|

市场调查报告书

商品编码

1928912

自动驾驶汽车市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)Self-driving Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球自动驾驶汽车市场预计到 2025 年将达到 2,024 亿美元,到 2035 年将达到 3,546 亿美元,年复合成长率为 5.4%。

人们对降低交通风险和提高出行效率的日益关注,持续加速自动驾驶技术的应用。支援受控测试和早期应用的法规结构,为自动驾驶技术的商业化开闢了新的机会。人工智慧、感测系统和高效能运算的进步,正在提升系统在实际环境中的可靠性和效能。自动驾驶车辆与智慧城市基础设施的整合,透过连网交通平台、车路通讯和自适应路径规划等技术,进一步增强了市场动力。这些技术有助于改善交通流量、缓解拥塞并降低能源消耗。自动驾驶出行平台的扩展,透过重塑城市交通经济格局、提高车队效率并实现可扩展的自动化交通模式,为自动驾驶出行服务的进一步发展提供了支持。随着车队营运商在部署自动化系统后营运成本至少降低30%,自动驾驶出行服务平台市场持续扩张。这些平台已被证明具有商业性可行性和扩充性,增强了人们对自动驾驶交通服务的长期信心。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 2024亿美元 |

| 预测金额 | 3546亿美元 |

| 复合年增长率 | 5.4% |

预计到2025年,L3级自动驾驶市占率将达到46%,并在2026年至2035年间以5.2%的复合年增长率成长。 L3级自动驾驶车辆正被广泛应用于多个车型类别,因为它们能够在部分减轻驾驶员负担的同时,确保驾驶员随时做好准备。相当一部分自动驾驶研发专案仍专注于L3级功能,从而带动了市场对L3级自动驾驶的持续需求。

预计到2025年,内燃机汽车市占率将达到72%,并在2035年之前以4.8%的复合年增长率成长。这些车辆受益于成熟的製造平台,简化了自动化整合。电动自动驾驶汽车占据第二大市场份额,这得益于它们与软体驱动架构、先进感测器阵列和集中式运算系统的兼容性,而内燃机平台则更依赖机械性能特性。

预计到 2025 年,美国自动驾驶汽车市场将占据 83% 的市场份额,市场规模将达到 336 亿美元。凭藉强劲的投资活动、有利的政策倡议以及加速的商业部署,美国将继续保持其作为自动驾驶汽车发展和长期市场成长核心中心的地位。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 道路安全和事故减少

- 人工智慧和感测器技术的进步

- 政府测试核准和监管

- 自动驾驶服务的成长

- 产业潜在风险与挑战

- 高昂的开发和检验成本

- 区域法规的不确定性

- 市场机会

- 机器人计程车和自动驾驶汽车服务的扩展

- 自主物流与货运

- 与智慧城市基础建设的融合

- 成长潜力分析

- 监管环境

- 北美洲

- 美国国家公路交通安全管理局更新自动驾驶车辆安全标准

- 美国运输部(DOT)自动驾驶车辆综合规划(AVCP)

- 州级自动驾驶考试许可证(加州车辆管理局和内华达州车辆管理局指南)

- 加拿大运输部自动驾驶系统(ADS)测试指南

- 欧洲

- 联合国欧洲经济委员会关于自动车道维持系统(ALKS)的第157号条例

- 欧盟自动驾驶系统(ADS)型式认证通用安全法规(GSR)

- 德国联邦汽车运输管理局 (KBA) 四级驾驶许可证

- 英国自动驾驶汽车法律与责任框架

- 亚太地区

- 中华人民共和国工业与资讯化部(工信部)ICV市场准入指南

- 国土交通省(MLIT)四级执照

- 韩国国土交通部自动驾驶汽车商业化安全标准

- 新加坡自动驾驶车辆技术标准 68 (TR 68)

- 印度公路运输和公路部 (MoRTH) 新兴高级驾驶辅助系统 (ADAS) 指南

- 拉丁美洲

- 巴西国家交通委员会(CONTRAN)关于驾驶员辅助的决议

- 墨西哥《交通与道路安全基本法》(LGMSV)对自动化的影响

- 智利运输部关于自动驾驶初步试验的规定

- 与联合国世界车辆法规协调论坛(WP.29)进行区域合作

- 中东和非洲

- 阿联酋道路和交通管理局(RTA)自动驾驶交通法规

- 沙乌地阿拉伯SASO电动与自动驾驶车辆技术标准

- 以色列运输部自动驾驶车辆测试指南

- 南非引进智慧型运输系统(ITS)的标准

- 北美洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产基地

- 消费基础

- 出口和进口

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 自动驾驶系统结构和软体栈

- 自动驾驶系统结构及堆迭分析

- 计算、感测器和软体编配模型

- 自动驾驶软体、人工智慧和数据飞轮

- 检验、测试和安全保证框架

- 自动驾驶汽车的经营模式和获利模式

- 高精度测绘、车联网和基础设施依赖性

- 消费者信任与接受度的障碍

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

5. 按自动驾驶等级分類的市场估算与预测,2022-2035 年

- 一级

- 二级

- 3级

- 4级

- 5级

第六章 按类型分類的市场估算与预测,2022-2035年

- 内燃机(ICE)

