systems

- 3.2.3 Market opportunities

- 3.2.3.1 Predictive Maintenance and Lifecycle Optimization

- 3.2.3.2 Adoption by Medium and Small Shipyards

- 3.2.3.3 Cloud-Based and Integrated Platform Deployments

- 3.2.3.4 Expansion of Digital Twin and Predictive Maintenance Solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: OSHA & US Coast Guard Guidelines

- 3.4.1.2 Canada: Transport & WorkSafe Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: BMVI & DGUV Regulations

- 3.4.2.2 France: DGME & CNES Guidelines

- 3.4.2.3 UK: MCA & HSE Regulations

- 3.4.2.4 Italy: ENAC & INAIL Guidelines

- 3.4.3 Asia Pacific

- 3.4.3.1 China: CCS & Maritime Safety Regulations

- 3.4.3.2 Japan: JCAB & MLIT Guidelines

- 3.4.3.3 South Korea: MOLIT & Safety Guidelines

- 3.4.3.4 India: DG Shipping & Dock Safety Rules

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ANTAQ & Ministry of Infrastructure Guidelines

- 3.4.4.2 Mexico: SEMAR & DGPM Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Ministry of Energy & Infrastructure Regulations

- 3.4.5.2 Saudi Arabia: Saudi Ports Authority Guidelines

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Digital Shipyard Architecture Framework

- 3.13.1 End-to-end digital shipyard reference architecture

- 3.13.2 IT-OT convergence layers

- 3.13.3 Data interoperability & integration standards

- 3.13.4 Cyber-physical systems in shipbuilding

- 3.14 Digital Maturity & Readiness Index

- 3.14.1 Shipyard digital maturity levels

- 3.14.2 Capability benchmarking: legacy vs smart shipyards

- 3.14.3 Regional maturity comparison

- 3.14.4 Readiness gaps by shipyard size

- 3.15 Buyer & Stakeholder Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Commercial shipyards

- 5.3 Military shipyards

Chapter 6 Market Estimates & Forecast, By Process, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Design & planning

- 6.3 Construction

- 6.4 Maintenance & repair

Chapter 7 Market Estimates & Forecast, By Capacity, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Large shipyards

- 7.3 Medium shipyards

- 7.4 Small shipyards

Chapter 8 Market Estimates & Forecast, By Digitalization Level, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Fully digital shipyard

- 8.3 Semi-digital shipyard

Chapter 9 Market Estimates & Forecast, By Technology, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 Automation & robotics

- 9.3 Internet of Things (IoT)

- 9.4 Data analytics & big data

- 9.5 Digital twin technology

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 Shipbuilders & shipyards

- 10.3 Defense & military

- 10.4 Ship Owners & Operators

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 ABB

- 12.1.2 Altair Engineering

- 12.1.3 Aras

- 12.1.4 BAE Systems

- 12.1.5 Dassault Systemes

- 12.1.6 Hexagon

- 12.1.7 iBase-t

- 12.1.8 Mitsubishi Heavy Industries

- 12.1.9 Schneider Electric (AVEVA)

- 12.1.10 Siemens

- 12.2 Regional Player

- 12.2.1 Austal

- 12.2.2 China State Shipbuilding Corporation (CSSC)

- 12.2.3 Daewoo Shipbuilding & Marine Engineering

- 12.2.4 Fincantieri

- 12.2.5 Honeywell International

- 12.2.6 Hyundai Heavy Industries

- 12.2.7 Kongsberg Gruppen

- 12.2.8 Larsen & Toubro (L&T) Shipbuilding

- 12.2.9 Mitsui E&S

- 12.2.10 Navantia

- 12.3 Emerging Players

- 12.3.1 DNV Digital Solutions

- 12.3.2 Marine Technologies

- 12.3.3 MarineCFO

- 12.3.4 Navis Marine Solutions

- 12.3.5 ShipConstructor

2026年全球造船厂4.0市场报告

2026年全球造船厂4.0市场报告 数位造船厂市场:2026-2032年全球市场预测(按组件、服务类型、应用、最终用户和部署模式划分)2026年全球数位化造船厂市场报告

数位造船厂市场:2026-2032年全球市场预测(按组件、服务类型、应用、最终用户和部署模式划分)2026年全球数位化造船厂市场报告 2026-2030年全球数位化造船厂市场

2026-2030年全球数位化造船厂市场 数位造船厂市场规模、份额和成长分析(按造船厂类型、技术、产能、工艺、数位化程度、最终用途和地区划分)—产业预测(2026-2033 年)

数位造船厂市场规模、份额和成长分析(按造船厂类型、技术、产能、工艺、数位化程度、最终用途和地区划分)—产业预测(2026-2033 年) 数位造船厂:全球市场份额和排名、总收入和需求预测(2025-2031年)

数位造船厂:全球市场份额和排名、总收入和需求预测(2025-2031年) 数位造船厂市场规模(按造船厂类型、规模、地区和预测)

数位造船厂市场规模(按造船厂类型、规模、地区和预测) 全球数位造船厂市场规模、份额、趋势分析报告:按解决方案、按产能、按造船厂类型、按技术、按地区、2024-2031 年展望和预测

全球数位造船厂市场规模、份额、趋势分析报告:按解决方案、按产能、按造船厂类型、按技术、按地区、2024-2031 年展望和预测 数位造船厂市场规模、份额和趋势分析报告:2025-2030 年按解决方案、造船厂类型、能力、技术、地区和细分市场进行的预测

数位造船厂市场规模、份额和趋势分析报告:2025-2030 年按解决方案、造船厂类型、能力、技术、地区和细分市场进行的预测