- 电的

- 混合动力汽车

第七章 按技术分類的市场估计与预测,2022-2035年

- 基于摄影机的系统

- 基于雷达的系统

- 基于光达的系统

- 感测器融合系统

第八章 按车辆类型分類的市场估算与预测,2022-2035年

- 小型车

- 中型车

- SUV和豪华轿车

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 个人使用

- 共享出行

- 物流/配送

- 公共运输

- 其他的

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

第十一章 公司简介

- 世界玩家

- BMW

- Daimler(Mercedes-Benz)

- Ford Motor Company

- General Motors(GM)

- Honda Motor

- Hyundai Motor

- Stellantis

- Tesla

- Toyota Motor

- Volkswagen

- 区域玩家

- BYD

- Geely

- Renault-Nissan-Mitsubishi Alliance

- SAIC Motor

- Tata Motors

- 新兴参与者/颠覆者

- Aurora Innovation

- Baidu

- NIO

- Waymo

- XPeng Motors

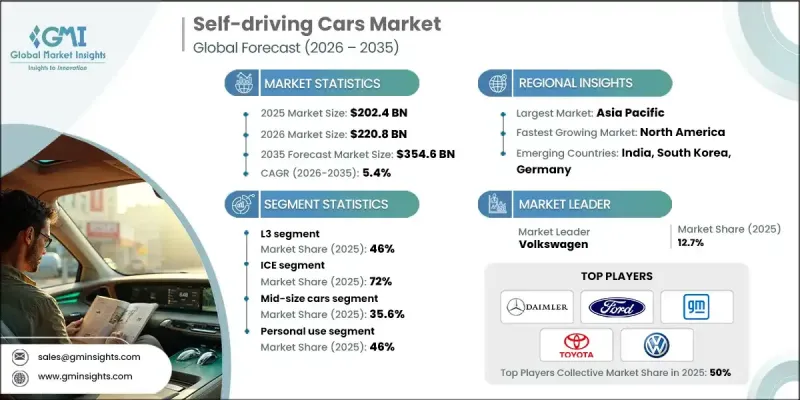

The Global Self-driving Cars Market was valued at USD 202.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 354.6 billion by 2035.

Increased focus on minimizing traffic-related risks and improving travel efficiency continues to accelerate adoption. Regulatory frameworks that support controlled testing and early deployment are opening new commercialization opportunities for autonomous technologies. Advancements in artificial intelligence, sensing systems, and high-performance computing are improving system reliability and real-world performance. Integration of autonomous vehicles with intelligent urban infrastructure is strengthening market momentum through connected traffic platforms, vehicle-to-infrastructure communication, and adaptive routing capabilities. These technologies are improving traffic flow, lowering congestion levels, and supporting reduced energy consumption. Growth is further supported by the expansion of autonomous mobility platforms, which are reshaping urban transportation economics and improving fleet efficiency while enabling scalable automated transport models. The autonomous mobility as a service platform market continues to expand as fleet operators report operational cost reductions of at least 30% following the adoption of automation-focused systems. These platforms are proving commercially viable and scalable, reinforcing long-term confidence in automated transportation services.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $202.4 Billion |

| Forecast Value | $354.6 Billion |

| CAGR | 5.4% |

The Level 3 automation segment held a 46% share in 2025 and is forecast to grow at a CAGR of 5.2% from 2026 to 2035. Level 3 vehicles allow partial disengagement from driving tasks while ensuring driver readiness, making them widely adopted across multiple vehicle categories. A significant portion of autonomous development programs continues to focus on Level 3 functionality, supporting sustained demand.

The internal combustion engine vehicles segment accounted for 72% share in 2025 and is expected to grow at a CAGR of 4.8% through 2035. These vehicles benefit from established manufacturing platforms that simplify automation integration. Electric autonomous vehicles represent the second-largest segment due to their compatibility with software-driven architectures, advanced sensor arrays, and centralized computing systems, while ICE platforms rely more heavily on mechanical performance characteristics.

United States Self-driving Cars Market held an 83% share and generated USD 33.6 billion in 2025. Strong investment activity, favorable policy initiatives, and accelerating commercial deployment continue to position the country as a central hub for autonomous vehicle development and long-term market growth.

Key companies active in the Global Self-driving Cars Market include Tesla, Toyota Motor, Hyundai Motor, Volkswagen, General Motors, BMW, Ford Motor Company, Daimler (Mercedes-Benz), Honda Motor, and BYD. Companies in the Global Self-driving Cars Market are strengthening their market position through aggressive investment in artificial intelligence, advanced driver assistance software, and proprietary autonomous platforms. Strategic partnerships with technology providers are enabling faster innovation cycles and improved system integration. Automakers are prioritizing scalable architectures that support multiple autonomy levels across vehicle portfolios. Continuous real-world testing and data-driven optimization remain central to product refinement. Firms are also focusing on regulatory alignment and safety validation to accelerate approvals. Expansion into fleet-based and mobility service models is helping companies diversify revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Level of Autonomy

- 2.2.3 Propulsion

- 2.2.4 Technology

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Road safety and accident reduction

- 3.2.1.3 Advancements in artificial intelligence and sensors

- 3.2.1.4 Government testing approvals and regulations

- 3.2.1.5 Growth of autonomous mobility services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and validation costs

- 3.2.2.2 Regulatory uncertainty across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of robotaxi and autonomous fleet services

- 3.2.3.2 Autonomous logistics and freight transport

- 3.2.3.3 Integration with smart city infrastructure

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US National Highway Traffic Safety Administration (NHTSA) FMVSS Updates for Automated Vehicles

- 3.4.1.2 US Department of Transportation (DOT) Automated Vehicles Comprehensive Plan (AVCP)

- 3.4.1.3 State-Level Autonomous Testing Permits (California DMV & Nevada DMV Guidelines)

- 3.4.1.4 Transport Canada Guidelines for Testing Automated Driving Systems (ADS)

- 3.4.2 Europe

- 3.4.2.1 UNECE Regulation No. 157 on Automated Lane Keeping Systems (ALKS)

- 3.4.2.2 European Union General Safety Regulation (GSR) for Type Approval of ADS

- 3.4.2.3 Germany Federal Motor Transport Authority (KBA) Level 4 Operating Permits

- 3.4.2.4 UK Automated Vehicles Act and Liability Frameworks

- 3.4.3 Asia Pacific

- 3.4.3.1 China Ministry of Industry and Information Technology (MIIT) ICV Market Access Guide

- 3.4.3.2 Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT) Level 4 Licensing

- 3.4.3.3 South Korea MOLIT Safety Standards for Autonomous Vehicle Commercialization

- 3.4.3.4 Singapore Technical Reference 68 (TR 68) for Autonomous Vehicles

- 3.4.3.5 India Ministry of Road Transport and Highways (MoRTH) Emerging ADAS Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil National Traffic Council (CONTRAN) Resolutions on Assisted Driving

- 3.4.4.2 Mexico Mobility & Road Safety General Law (LGMSV) Implications for Automation

- 3.4.4.3 Chile Ministry of Transport Regulations on Autonomous Pilot Testing

- 3.4.4.4 Regional Alignment with UN World Forum for Harmonization of Vehicle Regulations (WP.29)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Roads and Transport Authority (RTA) Regulations for Autonomous Transport

- 3.4.5.2 Saudi Arabia SASO Technical Standards for Electric and Autonomous Vehicles

- 3.4.5.3 Israel Ministry of Transport Guidelines for Driverless Vehicle Trials

- 3.4.5.4 South Africa Standards for Intelligent Transport Systems (ITS) Deployment

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 AV System Architecture & Software Stack

- 3.13.1 Autonomous driving system architecture & stack analysis

- 3.13.2 Compute, sensor, and software orchestration models

- 3.14 Autonomous Software, AI & Data Flywheel

- 3.15 Validation, Testing & Safety Assurance Framework

- 3.16 AV Business Models & Monetization

- 3.17 HD Mapping, V2X & Infrastructure Dependency

- 3.18 Consumer Trust & Adoption Barriers

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Level of Autonomy, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 L1

- 5.3 L2

- 5.4 L3

- 5.5 L4

- 5.6 L5

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.4 Hybrid vehicle

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Camera-Based Systems

- 7.3 Radar-Based Systems

- 7.4 LiDAR-Based Systems

- 7.5 Sensor Fusion Systems

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Compact cars

- 8.3 Mid-size cars

- 8.4 SUVs & luxury cars

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Personal use

- 9.3 Shared mobility

- 9.4 Logistics & delivery

- 9.5 Public transport

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BMW

- 11.1.2 Daimler (Mercedes-Benz)

- 11.1.3 Ford Motor Company

- 11.1.4 General Motors (GM)

- 11.1.5 Honda Motor

- 11.1.6 Hyundai Motor

- 11.1.7 Stellantis

- 11.1.8 Tesla

- 11.1.9 Toyota Motor

- 11.1.10 Volkswagen

- 11.2 Regional Players

- 11.2.1 BYD

- 11.2.2 Geely

- 11.2.3 Renault-Nissan-Mitsubishi Alliance

- 11.2.4 SAIC Motor

- 11.2.5 Tata Motors

- 11.3 Emerging Players / Disruptors

- 11.3.1 Aurora Innovation

- 11.3.2 Baidu

- 11.3.3 NIO

- 11.3.4 Waymo

- 11.3.5 XPeng Motors